About A Certain Database Company [Free Post]

Reflections on my decision this week to sell a big chunk of Oracle stock.

Friends of NFTBC.

I have my doubts that all of you will want to hear more about Oracle (ORCL) this week, so I’m making this post free to read in the vain hope of finding a wider audience. Consider it more of a journal entry and a thinking-out-loud exercise, for those who are interested. Until this week, ORCL was my largest holding and had been so for many years - so it’s been occupying a lot of headspace for me and it feels weird for me not to write about it.

If nothing else, events of recent days provide us with a nice example of the Beauty Contest having gone full circle - and that makes it kind of interesting in mv view.

Lots of pundits who have probably not looked at ORCL in years (or ever) now seem to have very strong views about it and about what it can and can’t achieve in future. While I don’t consider myself much of an authority on anything, perhaps my long experience with the company can provide a little extra perspective - you decide.

Fear not, we’ll be back to business as usual at NFTBC soon and there’s a new deep dive coming up - as it happens, it’s a software stock.

[NFTBC does not provide financial advice - please do your own research. Disclosure: I currently own ORCL shares]

Opening thoughts

So why are you writing about ORCL? / Have you lost your mind?

As I’ve noted previously, what I’m interested in most at NFTBC are the following characteristics:

Business that are doing something different and breaking with convention

The necessary institutional structures that will allow unconventional behaviour to persist, rather than fade due to pressure to conform

Situations where the strategy is sound and carries a reasonable prospect of a favourable outcome

Situations where the outcome might not yet be obvious

Less talked about names

Back in 2018 when I started buying ORCL, the stock fit the bill the perfectly. Revenue had been flat for five years (and would stay flat for another two). The shares were no higher than in 2000. Shares at various times between 2018 and 2020 were at 11-12x earnings - I kept on buying and buying up until March 2020. ORCL was considered to be a classic value trap - no one was expecting it to do anything at all other than wither away quietly.

As it turns out, ORCL was indeed doing something quite different. The fact that the company was controlled by one person (you’ve probably heard of him), meant they could keep pushing in that direction for better or for worse without interference from others. And as it turns out, the strategy was a good one. It just wasn’t glaringly obvious at the time - to see it required a little imagination and an open mind.

The stock has been very successful - up around 7X in 7 years for me.

For me, ORCL has always been one of those stocks that requires an appropriate balance between knowing too much and knowing too little - in order to be able to tell the wood from the trees. Regeneron is a similar one. I’ll explain. If you’re a specialist expert in the field of technology investing there’s never been any shortage of convincing reasons to talk yourself out of owning ORCL:

Larry talks nonsense

relational databases are obsolete

ORCL code is ancient

customers hate ORCL

CIO surveys say customers are reducing ORCL spend

they missed the cloud

they’re doing M&A to hide their lousy legacy software business

they’re not doing enough capex to compete in cloud

their cloud is low margin

developers won’t use OCI

they’re only getting cloud customers through aggressive pricing

customers will return to the other hyperscalers once capacity constraints are over

they’re only growing EPS through financial engineering

I’ve heard all of these arguments and many more from very sophisticated technology investors - all the way from $45 up to $330. While there might be ‘truthiness’ to some of these claims, the thing is, a specialist cookie cutter approach to analysing ORCL hasn’t worked. For example, while Larry sounds like he’s talking nonsense much of the time (such is his style), buried in the noise there’s still plenty of signal - you just have to keep listening, verifying and extending whatever timeframe he gives. And this is why knowing too little won’t do you any favours either - if you don’t listen to what ORCL says then you won’t even realise that the possibility of change exists.

More than a decade ago ORCL had a go at jumping on the cloud infrastructure bandwagon, but it didn’t work - they were indeed too late. But then, around 2014, Larry started poaching engineers from from AWS and Azure and set them up in Seattle - perhaps most notably Don Johnson and Clay Magouyrk. He gave them a blank sheet of paper to design a new cloud, realising that ORCL had to do something different to have a chance of success. And that’s exactly what they did. For a while ORCL called it “Gen 2 Cloud Infrastructure” and then eventually “Oracle Cloud Infrastructure” or “OCI” as it is today. I don’t intend to go into all the background and context here, but I’ll give you an abbreviated version. Part of it also stems from ORCL’s expertise in engineered systems and high-speed networking acquired with Sun Microsystems in 2010. Here are perhaps the two most important takeaways for now (but there are others): 1) OCI is fast which makes it particularly well suited to AI training and inference (also, faster = cheaper) and 2) OCI racks are uniform and modular. The latter means that ORCL can be highly efficient on capex while also providing flexibility and speed of deployment - ORCL can install an entire cloud region on just 6 racks in a customer’s own datacenter or it can fit out giant GW+ datacenters, and everything in between.

There are other parts to the ORCL thesis complimentary to OCI, but I’ll leave those for another time perhaps.

Fast Forward

Gradually, then suddenly, ORCL clawed its way back to growth - with an inflection arriving shortly after the AI revolution got underway. That was when OCI really began to gain traction. Three years ago, on the eve of ChatGPT’s release, OCI had an annual run-rate of $3.6bn - today OCI does that much in a single quarter and it’s not slowing down.

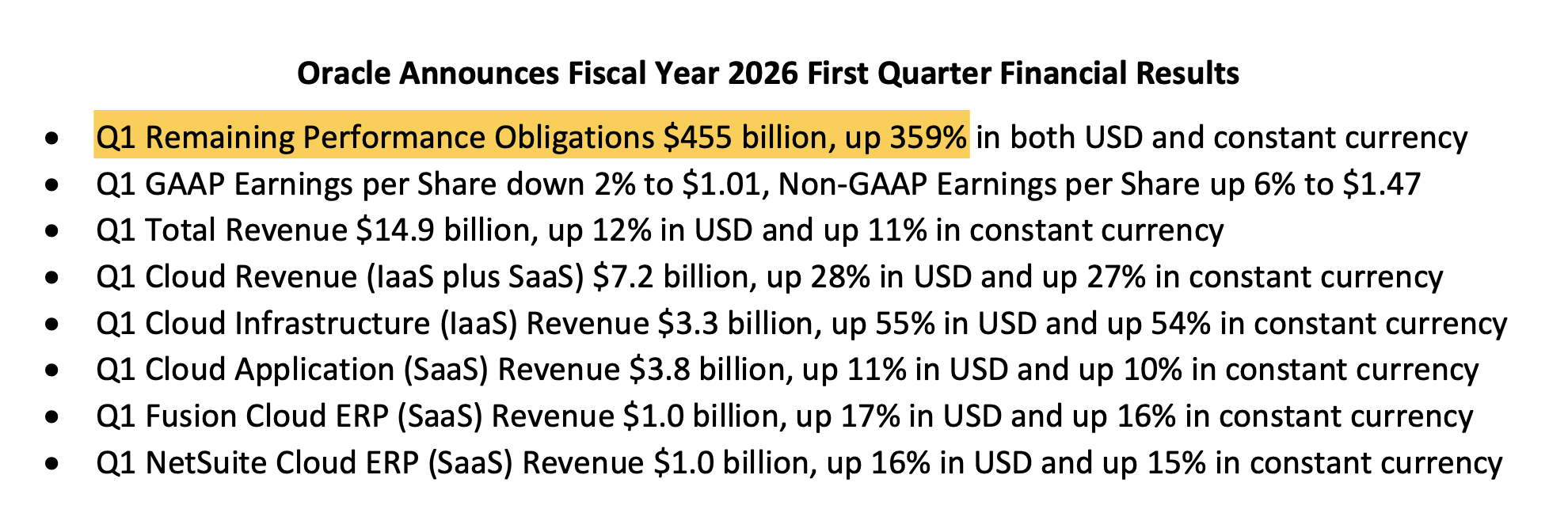

By 2025 most investors, like it or not, seemed to have conceded that ORCL had an accelerating top line. But then a bombshell landed this week, causing an extraordinary 35% one-day pop in ORCL stock up to a market cap of more than $900bn:

And:

To the uninitiated, remaining performance obligation (RPO) simply means contracted services that have not yet been performed or recognised in revenue. Some RPO gets recognised in the next 12 months and some (indeed, now the vast majority) over longer periods per whatever the underlying customer contract says. The bulk of this massive RPO ramp comes from AI customers contracting with OCI - OpenAI, xAI, Meta, NVIDIA etc. And then WSJ sources began to emerge that of the additional $355bn in RPO, $300bn comes from a contract with OpenAI. We had an initial hint of this in June, when ORCL disclosed the existence of a large contract that would produce more than $30bn of revenue starting in FY2028 (ORCL’s financial year runs from the beginning of June, so FY28 is June 2027 to May 2028). Per the WSJ the contract starts in 2027 (i.e. FY2028) and runs for “roughly” five years.

Right on cue, the doubters started showing up:

“this is the surest sign yet of a bubble”

“how can OpenAI possibly raise $300bn to pay for this?”

“there’s no way Oracle can pay for the capex - they’re already indebted and free cash flow negative”

“the deal has no substance - it’s a pipe dream”

Yet others saw ORCL’s RPO as further validation that we’re not in a bubble and that the AI revolution is coming at us fast 🤷♂️. Which is it then? My answer is that I don’t know. My intention here is to try to take a sober look at things from the perspective of a ORCL shareholder.

Can ORCL afford the capex?

In short, I believe the answer is yes. However, doing an equity issue seems sensible if they want to keep leverage at around 2.5x.

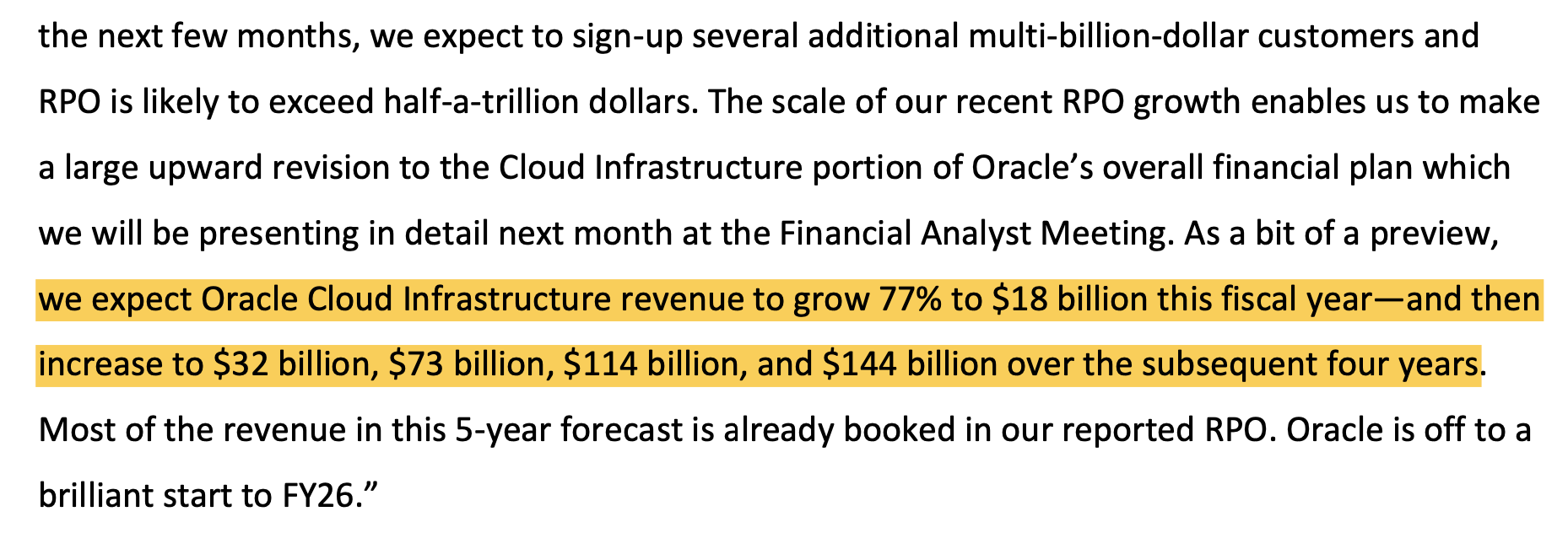

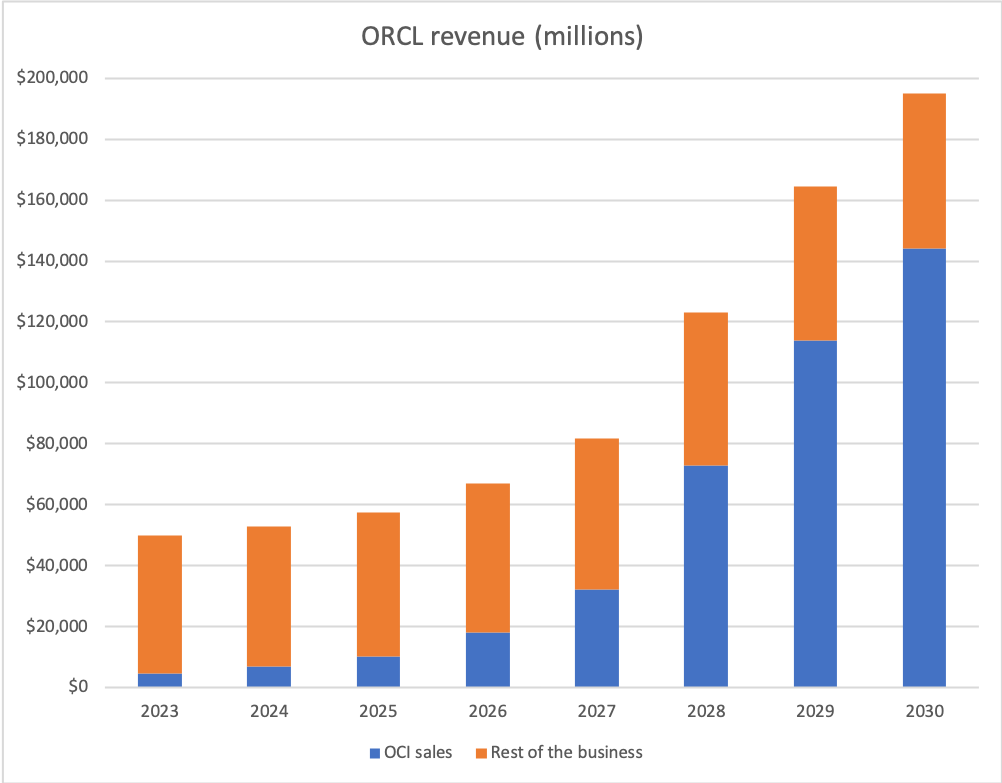

Per ORCL’s recent announcement, if they hit their OCI guidance numbers, here’s what the revenue trajectory would look like (including modest growth assumptions for the rest of the business):

There’s a huge step-up in revenue for FY2028. And a huge step-up in revenue requires a huge step-up in capex. As many have noted, currently ORCL is free cash flow negative as they invest the entirety of operating cash flow as well as incremental debt into capex. In looking to the future, there are many variable and unknowns, especially in a fast-moving space like this:

What we don’t really understand yet is just how much less capital intensity there is to OCI’s cloud growth relative to AWS or Azure. E.g. in the latest quarter MSFT signalled that more than half of their capex spending was for long-lived assets and the remainder on servers. Whereas Oracle have signalled that they do not acquire land and buildings as much as others - they install racks in buildings owned by others. Most of Oracle’s capex therefore is for equipment. I assume similar capital intensity per dollar of incremental growth as in the recent past.

Timing of capex - e.g. I assume the ramp for FY2028 starts in FY2027.

What will ORCL’s margins do? Up until fairly recently ORCL were saying they intended to increase margins out to 2029. But many have pointed out that cloud infrastructure is less profitable. I don’t think anyone outside ORCL really knows what the updated trajectory is likely to be (we might learn more at an upcoming event in October). I assume a steady but moderate decline - I’m not sure how reasonable this is.

I assume moderate growth in the rest of the business.

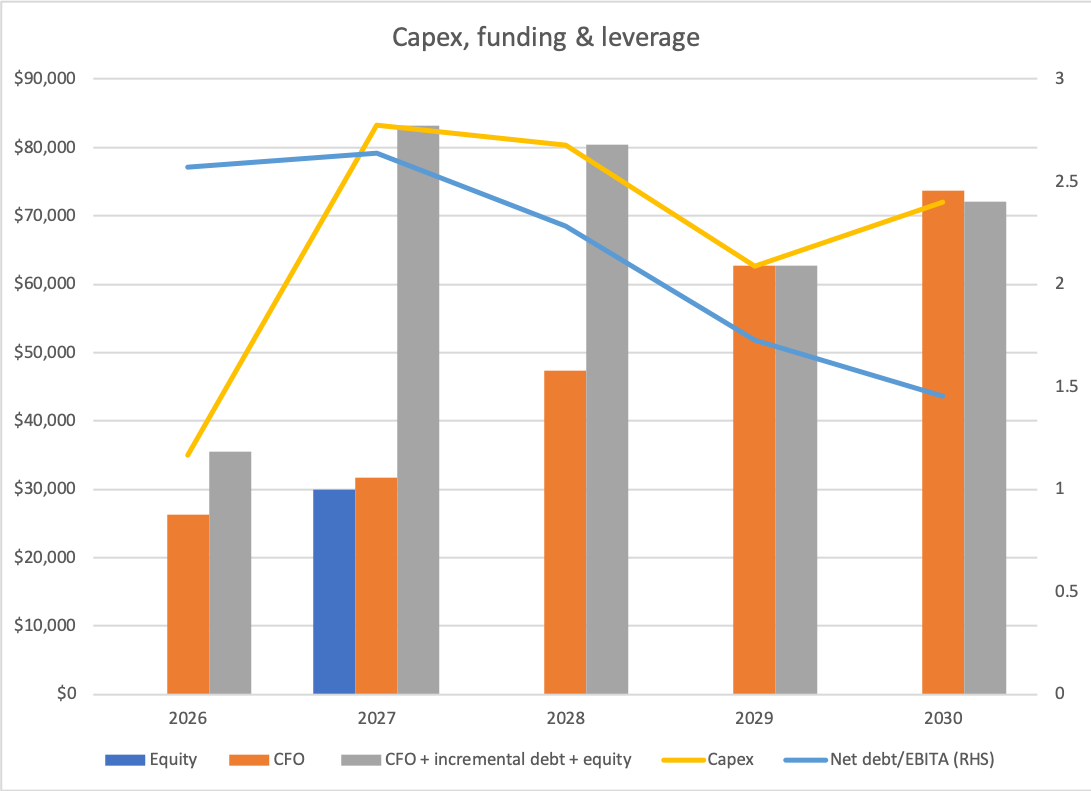

We can argue about the assumptions, but I think I could be on the conservative side (especially on operating cash flow relative to consensus). In any case, to cover the capex for the huge revenue ramp requires a huge amount of cash that ORCL does not currently have. The two obvious choices are 1) debt or 2) debt + equity. Debt alone would take the leverage ratio well over 3x, and that’s feels unnecessarily risky to me. Which is why I think an equity raise of around $30bn could be a good idea, while keeping leverage roughly where it is currently in the near-term:

By FY2029 (i.e. 2028) ORCL might then be back to sustaining investment through cash flow from operations (CFO) alone. This is just an illustration of course - please don’t take it as a forecast.

Perhaps an equity raise was going to happen eventually in the cloud capex arms race and perhaps this could be the first. With ORCL’s market cap now much higher than it used to be ($850bn at time of writing), a $30bn raise wouldn’t be overly dilutive in any case (3-4%). For additional context, ORCL repurchased 1/3 of it shares at an average price of $55 over the last 10 years - issuing a few more again at $275-300 doesn’t seem like such a big deal when seen in that light. What would make the whole episode particularly interesting would be if Larry were to take up his full allocation of $12.5bn. Would there be any precedent for something like that? It’s the sort of thing he might do.

Can OpenAI afford to pay ORCL?

I’d just start by dealing with the obvious: OpenAI does not need to raise $300bn. No doubt they’ll continue raising capital at least in the near- to medium-term, but I think the people making this claim are missing the point. It’s a 5 year contract that apparently ramps from $30bn only starting in 2027. In AI world, 2027 is in the distant future. To state it clearly then: OpenAI does need to grow revenue massively, if this cloud contract is going to be executed as claimed.

As reported by The Information in June, OpenAI had a revenue run-rate of $12bn at that time. To say that’s from a standing start in less than three years is mind-blowing. They’ll be on the hook to pay ORCL $30bn for cloud services in 2027/2028. Who am I to say they can’t hit $40-50bn in revenue by 2028 or $90-100bn by 2030? If they do that, then they’ll have the cash to give ORCL. Moreover, OpenAI’s CEO has previously said he doesn’t expect to make any profit until 2029 - probably in large part because they’ll be handing over such large sums to ORCL. It might sound pretty mad for a $50bn+ technology business to intentionally not make any money - but that’s how moats are sometimes built. Ask Netflix or Uber.

Will they actually do it? I don’t know, but I certainly wouldn’t dismiss it outright as many seem to be doing.

Concluding thoughts

An equity raise might be a sensible move - and if Larry were to take his full allocation it would help investors to gain confidence in this insanely audacious plan. But there are risks. As a shareholder, I don’t want ORCL taking on too much debt and getting into trouble. And while I’m pretty confident ORCL could hold up its side of the bargain, I think the trajectory of OpenAI in the coming years is more of a wild card. If ORCL is going to front the capex, it does need the cash to come in shortly after.

Is there an AI infrastructure bubble? Maybe! I just don’t know. Although the fact everyone seems to be calling it one might suggest otherwise. These are the only things I feel confident in saying:

No one knows what’s going to happen. Not Jensen, not Sam, not the pundits on social media.

Whatever things look like in 5 years from now, they’re likely to look very different to today.

Inference usage is only going in one direction.

I also have questions about the capital and energy intensity of AI infrastructure and the sustainability of current trends - I won’t venture into those right now and I’m no authority on those topics anyway.

So at this stage it’s all starting to get a bit crazy for me, and ORCL is edging towards the ‘too hard pile’. For this reason I’ve stepped back somewhat and dialled down my holding. But not completely. If they execute on this audacious plan, then ORCL may still be a cheap stock, as hard as that may be for people to believe. They would be catapulting themselves into the hyperscale in very short order, possibly even emerging as one of the largest. Moreover, other than a bit of a slow start, ORCL has exceeded my expectations at every step. I’ve had to revise up my expectations constantly. The next step is to listen to what ORCL have to say at the financial analysts meeting at AI World in October and reassess from there.

Thanks for reading. As always, get in touch if you have any comments or quesions.

This is a gift of an article for anybody interested in Oracle.

Fearful when others are greedy?