BMW AG - a Deep Dive (Part I)

Bavarian exceptionalism / why BMW is not like other car companies

Friends of NFTBC, welcome to Part I of deep dive #4 - Bayerische Motoren Werke AG.

I’d like to start by thanking you for giving this one a go. All serious investors know that automakers are to be avoided. Cars are commodities with no pricing power. The industry is too competitive. It’s subject to boom and bust. It’s too unpredictable. The margins are too thin. Car manufacturers have no ‘moat’, we are told. Moreover, disruption and trade wars are afoot. Actually I agree with all of this! But in the messy real world, there are usually exceptions. As I shall endeavour to explain, BMW is a rather unusual car company. It behaves differently, and has done for a very long time. And different behaviour results in different outcomes - even in an industry as lousy as this one. This will be the topic for Part I.

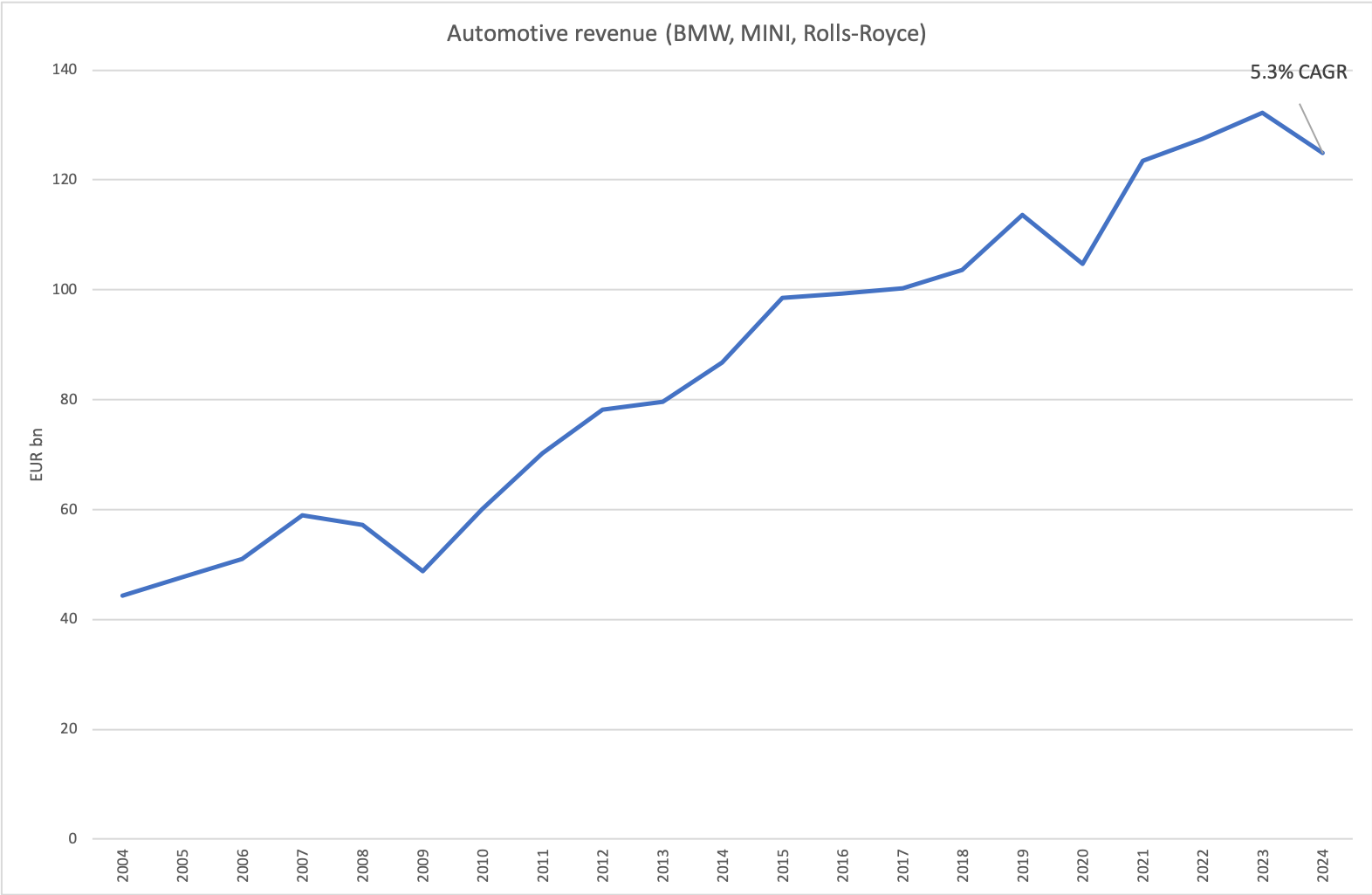

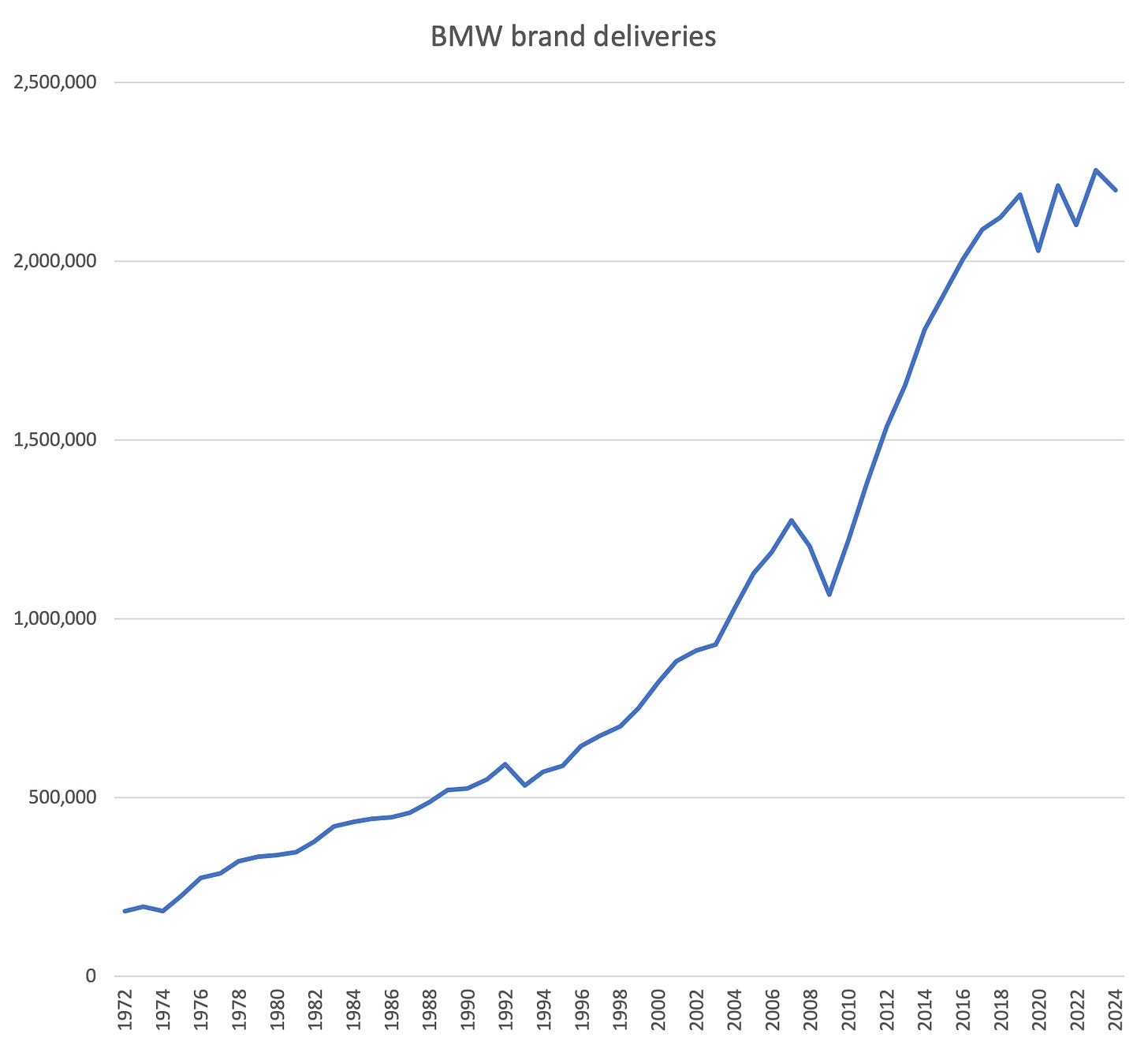

BMW’s car brands (BMW, MINI, Rolls-Royce) have compounded their combined revenue at over 5% organically during the last 20 years, with group EPS compounding at 7%. While not hyper-growth, it is comparable (if not better than) numerous consumer businesses that trade at 10-15x turns higher.

BMW has also averaged a group EBIT margin of almost 9% over the entire period. Take out the GFC and COVID (when they still turned a profit, by the way) and it’s nearer 10%. The company has been profitable every year since the 1960s. Yet, like those of most automakers, BMW shares persistently trade as if the company’s prospects are terminally impaired. Are they though?

Global car production peaked in 2017 and during the same time we have seen large-scale adoption of electrified vehicles (BEV and PHEV), new competitors, COVID, supply shocks and inflation. Most legacy automakers have been shrinking in such a tough environment and adjusting their footprint to the new reality. Not BMW, which continues to invest in growth, including opening a sizeable new plant in Hungary later this year while continuing to invest in the US and China. In this post we are going to explore the various reasons why BMW is a much better car business than almost all the other legacy players and how it will likely continue to avoid their fate.

So why am I publishing this now? In a few months, BMW goes live with its most radical and strategically important product and technology reinvention in decades - Neue Klasse. The implications for the business are potentially significant, yet currently very much under the radar. BMW have been signalling for several years that they intend to grow their business in the years ahead, and this is how they intend to go about it. In any case, it’s a really interesting time to be thinking and writing about this company, so that’s why I want to do it. I’m not providing any advice or recommendation here and I’ll leave you to make up your own mind as to whether the shares are worth owning, but I am disclosing that I currently own BMW non-voting shares myself.

To briefly address the two obvious elephants that you’ll want to hear about sooner rather than later: if the US automotive tariff situation does not achieve a suitable resolution, I would expect BMW’s profits and shares to come under further pressure - perhaps significantly so. But in this situation, I would be looking to add on a ~3 year view. Why? Because BMW is in a better position than most to adapt - as you will learn, they have a long history of it. Additionally, they already produce as many cars in the US as they sell there, so they’re starting from a strong position. Not many realise that BMW is actually the largest car exporter from the US and given two or three years they can retool the US to be primarily local-for-local, such is China today. Second, China and BEVs: with Neue Klasse, BMW will close any perceived smart technology deficit that exists vis-à-vis the latest Chinese models, while also further augmenting the differentiated authentic BMW driving experience - the very thing that defines the brand. BMW has no intention of competing aggressively in the mass-market in China (or indeed elsewhere) with 'smartphones on wheels’, focussing instead on its own premium niche. The company’s ambitions are for a modest 3-4% market share in China, which is actually a bit higher than where they are today.

In the end, I decided to break this post up into more than one part. It’s an interesting business in an interesting and topical industry - there’s lots to say. But even then, I’m not going to cover everything - just those matters that are most pertinent to what I’m trying to convey. I’d be delighted if you find my writing interesting enough to read the whole thing, but otherwise do please skip to the parts most relevant to you or plug the whole thing into your LLM of choice (if you don’t mind missing the nice charts and pictures, that is).

For newcomers, I would encourage you to check out the NFTBC User Guide for a bit more information about this blog and how I write about stocks - this will not be an especially typical automotive research note. Get in touch on here or through X if you have any comments or questions, and please share this post with anyone you think might be interested - especially those interested in cars!

As always, please do your own research.

Thesis

I believe BMW to be a much better business than generally assumed. In fact I don’t think it unreasonable to call BMW a good business, if by good business we mean one that is financially safe, likely to produce a satisfactory return on capital and increase its through-the-cycle earnings per share at least in line with inflation into the future. You could also say BMW is a great car business.

To boil it down, here are the characteristics that I believe make BMW a good business and a great car business with enduring advantages. In isolation any single attribute would not be enough, but they all compound together to create a Munger-style lollapalooza:

Authenticity: BMW’s cars look, drive and feel a particular way - a complex weave of creative design, engineering and brand mastery. This applies to each of the group’s brands: BMW, Rolls-Royce and MINI. Vanishingly few car brands are as good as BMW at this, yet in the premium and luxury segments it’s perhaps the single most important characteristic and it’s extraordinarily hard to replicate.

Consistency: They’ve been executing on their authentic brand strategy since the 1960s with unwavering consistency. Just one example - you can pick almost any BMW produced in the last 60 years and be able to easily identify it as a BMW side-on without seeing the logo or famous grille.1 But consistency goes beyond authenticity into other critical fields too, such as manufacturing - BMW is consistently among the very best at efficient manufacturing and high quality control.

Adaptability: BMW is an organisation and brand that bends rather than breaks. Its history is one of constant reinvention and creating new futures that simultaneously remain consistent and authentic - new markets, new niches, new technologies, new regimes, new pace of change.

Independence: The company takes pride in making up its own mind and doing things its own way - resisting the pressure to conform has been a tremendous advantage over time. BMW largely sets its own agenda rather than taking cues from others. The company also guards its operational independence.

Flexibility: BMW insist on making higher than average profit margins (specifically 8-10%), because doing so provides strategic flexibility - flexibility to invest more or to weather storms, for example. And to be clear, the primary reason for high margins is flexibility itself - shareholder value is an indirect outcome. But flexibility for BMW is much more pervasive than that - flexible manufacturing lines, flexible supply chains and flexible labour.

Credibility: When BMW’s management make claims, they’re generally believable. There’s no fluff, bravado or window dressing. If they say they’ll meet their fleet emissions target, they’ll do it. When they said the iX would go into production in three years, it did. When they said the i4 would prove the sceptics wrong, it did. If they say Neue Klasse will be their most impactful product development in decades, it’s a bet worth taking. Their annual financial guidance is generally quite good too, although not infallible given the industry dynamics - but when they say 8-10% strategic operating margin or €7bn in automotive free cash flow they really mean it.

Long-termism: Underpinning all of this is the support of committed family owners, who also impart long-termism throughout the organisation - brand strategy (decades), designs (intended to be fresh 15 years in the future), far-reaching technology platforms (many years to payoff), employee tenure (often decades), manufacturing footprint (decades), strategic financial targets (decades).

Now here are some direct predictions for you. In 10 years from now:

BMW will sell at least as many cars as it does today

Revenue per unit will, on average, continue to keep pace with inflation, as it has in the last 10 years

BMW’s automotive margin will be 8-10%

Yet BMW’s €46bn market capitalisation paints a rather different picture, with a normalised automotive free cash flow yield of >12%.2 And that’s before you factor in:

a financial services business with a book value of €17bn and profit of €2-2.5bn

A growing motorcycle business with profits of €150-180m

Net financial assets of €46bn

The full value of Rolls-Royce Motor Cars - of comparable quality to Ferrari, it could be valued at more than €30bn [please check out my separate Rolls write-up here - I do not intend to revisit it in detail here]

Now, in practise, I can’t imagine BMW ever spinning-off Rolls-Royce purely in an attempt to juice the share price - it’s not their way. But the brand is performing exceptionally well and they’re supporting it with additional investment - so the story might not remain entirely unnoticed forever. Perhaps more importantly, BMW has been moving with increasing aggression towards allocating its giant cash pile to share repurchases - given BMW’s well-known financial conservatism, this is a major development and likely to contribute to EPS growth in the coming years in a way that is altogether new for the company.

In addition to all of this, Neue Klasse brings optionality. Rather than merely an individual model, Neue Klasse is a radical new design language and suite of technologies that will rapidly proliferate both upwards and downwards through BMW’s portfolio starting later this year including into all drive train variants. Neue Klasse also brings with it BMW’s first dedicated BEV architecture. Notably, as regards the BEV transition, BMW is already far ahead of other legacy automakers with existing models, and that’s despite the compromise of BMW’s shared CLAR architecture rather than dedicated BEV architecture - a compromise others peers have chosen not to make. Yet Neue Klasse will take BMW BEVs to the next level in terms of technical capabilities, driving dynamics and cost structure. Distinctive radical design language, that is somehow less divisive will still be true to the brand. And BEVs that are fun to drive in the way BMWs are supposed to be. If they can really pull this off, then perhaps the group will return to unit growth rather than merely treading water. In June 2025, journalists were given the chance to test drive the first pre-production Neue Klasse model (iX3). I asked ChatGPT o3 Pro to read all of their reviews and give me an unbiased breakdown. Here were the principal conclusions (left unedited by me):

The iX3 feels “like a BMW – just a fabulously good one,” combining familiar dynamics with a genuinely new EV experience

Reviewers unanimously call it a step-change over the outgoing iX3 and a convincing first proof of BMW’s Neue Klasse platform

Journalists broadly agree the upcoming iX3 delivers the dynamic sparkle many felt was missing from earlier BMW EVs while leap-frogging rivals on efficiency and computing power. If production cars mirror these prototypes, BMW’s first Neue Klasse model is poised to reset expectations for an electric premium SUV.

Just days ago we only had BMW’s word to go on. The signal strength is now increasing. There are video reviews too - here’s one of the widely viewed ones:

One thing to watch closely for is how BMW decide to price these upcoming BEVs. The general assumption from auto journalists is that they’ll price at a significant premium to their ICE equivalents, as is the case currently (~20-25%). However, BMW’s next generation batteries reduce production costs by up to 50% while also significantly increasing range and efficiency (we’ll get into that in Part II) - the point is that BMW’s new head of development has said that cost savings will be passed to the customer. Given that BMW’s first two Neue Klasse models will be in its two highest volume segments (X3 and 3 Series) it will be interesting to see what BEV/ICE pricing parity could do for demand and a possible overall sales inflection.

My best guess is that after Neue Klasse has had several years to prove itself in the market and after tariff headwinds are behind us through policy resolution and/or mitigation efforts, BMW should be able to return to a more historically normal P/E ratio of 10-12x, with automotive margins of 8-10%. This would mean a share price potentially in the region of EUR 135 to 230 by 2029 or roughly +90 to 200% higher than today.

But who’s right here? Are BMW’s prospects permanently impaired? My feeling is that many automotive analysts do actually have an appreciation for the quality of BMW’s management, but don’t ultimately follow through on what that means. For example, one major sell-side bank’s terminal multiple implied terminal EBIT growth at BMW of minus five percent (in their own words) - but without any explanation, just because… My goal with this post is to shed a little light on these questions through a study of this fascinating company.

Some of you will understandably want to hear more about tariffs, the Chinese domestic market and Chinese BEV producers. My approach is to deal with that stuff later on after we’ve heard about the company. All I’ll say for now is that I do not consider these to be material risks to BMW’s business model on a medium-term view, once you consider the nature of the company, its flexibility and competitive position.

Introduction

The world of automotive investing is a peculiar one. Relatively few investors study the industry in depth these days, yet everyone seems to have strong views about it. While I won’t dwell on this observation, it’s worth highlighting one particularly persistent category error that results from not getting to grips with the nuance: the lumping together of groups of automotive businesses according to the nation from which they originate. For example, sweeping claims are made about Chinese automotive groups in general and it’s the same for German counterparts. Effectively, what we end up with is nonsensical syllogisms: “Chinese automakers are superior to German automakers; BMW is a German automaker; therefore, BMW is an inferior automaker.” As I shall argue, BMW is in a different category altogether. Sure, BMW is German, but it’s also Bavarian. Moreover it’s also somewhat Chinese and American too. BMW doesn’t really behave like any of its peers and that’s what makes it worthy of study, in my view.

Producing and selling modern cars at scale is a mind-bogglingly complex endeavour, from the strategic planning phase, to engineering, to design, sourcing, manufacturing, testing, logistics, sales, brand, marketing and regulation. You would have thought barriers to entry would be high, especially in conjunction with the capital required to make all this happen. Actually, barriers to entry are high and that’s why we’ve historically tended to see a steady net reduction in car brands on the roads over a period stretching back well into the 20th century. Of those that remain, most have been on the brink of bankruptcy at some stage or other, but as large employers and national champions, they tend to receive bailouts rather than be allowed to die. Were it not for government intervention, the industry would probably be less competitive and more profitable overall, I would speculate. And that brings us to the next point - through the operation of ZIRP in the US and state sponsorship in China we have seen capital barriers to entry come down in the last decade and a surge of new entrants into an already competitive field, all in pursuit of BEVs. It seems, however, that the barriers are coming up again - ZIRP no longer exists and even the Chinese government is now acting to staunch the effects of a brutal price war created by its own policies. The window is now closing, and eventually I suspect we’ll be back to some version of business as usual for the industry - and most of the new entrants will cease to exist as independent businesses. High capital barriers to entry - yet competitive and complex.

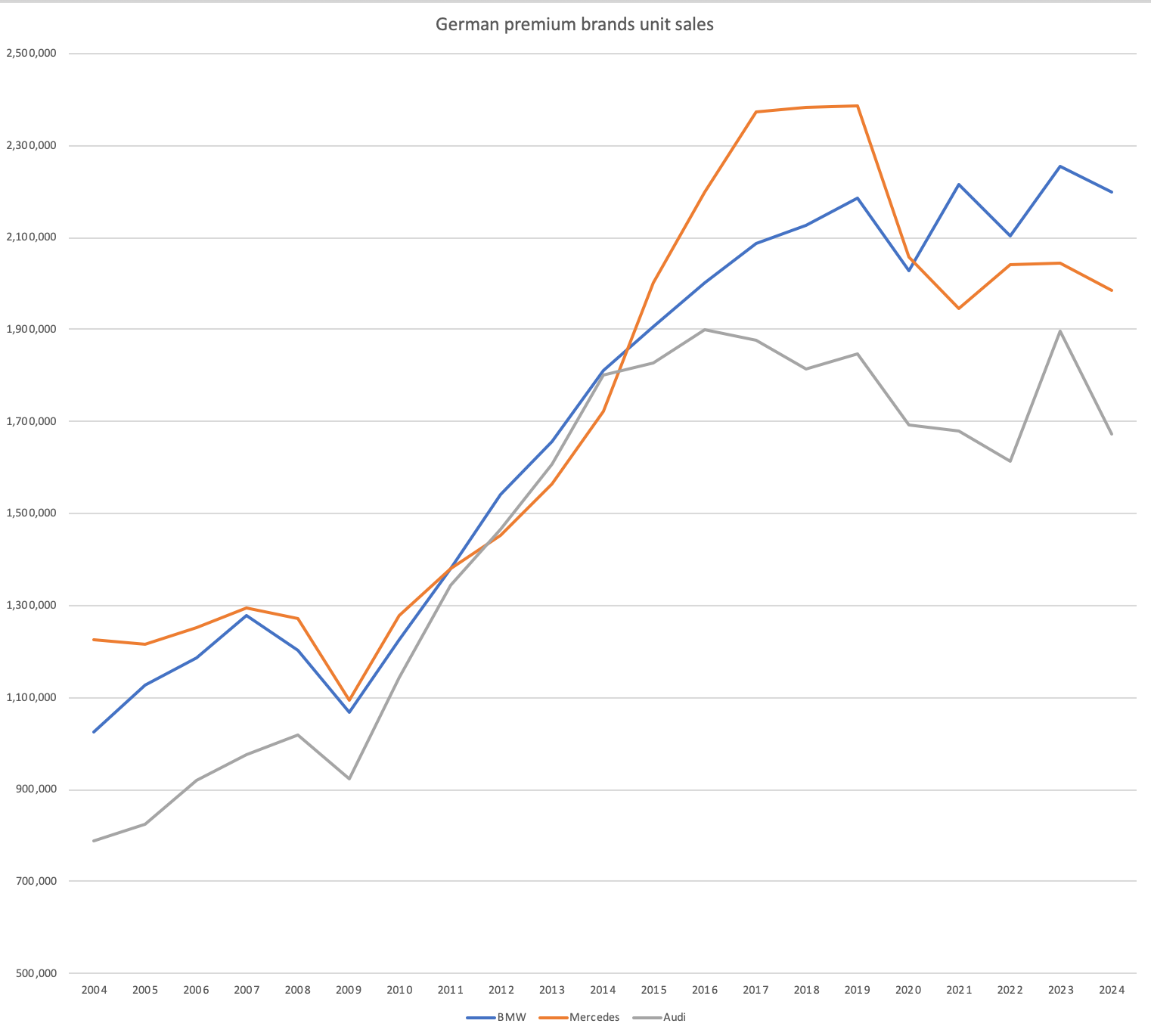

So how is an automaker to deal with this competition and complexity? It’s fiendishly difficult and that explains why so few are financially successful over the long-term. Earlier, I listed seven core attributes that I consider to be central to BMW’s success. None of this is to argue that you won’t find individual attributes at other automakers, but to find the complete set in combination is rare. And that’s how BMW has managed to outperform the sector as a whole and its peers for the last decade (and much longer):

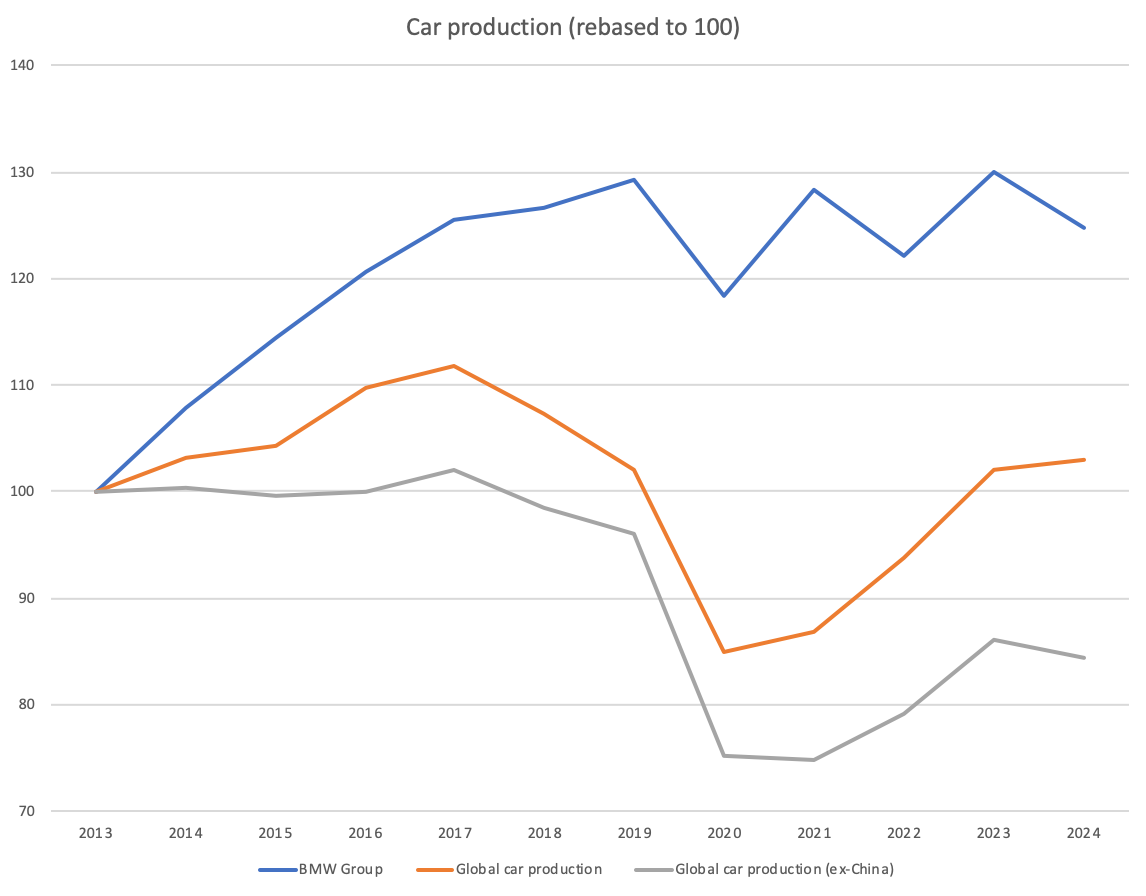

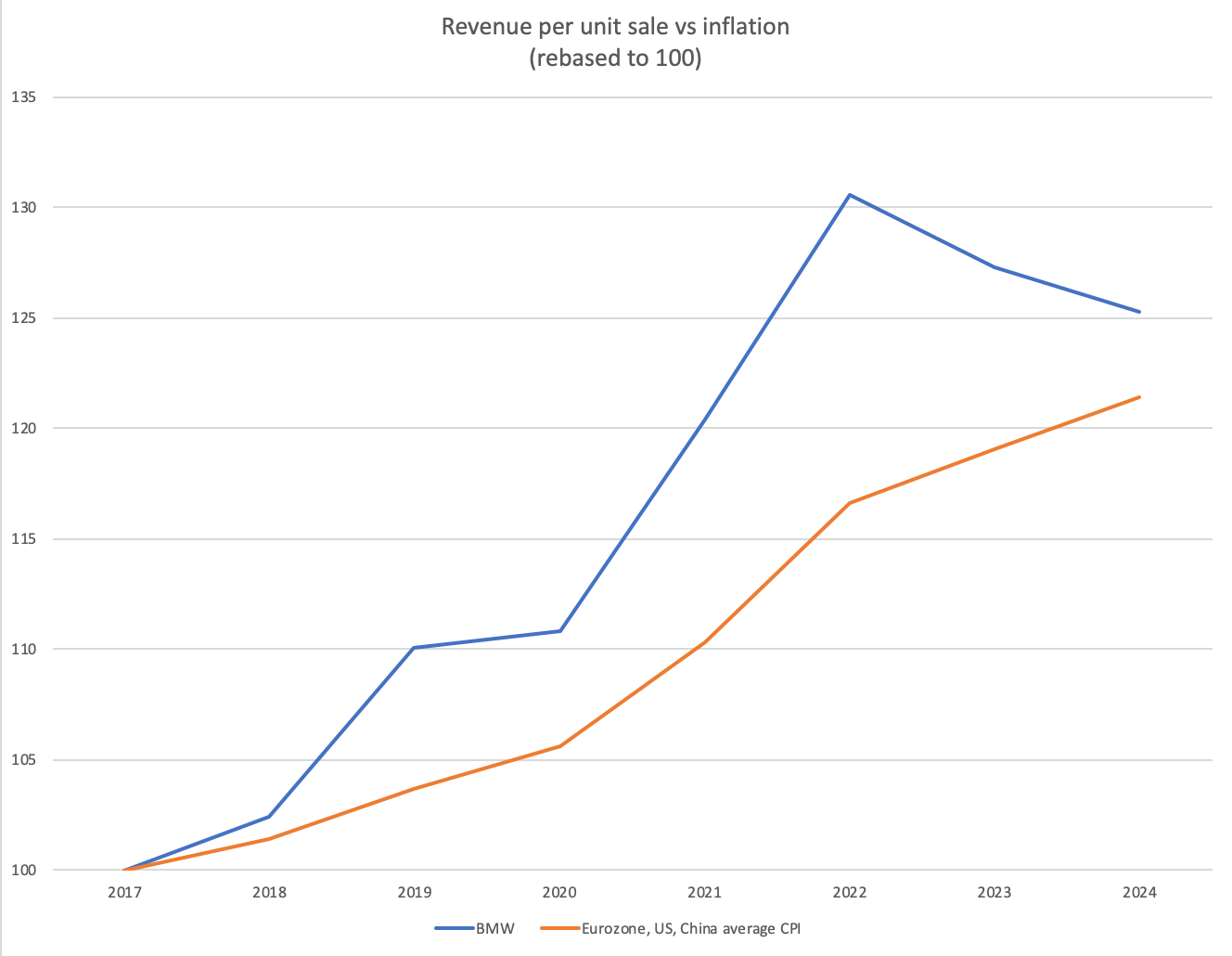

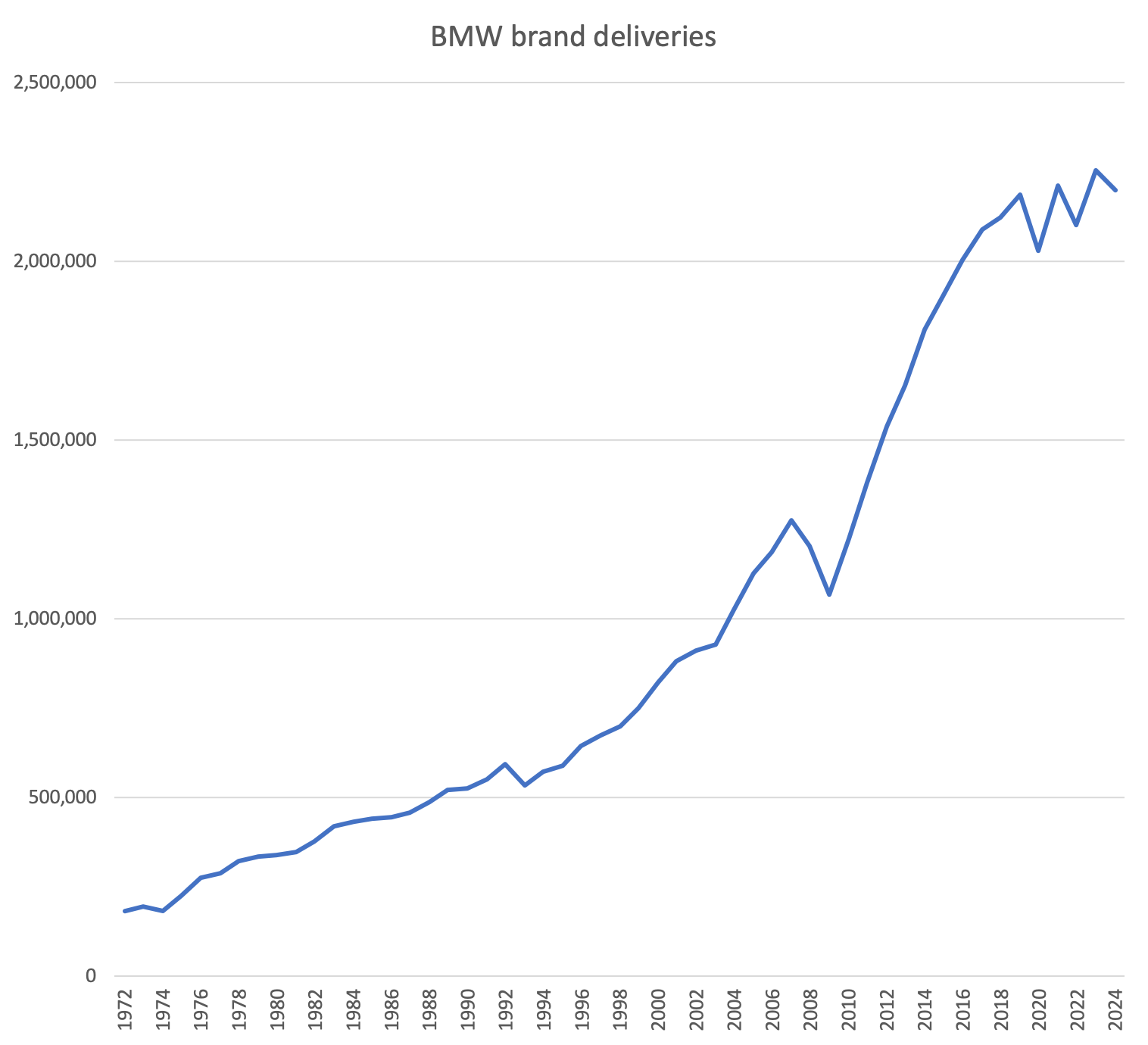

Notwithstanding its outperformance, BMW Group has hit something of a unit ceiling in recent years (we’ll discuss later whether they can resume growth), but that’s in the context of a global market that peaked in 2017 and is now smaller, significantly so in the case of ex-China production. So rather than unit growth, the impetus has shifted to price and mix in recent years:

The common claim is that automakers sell commodities and have no pricing power. Per the typical definition, pricing power refers to a company’s ability to raise prices for its products or services without experiencing a significant drop in demand or without losing customers to competitors. Given that BMW has realised unit pricing above the inflation rate but without any fall in demand, is it reasonable to say that BMW has no pricing power? I don’t think so! Now, some of you may quibble that revenue/unit is down two years in a row - this is true. This reflects normalisation following extraordinary pricing realised during the pandemic era supply chain shortages. Admittedly, some of it relates to the China BEV price war too - it’s up to you to decide if BMW can reassert its market positioning and brand power in China with the upcoming Neue Klasse launches. I think it probably can.

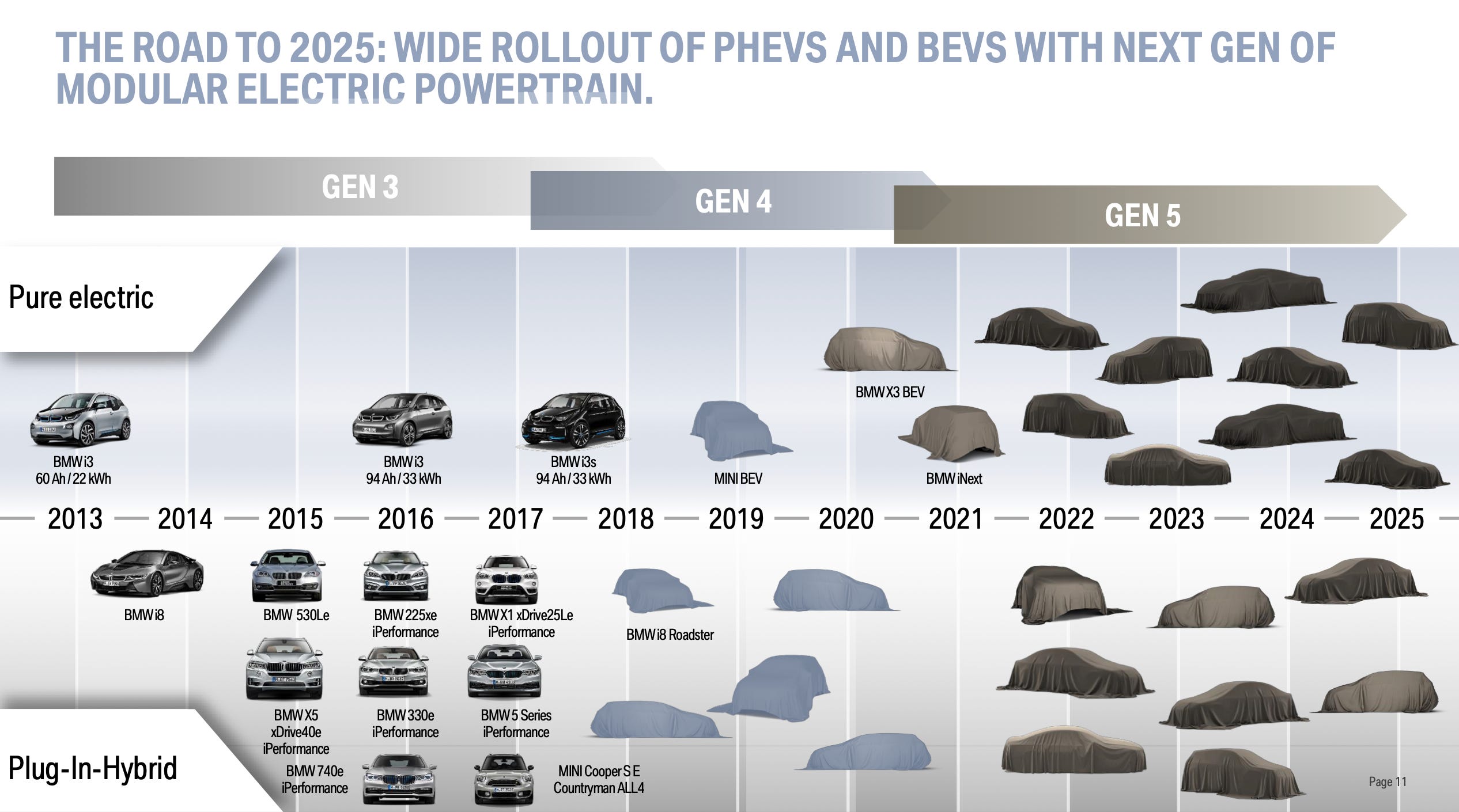

The last decade-plus, since 2013, has been a busy one for the company. Starting with BMW’s pioneering foray into mass-produced BEVs with the innovative i3 (on the heels of Tesla’s own Model S), shortly followed by the company’s first PHEV, the sporty i8. These two experimental vehicles certainly made the company look like an odd ball, to say the least. From 2015, BMW then began to roll out PHEV technologies more widely into its broader product portfolio. But no additional BEVs were forthcoming until 2020 with the original iX3 and MINI Electric, which again made the company stand out, but this time as ‘out of touch’ rather than pioneering. At this time almost all legacy peers were racing to outdo each other by setting increasingly aggressive ICE phase-out dates while rushing out new BEV models to market - BMW went its own way.

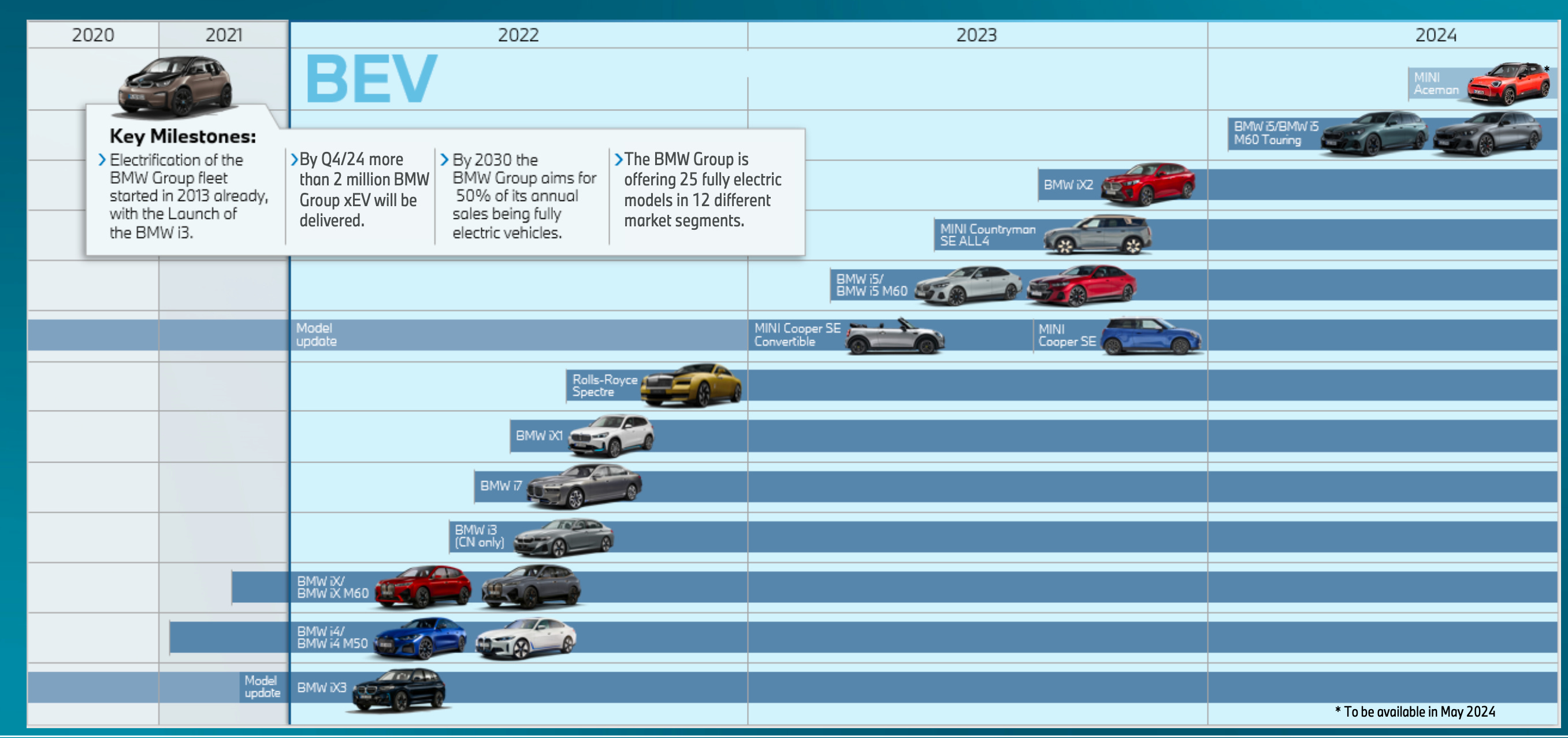

But then, in 2021, BMW finally began its full assault with the fully electric i4, iX, i7, iX1, iX2, Rolls-Royce Spectre, new electric MINIs and i5 all launched on time and in quick succession into each of BMW’s principal product segments.

Remarkably, with the partial exception of the iX, each of the BMW models shares architecture, styling and even production lines with the equivalent ICE and PHEV variants - much criticised in the run-up to 2021 this has proved resoundingly to have been the correct strategy and a nice example of BMW’s various attributes at play - starting with BMW’s independent way of operating. Take the 5 Series, for example, which is BMW’s longest consistently produced model with lineage back to the early 1960s - it’s a brand all in itself. You can buy an authentic 5 Series today, and regardless of the drive variant, it’ll look almost identical (again, consistency). Moreover, it’ll come down the same production line in Dingolfing (Germany) or Shenyang (China) giving BMW the flexibility to produce whichever version the customer desires without having to predict demand in advance or overbuild costly dedicated capacity. BMW’s flexible system to produce different variants down the same line actually originates in decisions made in the 1980s with its Regensburg plant (long-termism), but it’s not to say that BMW’s current drive train strategy is set in stone - they are in the process of adapting once again with Neue Klasse as we’ll get into in Part II.

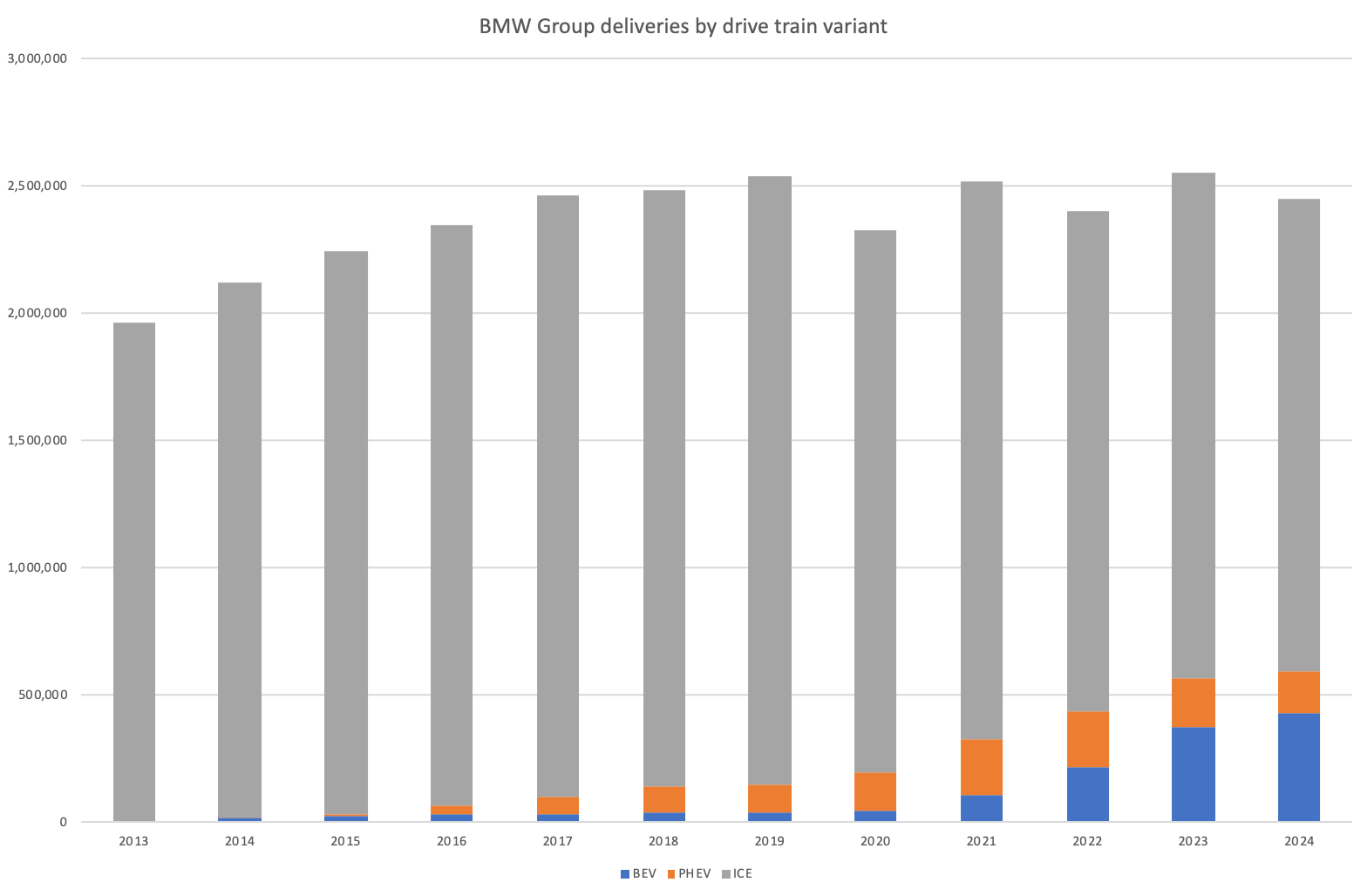

And so, despite the strong scepticism, BMW is now far ahead of all its peers in the transition to electrification:

In 2024 almost 25% of BMW’s deliveries were electrified vehicles (PHEV and BEV) and BEVs alone were 17.4%. At Q1 2025 these figures were 26.9% and 18.7% respectively. More advanced peers such as Mercedes and VW are in the 8-9% BEV range, while most legacy automakers are much lower still (3-5%). With peers now flip-flopping, revising their ICE phase-out dates and adjusting their BEV launches, BMW has just stuck to its strategy while also progressing onto the next. For the avoidance of doubt, none of this is intended to convey arguments of the sort: “BMW makes better cars than everyone else.” There are other legacy players who make great cars too. For example, I’m expecting the upcoming Mercedes CLA electric to be excellent, but that’s not to say Mercedes has made consistently good businesses decisions. For example, by making entirely separate BEV versions of the S and E class with different looks and architecture, they lost authenticity, consistency and flexibility too - and I suspect this is why Mercedes’ updated strategy has been starting to look at bit more like BMW’s (from hard electric-only approach » flexible and consistent).

Amazingly, BMW outlined their current strategy as long ago as 2017 (you can see it all here) - basically as I described above and setting a 2025 target of 15-25% electrified sales. They have executed to the letter (credibility + long-termism). I sometimes muse that finding credible company management is a little bit like being able to see into the future.

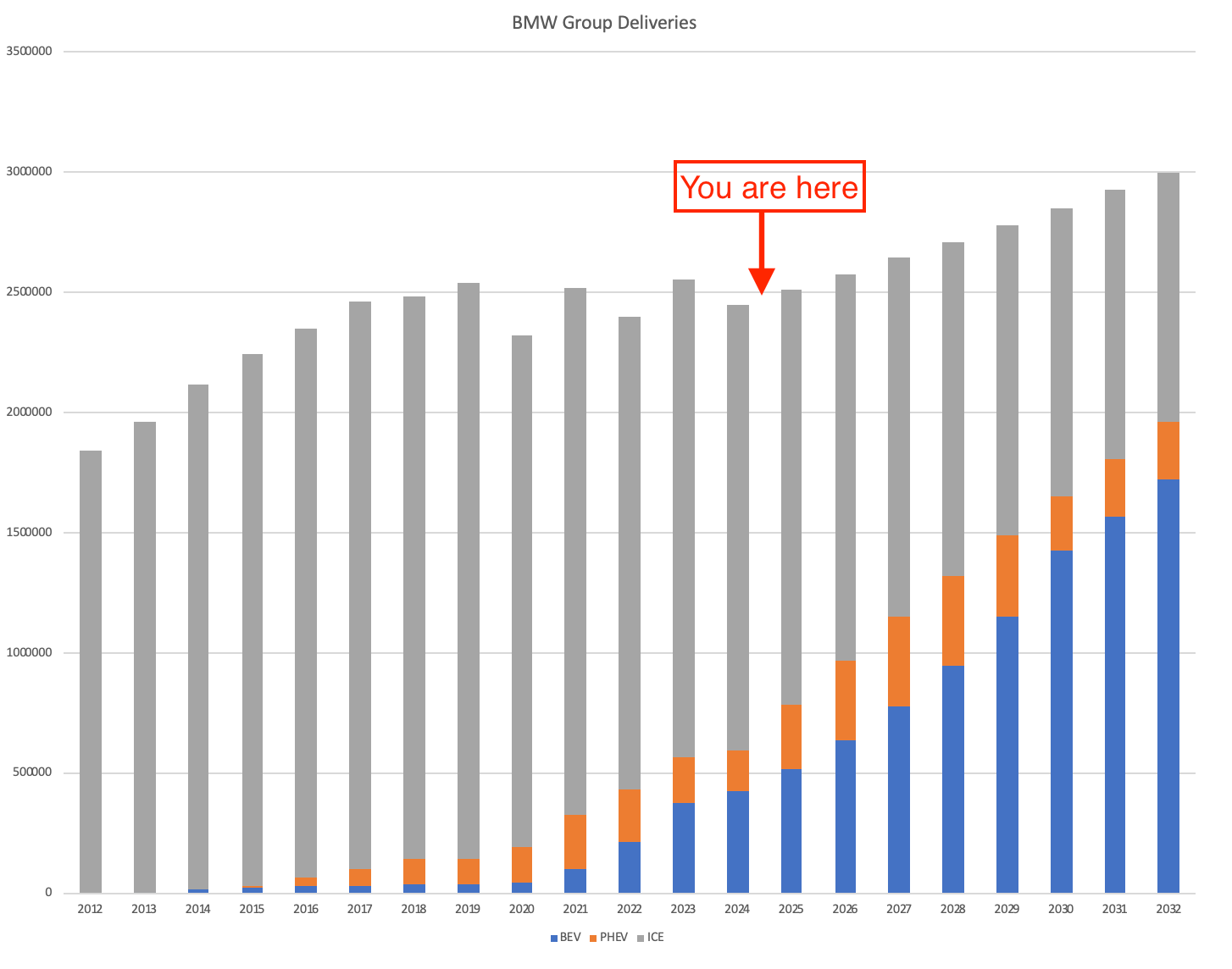

So BMW is faring well against its legacy peers, but what about the new guys - the Teslas, BYDs and Xiaomis of the world? My feeling here is that BMW will be the first legacy manufacturer to fully convince investors of its ability to flourish in the new automotive world - loosely analogous to the first packaged software players demonstrating their right to exist in the emerging SaaS world over a decade ago. In both cases there is a ‘valley of death’ to be crossed before the newer/growing part of the business manages to overwhelm the effects of the older/declining part:

I’ll get into the details later,3 but this illustrative chart is based on actual goals and targets that BMW has already given us. After years of going nowhere, ‘forecasts’ of this sort are typically met with scepticism. But in practice all it means is that BMW sells as many BEVs in 2032 as Tesla does today, while the total unit count increases by a mere 2.6% annually out to 2032. And with a return to unit growth, we get a shot at that 10-12x P/E I mentioned. Am I being unrealistic? Let me know what you think.

My view is that BMW will compete with Chinese brands primarily in the same way it competes with Toyota - i.e. they will only overlap insofar as Chinese automotive groups are able to successfully launch their own global premium brands, as Toyota did with Lexus. And building, nurturing and sustaining a global premium automotive brand is incredibly difficult. Toyota is the largest car business in the world and far better managed than practically all others (BMW being one exception). In 36 years, Lexus has not managed to reach even 40% of BMW’s unit volume, and even then it’s heavily concentrated in the US. As we shall see shortly, BMW itself has only really been at it 40% longer than Lexus. Tesla, of course, managed to ramp to 80% of BMW’s volume in a much shorter period (~12 years), but I would make several key observations here: 1) it was during a unique window when Tesla was, in effect, the only one with a practical ‘everyday’ BEV on the market, and it happened to be in the premium segment - this window is now closed; 2) Tesla’s CEO has said repeatedly that he wants to sell vastly more cars in future (20m by 2030 was the explicit goal until recently) - if he achieves this there are unanswered questions about the longevity of the brand’s premium status (scarcity); 3) Tesla’s rapid collapse in Europe this year, reinforces the notion that the company is not sufficiently capable in the art of brand management as is required to sustain a premium brand. It’s not a hill I’m prepared to die on, but I suspect Tesla will gradually exit the premium category over time, whether intentionally or unintentionally.

Time to dive deeper.

Dramatis Personae

As I will refer to various persons involved in the BMW Group over the years, I thought it might be easier to list them in one place that can be referred to (current cast members in bold). Note that in Germany, public companies typically have a ‘board of management’ or vorstand, the equivalent of which is ‘executive committee’ in the Anglo-American world. The chairman of the board of management therefore is equivalent to CEO, so whenever I refer to the ‘chairman’ that is how you should interpret it rather than the chairman of the board of directors. German businesses similarly have a ‘supervisory board’ - equivalent to the ‘board of directors’ in the Anglo-American world. Lastly, note that German supervisory boards also have mandatory employee representatives among their members.

Chris Bangle - Director of Design BMW cars 1992-2004, Director of Design BMW Group 2004-2009

Domagoj Dukec - Head of Design BMW cars 2019-present

Wilhelm Hofmeister - Head of Body Engineering 1952-1976

Adrian Van Hooydonk - Head of Design BMW cars 2004-2009, Director of Design BMW Group 2009-present

Eberhard von Kuenheim - Chairman of the board of management 1970-1993, chairman of the supervisory board 1993-1999

Claus Luthe - Director of Styling 1976-1990

Walter Mertl - CFO 2023-present

Joachim Milberg - Chairman of the board of management 1999-2002, Chairman of the supervisory board 2004-2015

Milan Nedeljković - head of production 2019-present

Helmut Panke - Chairman of the board of management 2002-2006

Nicolas Peter - CFO 2017-2023, Chairman of supervisory board 2025-present

Bernd Pischetsrieder - Chairman of the board of management 1993-1999

Joachim Post - head of development 2025-present

Norbert Reithofer - Chairman of the board of management 2006-2015, Chairman of the supervisory board 2015-2025

Wolfgang Reitzle - Head of product development 1987-1999

Frank Weber - Head of development 2020-2025

Oliver Zipse - Chairman of the board of management 2019-present

The Making of Modern BMW - A Tail of Two Crises

Bayerische Motoren Werke (Bavarian Motor Works) officially dates its own birthday to 1916, although parts of the business stretch further back. Save for some brief scene-setting however, our story shall begin shortly in 1959.

The famous BMW roundel was created in 1917 and has remained largely the same:

Contrary to popular belief the blue and white design does not represent an aircraft propeller, but instead takes its cues from the Bavarian flag and the crest of the former Bavarian royal dynasty. Now, I’m delighted to confirm that NFTBC has over a dozen Germany-based readers (wie geht’s! 👋). I’m hoping some of you are Bavarian and can set me straight if I’m about to embarrass myself. Bavaria is something of an unusual state in the context of the wider German federal republic - typically darker hair, Catholic, its own politics, a distinct dialect, lederhosen etc. BMW itself is based in Munich, which is sometimes referred to as the most northerly city of Italy, being only 75 miles from the Italian border and sharing the same Alpine region. It is reasonable to say that Bavarians take pride in being different - BMW is much the same.

We don’t need to go into the deep history of BMW here. But if you wish to there are great books that cover the history, and you’ll find some referenced at the end. Just know that from early on there were aircraft engines, motorbikes, cars and then war. Instead we’ll take a look at two crises that have had lasting effects on the business and help us to understand BMW as it is today. It’s actually difficult to overstate the importance of the first - so profound was the impact that it changed the very nature of the company’s DNA and remains part of company lore today, present in the hearts and minds of employees 65 years later.

1959: Quandtum Leap

Prior to the war, BMW had been a successful automotive business, with iconic models such as the 328 roadster. Following the war, BMW was only permitted to produce motorcycles initially, returning to cars in 1951 with the “boat-like” 501 - heavy, underpowered and expensive, it was never a commercial success. While 1955’s 507 would go on to become an influential all-time classic, it wasn’t a money spinner either. Attempts to get the company onto sound financial footing included the Isetta microcar, produced under license, and then the more stylish compact 700 - these did not immediately manage to steady the ship either, and it was clear the company lacked strategic direction. By 1959 the situation was dire and the company came close to losing its independence through a proposed sale to rival Daimler. The path to redemption began when shareholder and industrialist Herbert Quandt presented a reorganisation plan which involved recapitalisation as well as significant personnel and organisational changes. With support from small shareholders and dealers, the plan was put into action. Internally, BMW had already begun engineering on a more affordable premium mid-size car - development was accelerated, taking place in two years rather than the usual four. Quandt had a gift for hiring and brought in a new chief engineer with the ability to execute on the project. And so in 1961 they launched the 1500:

With the 1500, BMW had found its niche. A sporty mid-size sedan with modern engineering, aggressive styling and agile handling. The modern BMW, both car and business, was born. BMW’s new sales director (hired by Quandt) would go onto to market 1500-derived models as Neue Klasse (New Class) - it was incredibly successful. The original four cyclinder engine would ultimately supply 3.5 million vehicles over a 26 year run and Neue Klasse’s basic design language would last into the 1980s.

From here the strategy took shape:

Periodic updates to keep the product fresh between generations, including engine variants

Expansion into new niches: coupé variants, more affordable shorter versions, convertibles, limited high performance versions

Strict adherence to, and marketing of, the redefined brand identity in each model: Freude am Fahren, Sheer Driving Pleasure, The Ultimate Driving Machine - all variations on the same theme “Joy/Freude” from the 1960s to today.

During the 1970s the Neue Klasse sedan evolved into the 5 Series, the coupé variant evolved into the 6 series and the smaller ‘02’ version evolved into the 3 Series - an innovative naming convention that remains today very much part of the brand itself (consistency).

In BMW lore Neue Klasse is credited with preserving the company’s independence and defining the strategy that would go on to turn BMW into a global success. Modern BMW had now arrived. If there are two words that really define this era and what they instilled into the business, they are: authenticity and consistency. Producing cars that look, drive and feel a certain way - the BMW way. And doing so with the utmost consistency, without deviation. The significance of the decision to re-deploy the Neue Klasse label in 2025 can hardly be overstated - the original Neue Klasse has big shoes to fill so it’s not a decision BMW has taken without careful intent about their ambitions.

The English Patient

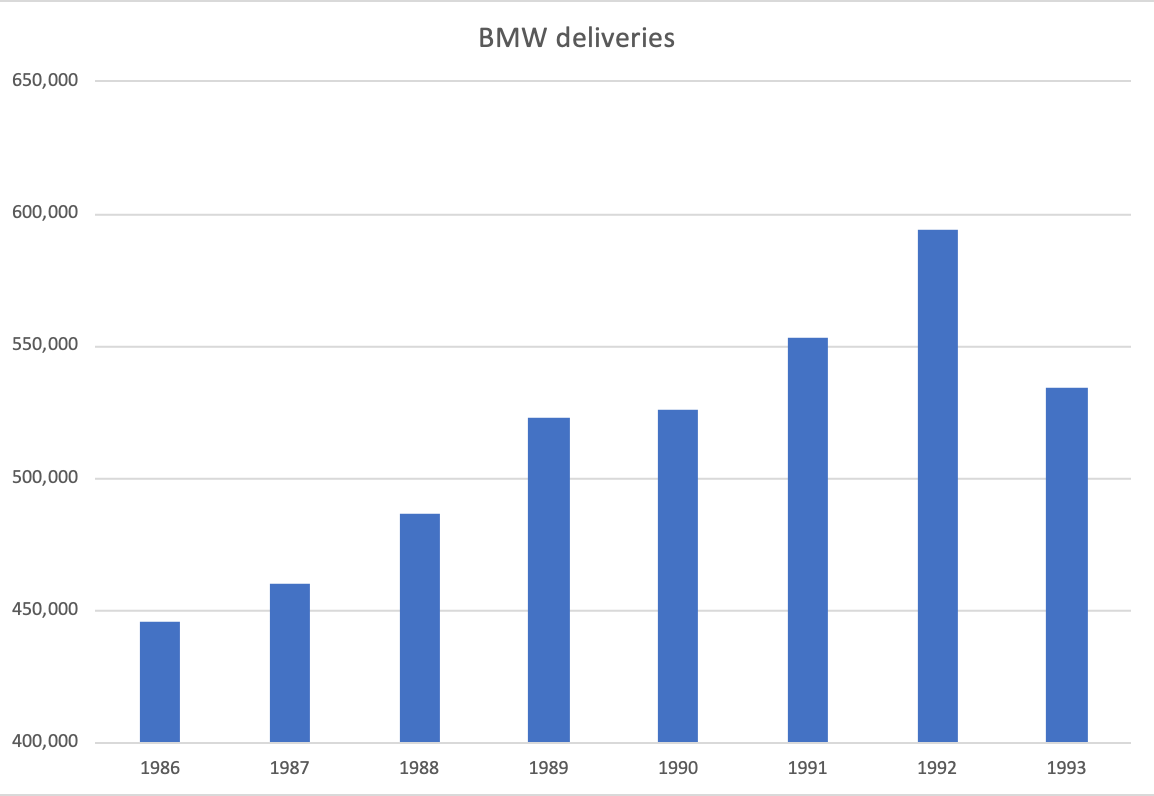

With the original Neue Klasse and its various derivatives and successors BMW enjoyed rapid growth well into the 1980s, all under the stewardship of Eberhard von Kuenheim, Herbert Quandt’s handpicked chairman. But by the time 1993 came round, BMW found itself in the unusual situation where deliveries had gone nowhere in five years. At various stages that year the shares were trading 25% lower than in 1989 too.

It’s easy to get lost in the commotion and chaos of one’s own time - and 2025 has no shortage on that front. But there was a lot going on back then! Germany had recently reunified, much of the western world was in recession and currencies were in flux (BMW made a profit during the recession, by the way). There was a lot going on at BMW too: von Kuenheim had finally passed the torch to Bernd Pischetrieder having chaired the company since 1970 and BMW was in the midst of opening its first major overseas plant, in South Carolina. To give additional colour to the scene, BMW as a group was having a sort of identity crisis or moment of self-doubt, perhaps. BMW’s design language had remained remarkably similar to the original Neue Klasse’s all the way through to the early 1990s - and it was starting to look stale. I’ll get into this in Part II, but BMW was already well advanced in reinventing itself in this regard, even if the results were not yet manifest.

Starting in the late 1980s the big three Japanese automotive groups moved aggressively into the premium segment with new brands (Lexus, Acura, Infiniti) - especially in the US, where BMW was not yet as well established as it is today. With lower prices, compelling features and arguably higher build quality at the time, there were genuine fears as to how BMW, Mercedes and Audi would be able to compete [note: has anyone spotted the parallel to today yet?]. In its first full year (1990) Lexus outsold the entire BMW range in the US, and two years later overtook Mercedes too! Lastly, there was a widely circulated McKinsey report in the early 1990s recommending that automakers needed to make at least 1.5m vehicle sales per year in order to have sufficiently competitive unit economics - anyone below this threshold was deemed at risk of losing its independence. BMW was well below the threshold.

With that backdrop, BMW’s leadership concluded that the company needed to expand through acquisition in order to achieve better scale, rather than risk diluting the BMW brand itself - all in order to protect the company’s independence. An early target was Porsche, which BMW came pretty close to buying - the ~$600m price tag proving too steep for von Kunheim.4 Instead, now under Pischetrieder, BMW acquired Rover Group in early 1994 for £1.7bn. The acquisition brought with it the Rover, Land/Range Rover and Mini brands. While BMW was particularly keen to get hold of the heritage brands Range Rover and Mini, the deal could not be closed without Rover, and Pischetrieder believed they could make a success of that one too. The acquisition was disastrous. The Rover brand itself proved to be beyond repair, despite the best efforts of BMW’s engineers. For the next six years it became such a drain on the Group’s resources that it was known internally as “The English Patient”. In 1999, Rover Group even forced BMW to report a massive asset impairment. Ultimately, the acquisition led to major change at the top in 1999 - Pischetrieder was out as chairman, von Kunheim was out as supervisory board chair and within the space of 14 months most of the management board had been turned over, including BMW star Wolfgang Reitzle.

I won’t say this was not a very difficult time for the company. But I also think that this time crystallizes why this company is as strong as it is. After 1999 and 2000 and all these changes of personnel, we not only replaced everyone on the management board from inside the company, but we restored earnings despite economic recession in Europe, the US and Japan and achieved our strongest sales in history

Helmut Panke

BMW had to pay around EUR 3.2bn to get rid of Rover in 2000, not to mention around £3bn in losses over six years. On the other hand they did recoup around EUR 2.9bn in selling Land Rover to Ford - a very divisive decision at board level, contributing to the board turnover. BMW was left with just the Mini brand (or ‘MINI’ as it was soon rebranded). In the end BMW completely re-invented and re-engineered MINI, and by using the brand’s uniquely authentic heritage in a very BMW-like way they have taken it from nothing to around 250,000 annual deliveries today - it’s been a great success, yet a poor ROI unless you include the synergies of being able to share architecture with BMW’s own smaller models. Similarly the success of the Range Rover brand today, is largely a reflection of BMW’s engineering efforts more than 20 years ago.

Before his ouster, Pischetrieder did however make one deal that would more than make up for his other error. In an extraordinary move, he effectively managed to force VW into selling BMW the rights to the Rolls-Royce Motor Cars brand for £40m. Much like MINI and Rover, Rolls-Royce was an exceptional heritage brand, but one that had suffered from years of neglect. BMW completely reinvented the company - locating and building a new plant in Goodwood and designing and engineering an entirely new yet sublimely authentic car. The success of this brand today can hardly be overstated - and it’s potentially worth in the region of EUR 30bn. [see my Rolls-Royce post here].

So here are the principal lessons I believe BMW took away from the 1993-2000 period (and why I have taken the time to write this part):

Don’t underestimate the strength and potential of the BMW brand. Any fears that drove BMW to acquire Rover were ultimately unfounded. Starting in the 90s they pushed the brand into new segments, markets and niches with tremendous success (X models, roadsters, 1/2 series etc).

Stick to truly iconic and authentic brands that serve premium or aspirational niches - brands that have a story to tell. This includes BMW, Range Rover, MINI, Rolls-Royce and Porsche, but not Rover and most others - the bar is very very high.

Don’t risk what you already have for what you don’t need. BMW had built an independent and financially strong business with a great culture and exceptional brand - the cultural and financial drain of the Rover Group put all of this at risk.

And here are some additional lessons that we can take away:

BMW is extraordinarily good at managing iconic car brands, even if they’ve been neglected for decades. They completely re-engineered, re-designed and re-launched MINI, Range Rover and Rolls-Royce and made each the best it has ever been. I can’t think of anyone else who’s done the same once, let alone three times. (Note: VW hasn’t done a bad job with Bentley but nothing like as well as Rolls-Royce - see for example the relative resale values)

The depth of management talent at BMW is really impressive. BMW could turnover its top executive ranks in short order through internal promotion, without any loss of continuity or business momentum. And, indeed, the departing execs all went on to top roles elsewhere. Notably, after BMW Pischetrieder spent 6 years in a executive role at VW and 10 years on the supervisory board of Daimler/Mercedes - it’s difficult to imagine the reverse.

The value of committed family owners

Source: BMW Group reports

The Quandts

Herbert Quandt passed away in 1982, following which his widow Johanna became the family’s representative on the supervisory board. In 1997 Johanna retired, and her children Stephan Quandt and Susanne Klatten joined the supervisory board, where they remain today. Per the 2024 annual report, Stephan owns 26.6% of the ordinary shares and Susanne owns 21.5% - around 48% of the total and 44% of the economics once you factor in the non-voting shares. Aged 59 and 63 respectively, I’m expecting them to remain closely involved with the company for a long time to come.

At one stage I was toying with the idea of sub-titling this post “BMW - The Anti-Tesla”, as a tongue-in-cheek attention grabber. Tesla and BMW’s principal shareholders could hardly be more different. Stephan and Susanne are intensely private and publicity shy, and they expect BMW’s senior managers to act with a similar level of decorum:

Von Kuenheim is known to describe the proper way a true BMW manager conducts himself with a French term, comment. The literal translation is simply “how,” but in his own idiomatic use of the word, according to one BMW executive, it means, “you just know.” What this means at BMW is that BMW managers, especially the chairmen, are expected to always act discreetly. Never air the company’s laundry in public. Never discuss private meetings, especially with the Quandts. Be poker-faced and speak in professional terms - and then only when you have something worthwhile to say. Don’t ever put the company’s business in the street. This is something that doesn’t have to be written down or ever spoken to BMW managers. The ones who will rise high within the organization “just know it”. This was the style and pattern of Herbert Quandt, and it is still a part of the company culture more than 20 years after his death, because the merits of discretion and privacy are so ingrained in this children.

From Driven by David Kiley (2004)

Fresh to the supervisory board, in the end it was Stephan and Susanne who precipitated the management overhaul I mentioned before, as well as bringing a decisive end to the Rover debacle, which in addition to all the other issues, was becoming an increasingly public affair in both Germany and the UK.

In fact, there’s so little public information about the Quandts, I couldn’t make this section long even if I wanted to. But here’s something they said in an extremely rare interview five year ago with Manager Magazin (Google Translate):

Klatten: As supervisory board members, we act as sparring partners; we advise to prepare well for decisions. As supervisory board members and as shareholders, it is important to us that business is well managed in the interests of the company and its employees. Therefore, we pay particular attention to critical issues such as personnel or strategic questions. But the executive board alone manages the business.

Quandt: None of us tries to interfere in the company bypassing the executive board. Sure, I also visit plants or, as a member of the supervisory board, get briefed on special topics. But I don't call the third level to embarrass the executive board with detailed knowledge. That's part of respectful interaction. I live by the principle of a long leash, and I have the impression that my sister sees it similarly.

Is the leash particularly long for the board of directors at BMW, by far your most significant holding?

Quandt: I think so, because the BMW board doesn't have to deal with takeover scenarios or boost the stock price in the short term, as is sometimes the case elsewhere. And because each of us stood by BMW during the dramatic corporate crisis following the failed Rover takeover, and the board can still rely on that today, it has – indirectly – greater freedom.

Klatten: The company is professionally managed; we as shareholders enable calm and a long-term perspective. Independent of BMW, my personal goal is to constantly review whether I'm still the best owner. One who doesn't just bring in silly money, but creates added value, working together with management. The important thing is that neither side should be overburdened. And it has to align with the company's values, such as sustainability. That's sometimes a balancing act.

Employees, strategy, long-termism, sustainability - not much about ‘shareholder value’. In fact in the same interview, Quandt goes on to say he’s more driven by his responsibility for securing jobs in Germany than he is about money. Perhaps somewhat alien to acolytes of the Friedman school of economics - NFTBC readers will already know that there are other examples of businesses that are financially successful only as a secondary outcome of some higher purpose. The economist John Kay calls this Obliquity. Just think about it - what is the best way for BMW to secure jobs in Germany in the long-term? The answer: to be a damn good car business with efficient manufacturing, desirable products and high margins. A means to an end. The contrast with VW, which is having to layoff thousands of employees in Germany, could not be more stark. While BMW’s two large peers also have employee-profit share schemes these days, BMW was something of a pioneer:

BMW derives much of its strength from an almost unparalleled labor harmony rooted in that long-ago pact. In 1972 and years before the rest of European companies began to think about pay for performance, the company included all employees in profit sharing. It set up a plan that distributes as much as one and a half months’ extra pay at the end of the year, provided BMW meets financial targets. In return, employees are flexible. When a plant is introducing new technology or needs a volume boost, it’s not uncommon for associates from other BMW factories to move into temporary housing far from home for months and put in long hours on the line. Union leaders have made it easy for BMW to quickly adjust output to meet demand. Without paying overtime, the company can increase the production schedule to as much as 140 hours a week (20 hours per day, 7 days a week) or scale it back to as little as 60 hours. The system enables BMW to provide a high level of job security.

From Organization Behaviour, by Don Hellreigel and John Slocum (13th ed, 2010)

For a rare opportunity to see Stephan Quandt speak at some length, check out BMW’s recent AGM where he pays tribute to Norbert Reithofer following his retirement as supervisory board chairman for 10 years, and before that management board chairman (starting 2hr 7min). He touches many of the issues you will now already be familiar with - most notably the importance of flexibility (“an integral part of BMW’s DNA”), financial strength and strategy.

Part I - Conclusion

Now, believe it or not but a decade or so ago I was particularly bullish on Tesla’s prospects for selling an awful lot more cars than they were at that stage (~30,000 in 2014). Back then, there was an intense degree of scepticism that BEVs would ever take off in any meaningful way. But it seemed pretty clear to me that Tesla had created a highly disruptive product - all they had to do was navigate the litany of automotive industry challenges and complexities that I outlined earlier. Within four or five years (and thanks to the unique capital markets talents of the CEO) it suddenly became obvious that Tesla was going to be a very large business. And then, of course, with hindsight the whole thing became obvious all along. Recall this also coincides with the period when BMW was perceived to be a laggard in the race to electric.

And I was asking him, “you’ve had success with the Model S, but the German manufacturers are going to do this, and they’ve got all this manufacturing expertise and et cetera.” And so I asked him these sorts of questions for five minutes or something, and he stopped me and said, “listen, you just don’t get it. Our ability to succeed will be dependent on our own execution. They are institutionally incapable of competing with us.”

Baillie Gifford’s Tom Slater, speaking to Elon Musk in 2013. As retold in Steven Clapham’s podcast.

Institutionally incapable. Tom Slater is a really insightful investor, and so what he saw early came to be ‘common knowledge’ years later. Is it necessarily true though? To me, the evidence says otherwise or indicates only a half-truth perhaps (recall the category error I highlighted earlier). In the intervening years Tesla’s time-to-market has been lengthening and its execution getting somewhat patchy. For its part, BMW’s development cycles have shortened significantly (by almost 50%!) and execution has been solid and consistent.

In Part I we have introduced the principal characteristics that set BMW apart from its peers as well as some of the history explaining how this came to be - the unusual structures that enable it to compete as an institution. In some respects, a very conservative institution, but in others a highly dynamic one. There are few sacred cows at BMW, other than the very essence of what a BMW is supposed to be - and this is how the company is able to keep pushing forward and adapting, all while remaining consistent with the past. Perhaps Norbert Reithofer summarises it best in the introduction to BMW’s 100 year anniversary book, A Century of BMW:

The future belongs to those who dare. Throughout its fascinating history, Bayeriche Motoren Werke has proven this to be true time and again. Over the past 100 plus years, the company has repeatedly managed to reinvent itself and shape the future - all by going its own way.

In Part II we will start by looking how it competes, including design, engineering and a closer look at Neue Klasse 2.0. In the meantime feel free to leave a comment or get in touch if you have any questions.5 Also, check out my Rolls-Royce Motor Cars post if you haven’t yet.

Further Reading

A Century of BMW, Manfred Grunert & Flortian Triebel (BMW commissioned)

BMW Group - The Next 100 (BMW commissioned)

BMW by Design: The Untold Story of BMW Styling, Past, Present and Future, Steve Saxty

The BMW Century, Tony Lewin

Driven: Inside BMW, the Most Admired Car Company in the World, David Kiley

I’ll add the caveat that at least some interest in cars is required. With no interest at all, Mrs Crashkolnikova would struggle at this task for example.

When originally published I quoted a FCF yield of 15%, but this did not factor in the minority interest in BBA (BMW China). The revised figure is my best guess, based on figures that BMW have given us.

Until 2-3 years ago BMW had a stated ambition (as opposed to target) of 3m vehicles annually in 2030 - they have de-emphasised this somewhat now but without explicitly rescinding it, while remaining committed to growth. I’ve pushed the 3m ambition to 2032 here. BMW also has a ‘target’ for 50% BEV mix by 2030, which they remain committed to. These are the principal assumptions I have used here, the rest is basically extrapolation.

What a sensational acquisition that would have been. And a bargain!

If your question is about the size of BMW grilles, please wait for Part II!

Very insightful piece and I’m eager to read part 2.

Really intereting!!