Merck KGaA - A Deep Dive

And observations on multi-century compounding

Friends of NFTBC

I’ll start by saying this post is not about the large US pharmaceutical business “Merck & Co”, rather, it is about the German business “Merck KGaA”. Many moons ago the former was actually a subsidiary of the latter - I’ll touch on some of that and the resulting regional nomenclature later. For simplicity, I shall refer simply to “Merck” from hereon.

Next, a couple of items of housekeeping. First, for any newcomers please check out the NFTBC User Guide for a sense of what this blog is about. In summary I write about large and mid-cap global equities that are doing something different, worthwhile and are potentially worth owning - but don’t seem to attract much attention in the usual online forums.

Second, NFTBC now has a referral program! If you want to read NFTBC for free for one month, all you have to do is successfully refer one other reader (free or paid). More referrals = more months. Get your unique link here:

Now onto Merck…

[NFTBC does not provide advice - please do your own research. Disclosure: I currently own Merck KGaA shares]

Introduction

If you go around asking people about Merck, you’ll typically hear something vague about pharma or chemicals, or the inevitable confusion with Merck &co. Some of the compounder crowd have heard of Merck via their interest in bioprocessing, but it’s not one they usually own themselves. So what is Merck? Based in Darmstadt, Germany, for over 350 years, Merck today has major operations in three domains: life sciences, pharmaceuticals and electronics (in descending order of revenue). It’s a EUR 21bn revenue business with a market cap of ~EUR 50bn at time of writing.

My ambition with this post is to bring the curious and motivated reader up to a good level of understanding over the course of 30 minutes - if I get it right, I’m hoping to demystify this interesting business for those who might otherwise be put off. I don’t intend to analyse the living daylights out of all of Merck’s business units here, but I do anticipate writing more about the company in future posts and you can sign up for those here:

From a competitive standpoint I would argue that Merck’s business is the best it has been since IPO in 1995. For sure, there are a couple of perceived hairs on some of Merck’s businesses currently - but, as I shall argue, one is emphatically a transitory issue (Semiconductor Solutions) and the other (Healthcare) is in a much better idiosyncratic position than your typical large/mid pharma and is also undergoing some quite promising self-help. Presently, the intersection of cheapness combined with sufficiently high durable growth makes things interesting. But I should note that I don’t expect any near-term miracles - the pharma part of the story could well take in excess of 12 months to play out in a way that sufficiently quells investors’ doubts. For time horizons longer than 12 months I think Merck is looking intriguing at these levels - I now own a little myself for the first time.

Let’s consider some longer-term context…

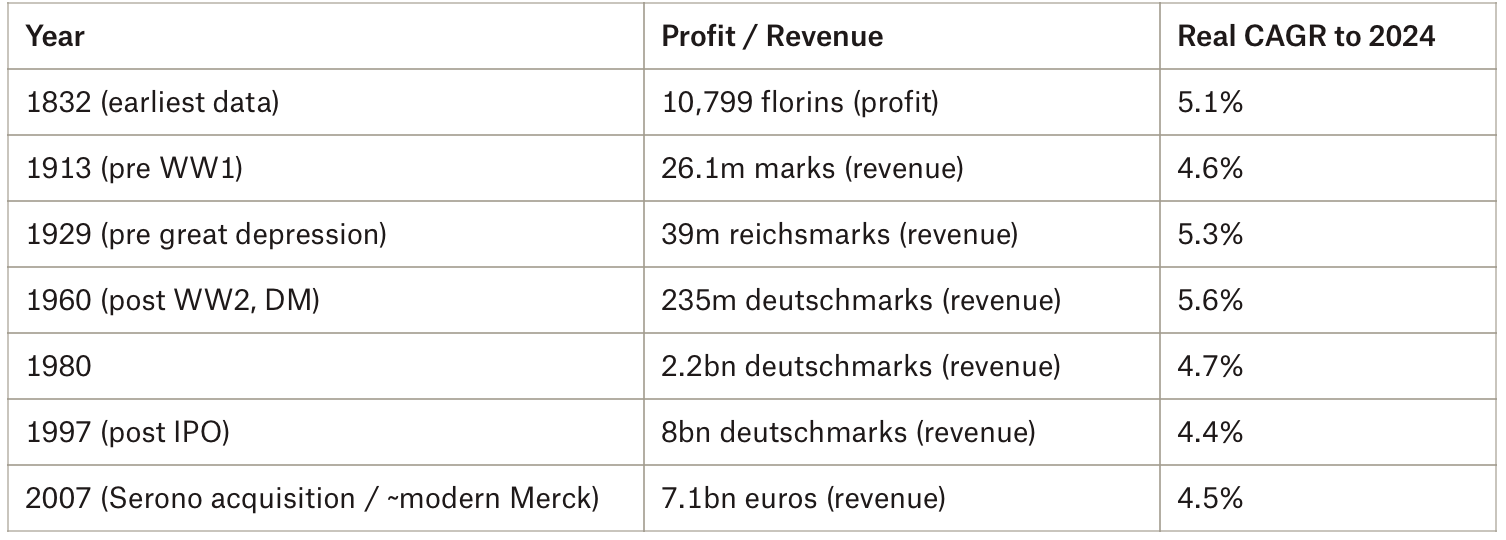

It’s extraordinary to me that a EUR 21bn business that’s more than 350 years old can still be 70% owned by the heirs of the founder. Through wars, new nation states, expropriation, 5+ monetary systems, global financial crises, hyperinflations, family feuds, technological disruptions and dozens of other crises, the family hasn’t been diluted out of their position. Yet, over exceptionally long periods Merck has outgrown inflation by 4-5% - do that for long enough and you grow quite large.

[For the avoidance of doubt, this exercise👆 is intended as a bit of fun and I encourage readers to take it in that spirit. While some unknown number of TPUs/GPUs were melted in its making, it is not intended as a rigorousness academic study]

There have, of course, been long stretches of stagnation here and there and stretches of high performance at other times. The moral of the story is one of adaptation - there obviously hasn’t been a singular playbook the whole time. For me, Merck brings to mind the Lindy Effect, popularised by Nassim Taleb: the longer that something has survived, the longer its remaining life expectancy. Conversely, Taleb also notes that size is the enemy of survival:

You have family-owned businesses that have been around for 500 years. You cannot name a corporation that survives intact for even a few decades.1

It seems Taleb more had in mind Japanese Shinese, small artisanal family firms rather than a large corporation like Merck. While I don’t want to pull on this thread too vigorously, I still wonder if there’s something to it - for example, the word “resilience” comes up on 24 different pages in the most recent annual report. And since 1990 (when the company started to become more active) the primary motivation for both acquisitions and divestments has been to “safeguard” the existing business rather than grow revenue. I think that’s why real growth has “only” been in that ~4 to 5% range - to grow much faster might risk long-term survival.

So the crux of what I’m trying to get at in this post is that this real growth is likely to continue well into the future and in the current context that means per share earnings to keep compounding at ~7% on average or perhaps slightly higher. I don’t think it’s unreasonable to frame Merck therefore as a compounder - just an extremely long duration one rather than a higher octane one of the popular sort.

But we investors tend to over-shoot. Merck’s Life Science and Electronics businesses were major beneficiaries during the pandemic and the company enjoyed several years of unsustainably high growth in the teens.

We investors also undershoot however, and that is what I believe is going on today.

Sum-of-the-parts is not the central thesis I intend to offer you here - it’s very unlikely Merck will go down the spin-off or sale route. The conglomerate structure is itself part of the resilience strategy. We will therefore, take Merck as it is. Nevertheless, some elements of SOTP thinking are interesting to consider if only in passing to give a sense of what’s there and what it might be worth. Take Merck’s world-class bioprocess business Millipore - revenue has compounded at >10% for the last 15 years and now sits at >EUR 3.5bn and 16-17% of Merck’s total. As a standalone listed business with, say, a 7x revenue multiple equivalent to peer Sartorius Stedium Biotech (XPAR: DIM) and to what Danaher paid for GE Healthcare Life Sciences, Millipore would probably trade at a market cap of ~EUR 25bn accounting for 50% of Merck’s total market cap. Much of the rest of Merck’s Life Science business came with Sigma-Aldrich, which they acquired for EUR 13bn a decade ago. Admittedly, they paid a steep price but the business has grown in the intervening years, is generally high margin and competitively positioned. For simplicity let’s just assume they could still get at least EUR 13bn for the non-bioprocess Life Science businesses. The closest comparators to Merck’s Electronics division are Entegris (NASDAQ: ENTG) and Qnity (NYSE: Q) - similar markets (semiconductor materials), similar size and similar profitability. ENTG trades at 23x earnings and >4x revenue and Q at 29x and ~4x respectively. On a comparable basis, Merck’s Electronics division could be worth EUR 15bn or more. So far we’re at EUR 53bn, similar to Merck’s market cap today.

But then there’s the Healthcare/pharma business with around 40% of Merck’s total revenue and an even higher share of profits. In my experience it’s pretty common for generalists to be put off by pharma - it often goes in the too hard pile. And not without good reason. And so I wonder if this is an exclusionary factor for many who might otherwise be tempted to take a look at Merck. My message here is: don’t be put off. Merck has a weird pharma business, and I mean that in a mostly good way. On the one hand Merck Healthcare has impressive technologies developed in-house, but on the other the bulk of profits come from assets that behave a lot more like well-established consumer brands than like patented medicines - there aren’t many comparators with this model. As we shall see 60-70% of Merck’s pharma portfolio is long off-patent (decades in most cases) and relies on things other than composition of matter patents, for example: brand/trust (particularly in emerging markets), quality, lifecycle innovation, massive scale and manufacturing complexity. For example, Merck sells the world’s leading fertility drugs and the world’s leading branded metformin - used by millions around the world. These products are growing and producing plenty of cash flow. The rub lies in the R&D supported side of the pharma businesses. Following a series of high profile clinical trial failures and years of heavy expenditure that will show little or no return, Merck Healthcare has been deemed a chronic destroyer of value. But Merck is not oblivious to the need to do better and the good news is that the problem is fixable - there’s now a well-considered new strategy in motion and they’ve brought in some world-class outside help by appointing Regeneron’s former head of clinical development as R&D chief and CMO. Merck has rapidly taken action by bringing in a commercial-stage rare disease franchise at relatively low cost, while there are some promising assets in the later stage pipeline. When I look at Merck Healthcare, I see cheap optionality - looking out two to three years the risk is more to the upside than the downside. Or in any case, this part of the business is worth an awful lot more than nothing.