BMW - Update (October 2025)

Reflections on the Q3 sales numbers and 2025 guidance

Friends of NFTBC.

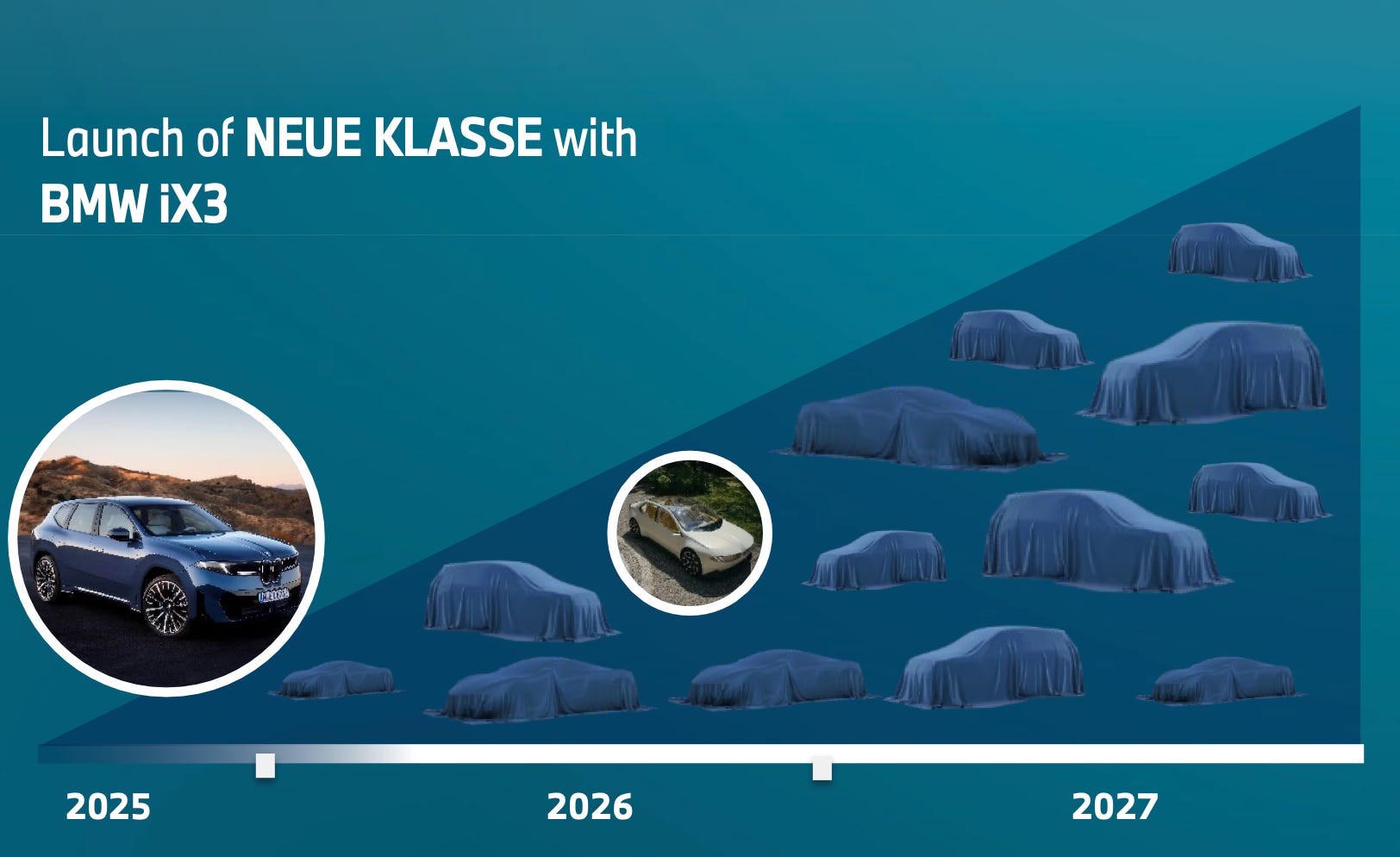

It’s a historically interesting time to be looking at BMW, which is why I started writing about it in July. On the one hand, the winds of change in the automotive industry are blowing about as hard as they ever have. On the other, BMW has just undergone its greatest internal reinvention since the 1960s and is about to rollout 40 re-imagined models in 26 months - with best-in-class technologies, lower BEV price points and lower cost structure. If you’re curious to learn more, Part I of my deep dive remains free to read.

I, for one, am very curious to see how it will all unfold. My thesis is that investors will be positively surprised in the end, and that BMW could be the first of the legacy automotive players to demonstrate a renewed right to exist. If I’m right, for the first time in a decade or so, BMW will once again be viewed as a growing business - in sharp contrast to the implied terminal value today.

But the voyage might not be plain sailing from A to B. While the product ramp will be genuinely unprecedented in its speed, it is not quite yet underway. So until the hard data starts to come in next year, the bull case will remain conceptual and subject to doubts. Yesterday’s update had both positives and negatives, and I would fully expect the latter to outweigh the former at this stage.

This is a brief post for those NFTBC readers following the story. I anticipate there will be more to say in early November when full results are published.

[NFTBC does not give investment advice. I currently own BMW preference shares and might buy more]