BMW 2026: Entering the Final Straight

After eight years of flat volumes, a return to growth might finally be coming into view

Friends of NFTBC

Being an automaker is hard, really hard. Which is why there aren’t many financially successful automakers and why investors generally avoid the sector altogether. If you want to learn about what makes BMW different - please check out my free post here:

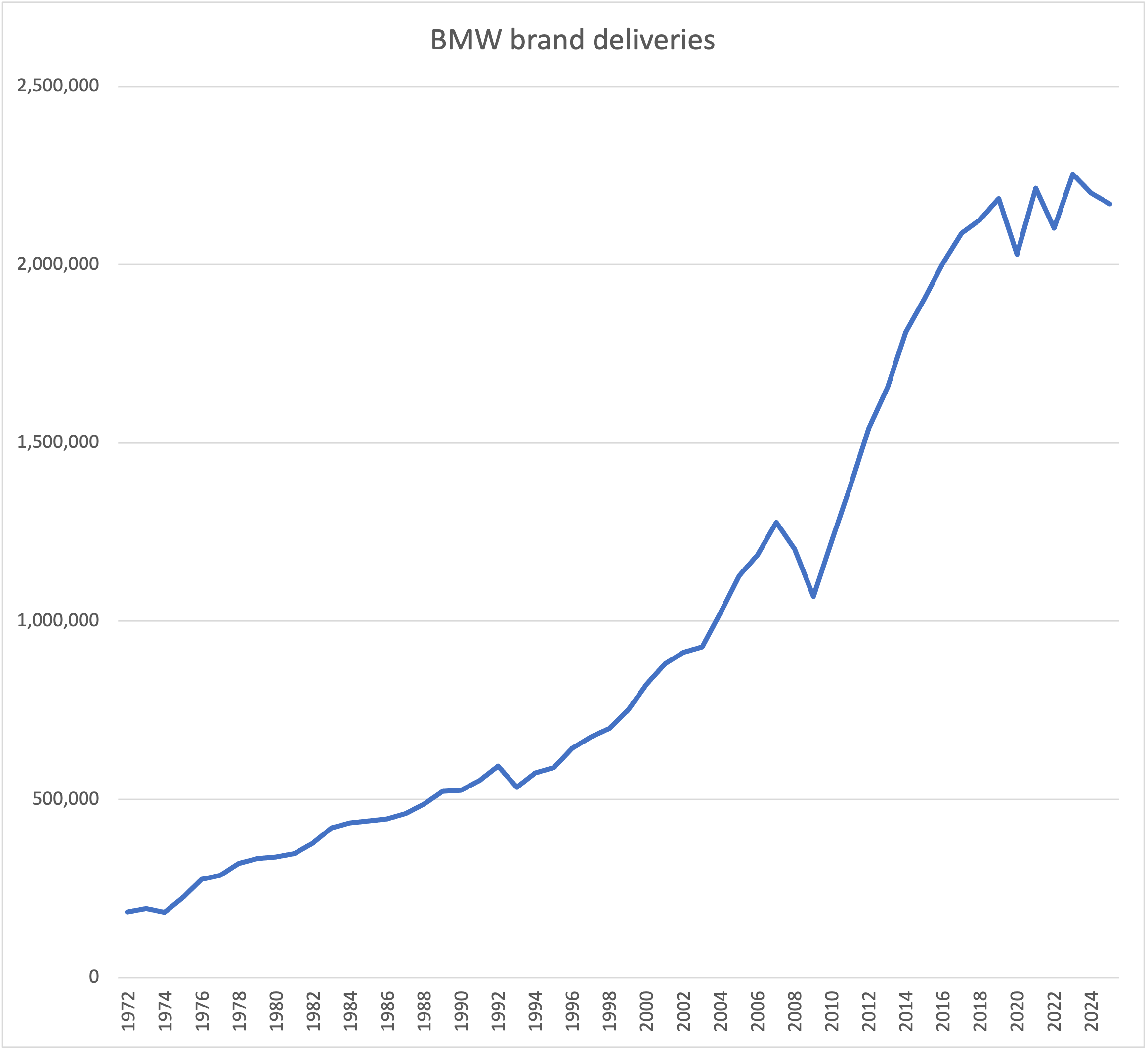

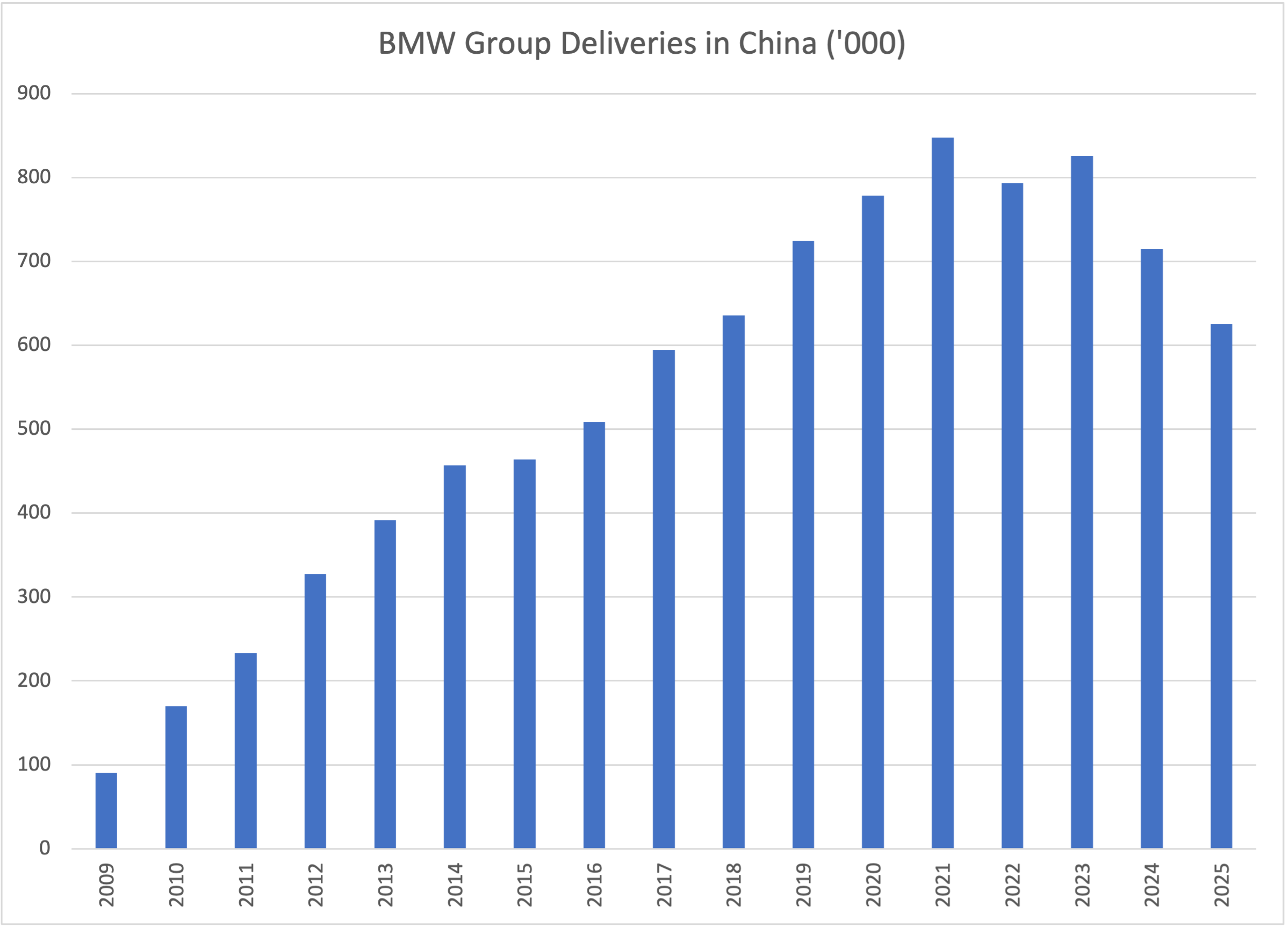

My purpose with these occasional BMW posts is to check in on the company’s progress as it undergoes a historical reinvention. If I’m right about BMW, then the company will soon enough resume its longer-term trajectory of growing volumes with a relatively steady cadence. This follows a near-decade long period of treading water:

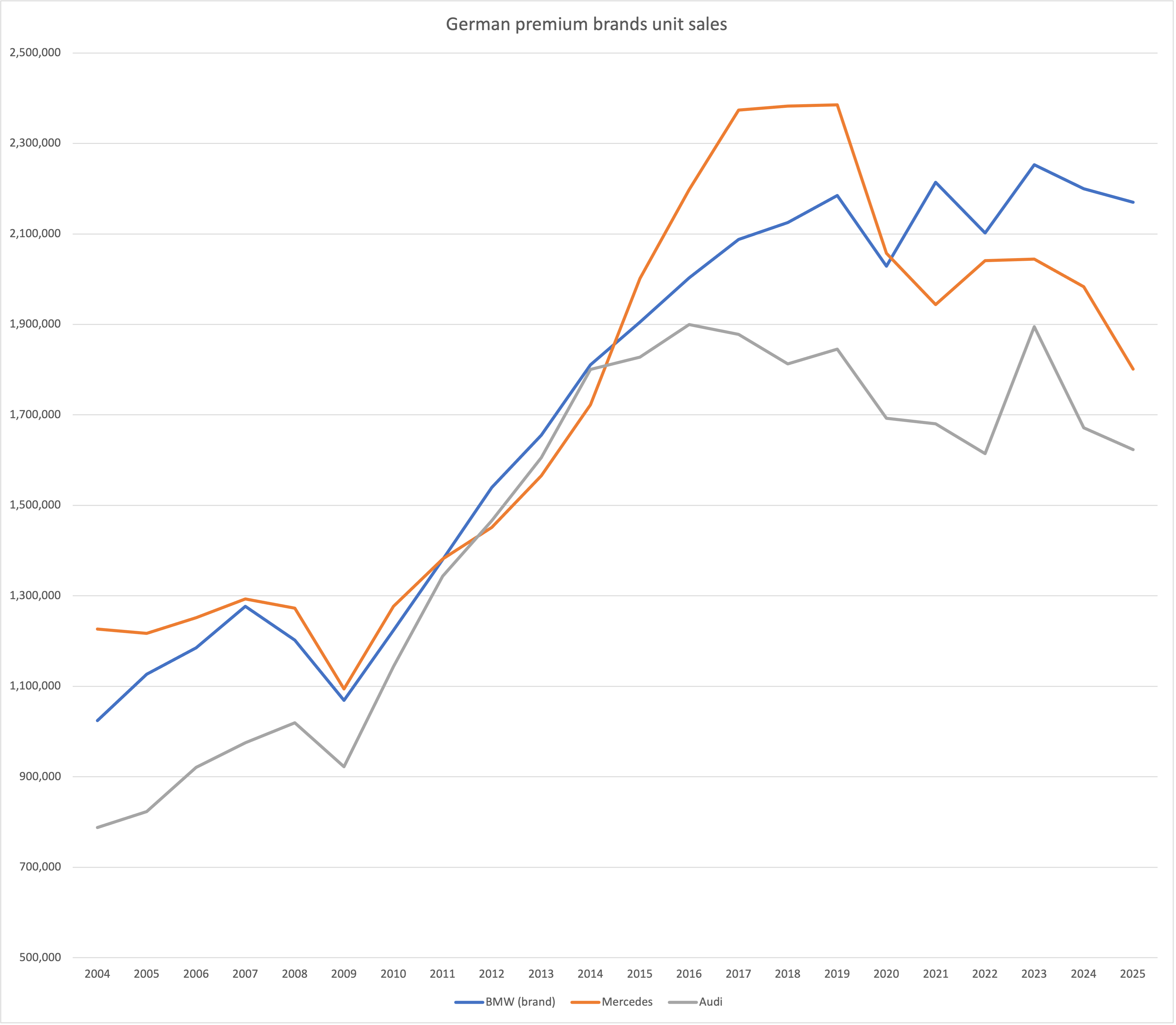

So what happened in the last decade? In addition to global car sales peaking around 2017, two additional factors weighed on performance. These are: 1) Tesla stepping up from ~100,000 premium BEV units in 2017 to ~1.6m in 2025. And 2) a toughening of conditions in China since 2023 from increased local competition and slower business in the high-end segment. While BMW is now well ahead of other legacy carmakers in electrification, from ~2017-2022 they didn’t have a strong answer to Tesla. And from 2024, BMW’s outgoing BEV portfolio is showing its age against fast-moving Chinese competitors. Together, these two headwinds have depressed annual volumes by hundreds of thousands of units. Even still, BMW has done significantly better than its two closest peers:

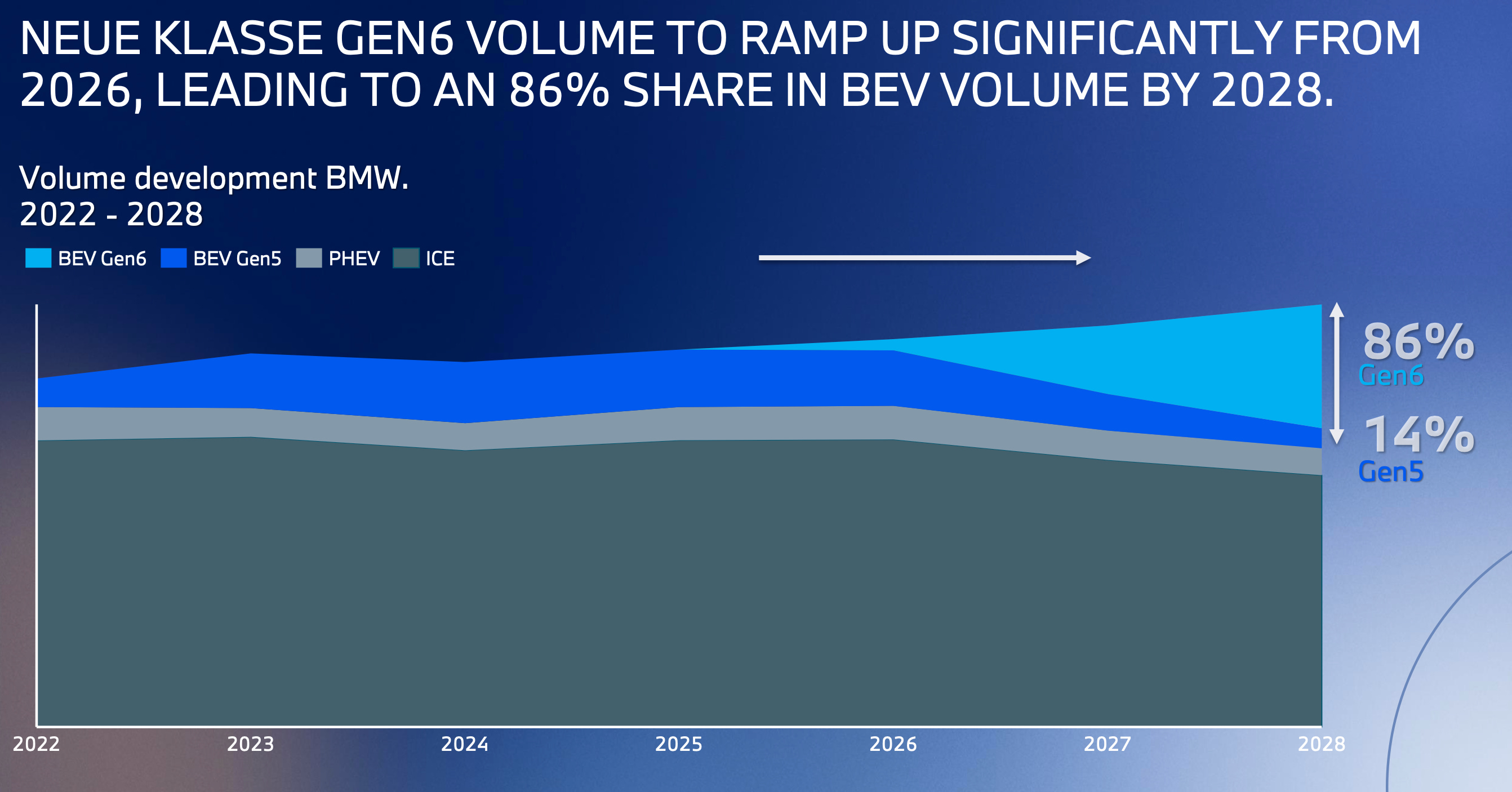

The good news, as I have discussed elsewhere, is that BMW is a forward-thinking business and has spent some years reinventing its product portfolio for the future - if they get it right, the headwinds of recent years seem likely to fall away. Innovations include a Neue Klasse BEV-first architecture as well as suite of new technologies, new design language and important unit cost reductions. In addition to all-new Neue Klasse launches, over the next two years BMW is also carrying out unusually extensive mid-cycle refreshes that incorporate the new technologies - the result is a complete overhaul of the product portfolio in a very short period of time, 40 models in all. We have been told that some existing models (such as the 7 Series) will emerge as substantially new cars. Importantly, the Neue Klasse innovations apply across all drive variants, not just BEV.

Deliveries of the first Neue Klasse model, the new iX3, began in Europe about a week ago, while BMW unveiled the upcoming electric 3 Series (i3) just today:

The launch model will be the i3 50xDrive - much like the iX3 launch model with front and rear motors. The specs are impressive, including 560 mile (900km) WLTP range (BMW estimates 440 miles EPA range). If they follow the iX3 strategy, pricing will be no higher than the equivalent 3 Series ICE/PHEV models. This seems likely to be a highly competitive package - and that’s before BMW’s claimed differentiation on unique driving dynamics (see prototype test drive here). There are more model announcements coming up in the next few months, including the China-specific long wheelbase iX3, the new 7 Series, a new X5 as well as different i3/iX3 variants.

[NFTBC does not give advice - please do your own research. I currently own BMW shares].

Financials and Expectations

All told, we can expect a wave of news, journalist previews and such things throughout 2026 but we’re only in the early stages of deliveries and rollouts around the world. For this reason 2026 is too early to expect a positive financial impact - this is more likely a 2027 story.

2025

You can find BMW’s 2025 year-end materials here.

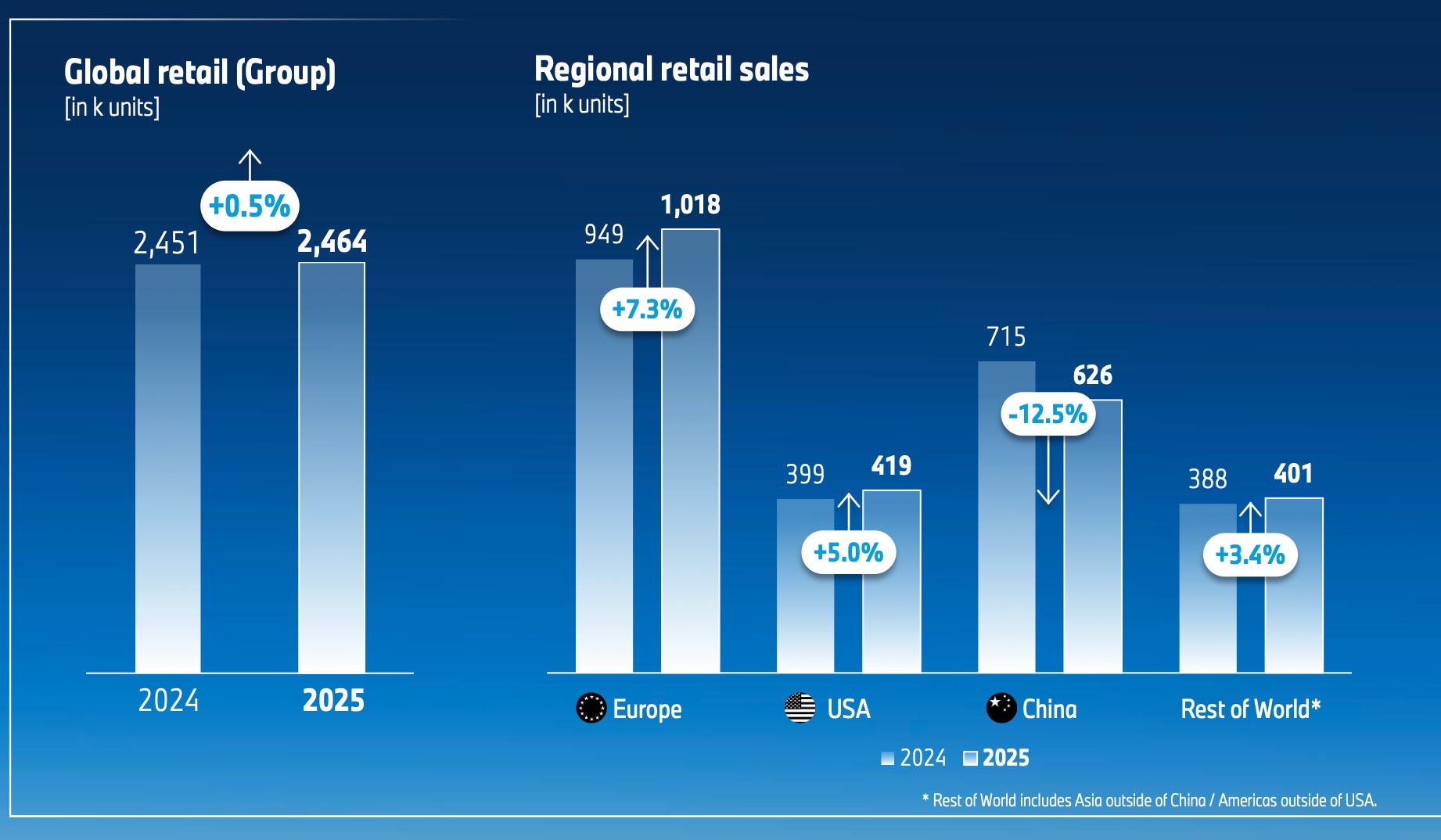

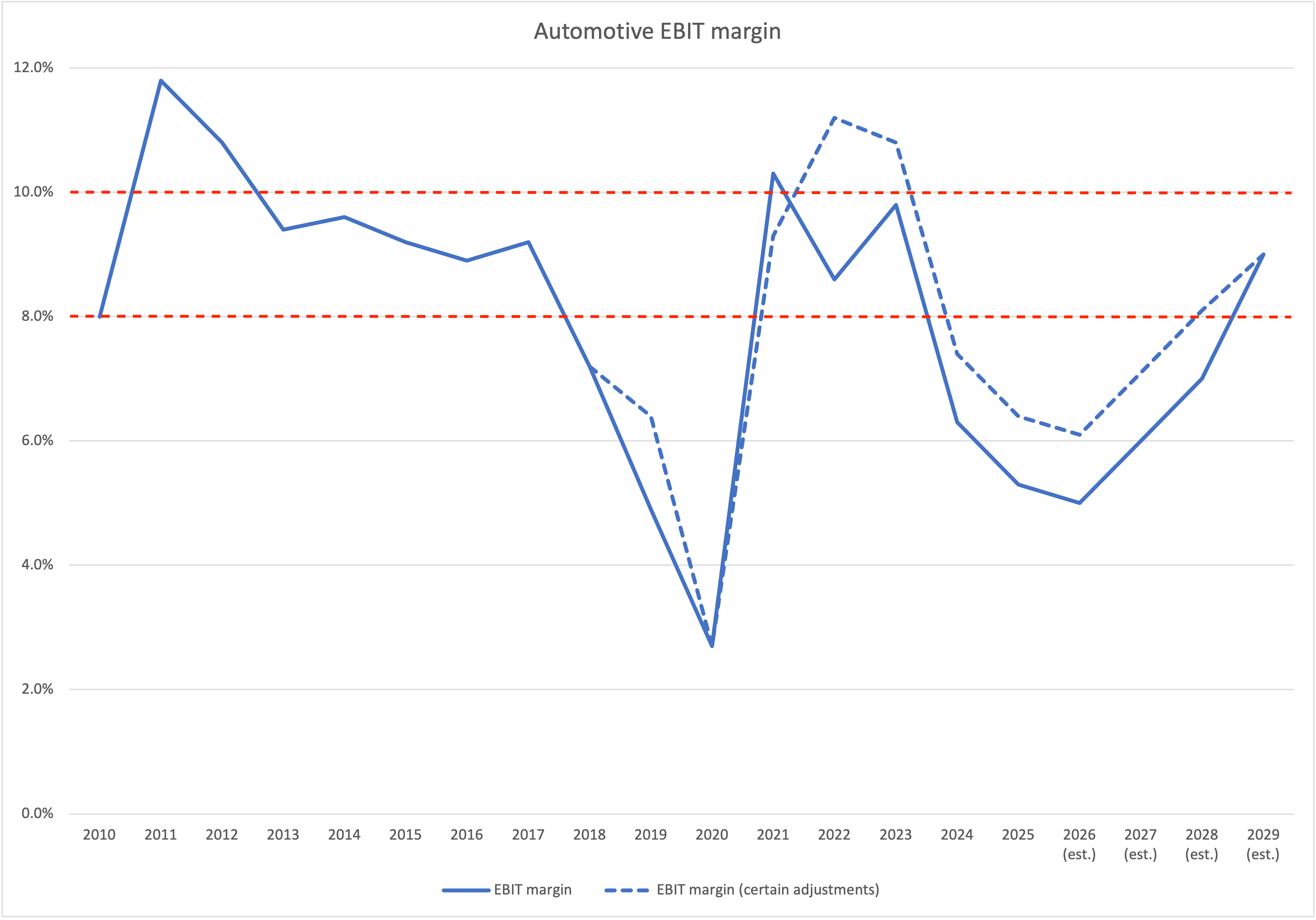

Briefly, 2025 was actually an unremarkable year financially speaking - stable group volumes, stable group margin and moderate increase in EPS. For the most part, BMW came within its outlook set at the start of 2025. But this masks a good deal of shifting beneath the surface:

Notably, performance remained strong outside of China. Automotive revenue of EUR 117.6bn was down 5.9% on FX and pricing (~1.7pp), while Automotive margin declined by 1pp to 5.3%. Excluding the effects of new 2025 tariffs as well as the non-cash BBA purchase price allocation, Automotive margin would have been 7.9% which is just below the strategic target of 8-10%. Along with tariffs, China and fluctuating effects from investment levels, there’s a lot of noise in BMW’s margins currently.

China

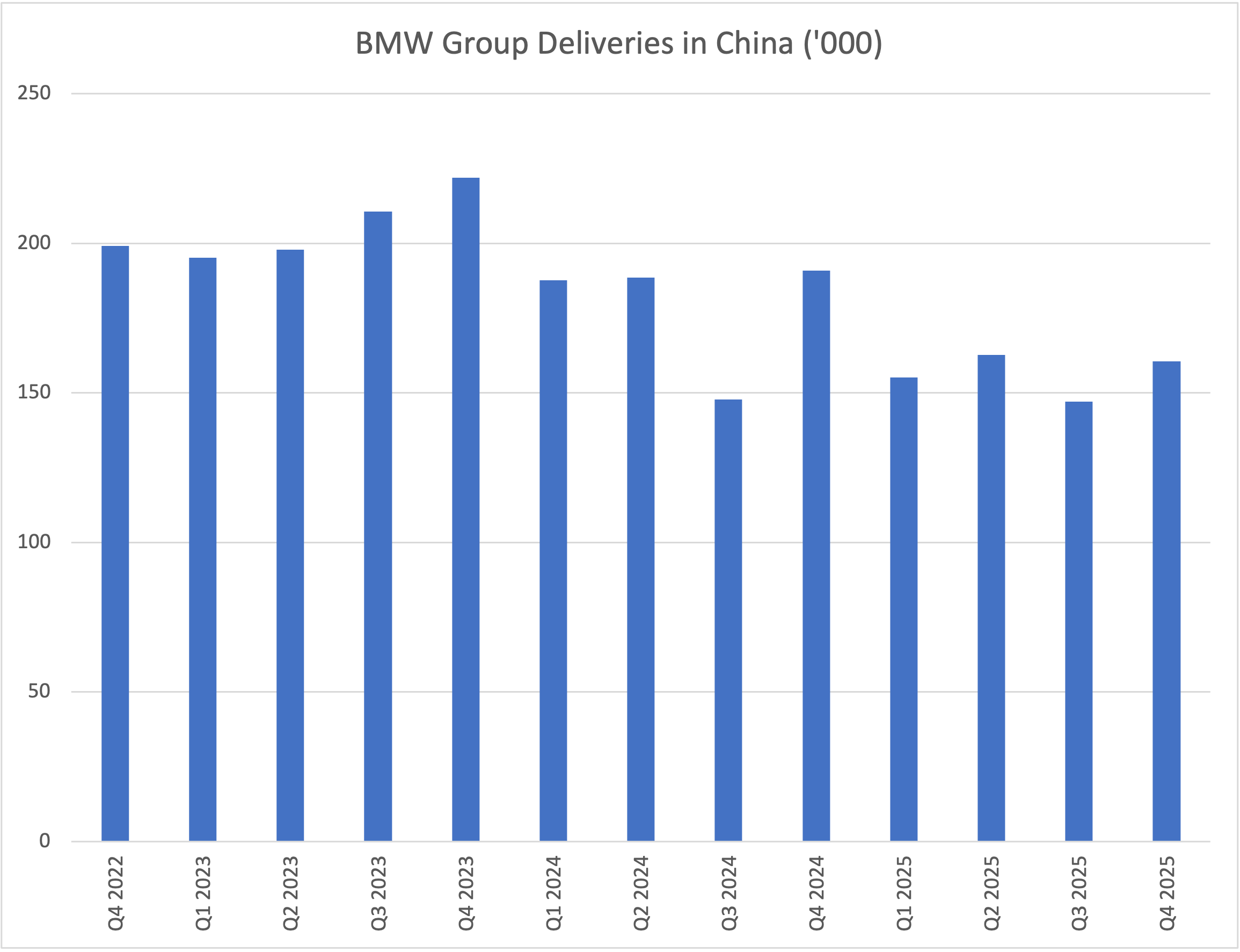

A year ago, BMW was hoping to be flat in China for 2025. In the end, the market continued to deteriorate in the first half, leading BMW to implement further pricing and product measures to stabilise sales. This was in addition to a thorough restructuring of the BMW China dealership network. Per BMW these various measures are starting to be more effective now and they have stabilised at around 50,000 units per month for all of 2025 - this has continued into the first two months of 2026. Additionally, per BMW, pricing has now stabilised since Q3 and even turned positive. Their current expectations are for flat sales and profitability in 2026, which would be a significant improvement on 2025 - and this is before Neue Klasse launches in China towards the end of the year. Things could, of course, get worse again - but for now the outlook is stabilising:

The German automakers certainly capture a good deal of attention currently regarding their recent performance in China. For their part, BMW have spoken about the prospect of increased local competition in China for a number of years, which I think dispels the sorts of claims you hear about the company being strategically blindsided:

The industry is facing a period of profound change. The BMW Group is not about to turn its back on its core business of building and selling premium cars and motorcycles, but the competition is getting tougher. New economic superpowers such as China and India offer opportunities and risks in equal measure. In the future, they will not only represent sales markets but at some point - probably not long from now - will also step up as providers of competitive products.

- The Next One Hundred (BMW’s 100th anniversary book, published in 2016)

When you look at the Chinese market, then the first thing you must recognize this is by far the largest car market in the world. And all along, it was clear, the largest car market in the world will be highly competitive, highly innovative and, of course, dominated by the largest local players. So what happened and is still happening in this market is not a surprise. It’s normalizing. So when you say normalizing, that means there is competition in a saturated market, like we have in Europe and in the United States.

- Oliver Zipse speaking at BMW’s Annual Conference, March 2026

What matters next, is what they do about it - and preparations actually began some years ago. It’s abundantly clear BMW is upping their game: “High local content, super innovative and highly competitive”. Chinese reviews for the iX3 prototype seem to be similarly positive to European/American ones so far - we’ll see how it goes.

2026 Outlook

BMW have left themselves a fair bit of wiggle room on guidance for this year, briefly:

Group deliveries flat (in BMW-speak that could mean +/- a few percent)

Automotive EBIT margin 4-6%

Automotive free cash flow “more than” EUR 4.5bn

Group EBT down ‘moderately’ (could mean ~10% in BMW-speak)

Continuing buy backs (currently reducing share count by ~3% per year)

Notably, Automotive margin assumes a 125bps tariff headwind this year (vs 150bps in 2025 and 175bps annualised in H2 2025). BMW are working on the assumption of finalised/implemented EU-US and US-Canada-Mexico agreements by July, but the outlook also includes mitigations if these do not materialise. Note that the 125bps (if it happens), seems to imply a still lower annualised rate for 2027. The outlook apparently does not appear to include the possibility of a negotiated exemption from the EU-China BEV anti-subsidiary tariff of 20.7% that BMW currently faces on imports from China into Europe - recent reports suggest that such a negotiation is ongoing following a similar deal struck by VW. I would estimate this could be around a 30bps margin benefit if it comes through.

The other principal margin headwinds would include lapping some of the China measures from 2025 as well as increased depreciation and amortization from prior investments as new products come to market. Partially offsetting this is the ongoing ramp-down in R&D expenditure - in 2025 the R&D ratio was 6.2% as against a strategic corridor of 4-5% which BMW intends to return to by 2027.

One thing to keep an eye on is consumer behaviour surrounding the ongoing launches. It’s easy to envisage a scenario where purchasing is delayed due to the significant upgrade in capability coming from newer models. Partly as a result of product cycling, BMW is not projecting an increase in BEV share for this year (18%).

Longer-term outlook

As I’ve noted previously, 2026 is a year of transition at BMW. We should not take it therefore as a point from which to draw strong inferences about the future. I’m currently looking at BMW on a multi-year view to capture the future effects of all the efforts currently underway.

Frankly it’s pretty tough to model BMW with precision, but nevertheless I think we can make a solid case directionally - and that’s good enough given where the valuation is (7.5x consensus EPS on depressed margins, also see here). BMW confirmed this week that they intend to return to their strategic Automotive margin target of 8-10% within the ‘medium term’ - and for the reasons I’ve discussed previously I’m inclined to take this as a sort of North Star given its centrality in how they manage the business. While they haven’t given a specific timeframe, it’s a very fair bet they are planning around this internally. Four years, or year-end 2029, seems like a reasonable point to take as ‘medium term’.

So I think you can reasonably assume a trajectory something like this:

Naturally, the stronger the growth in volumes, the easier and faster it will be to normalise margin through operating leverage. Note that by 2029 the BBA purchase price allocation effect (dotted line) will drop out following completion of the allocation. With a margin normalisation, you don’t have to be especially aggressive on your revenue growth assumptions: 5% seems reasonable from a combination of volume/price/mix:

Am I being wildly optimistic? BMW have a soft target of 3m vehicles a year in 2030 which would imply something in the region of 5% annual volume growth 2026-2030.

Whether or not they do indeed achieve this remains to be seen. But one thing is emphatically clear - they do intend to grow and this is what they’ve been planning for.

Thanks for reading