Notes on GSK

Musings on the leadership change and future vs past

Friends of NFTBC.

Given the recently announced leadership change, GSK is a business I’ve been thinking about this week. It’s one I’ve owned on and off in the last five years. Somehow or other I managed to eke out a pretty decent return from it - perhaps a story for another time. I own some currently.

Before you question if I’ve started to lose my mind, I own much less of it than I do of REGN (see deep dive here). I don’t mind sharing with you that REGN excites me a lot more and is fundamentally the more disruptive business. But there’s more than meets the eye at GSK - hence my interest.

Much of the media coverage on GSK focusses on the fact that the shares haven’t gone anywhere under Emma’s nine years of leadership. This is, of course, true. But does it, of itself, make her leadership a failure? We’ll look at some of the context around this and try to shed a little light.

The other thing I want to consider is GSK’s new CEO-designate and what he inherits. Luke Miels officially picks up the baton at the start of 2026. Here’s the short version: it’s going to be much easier for Miels to gun for share price performance in the years ahead than it was for Walmsley:

His effective starting P/E is <8.5x (compared to ~15x)

There’s no need for a major R&D ramp ahead of sales growth - that’s already out of the way

The balance sheet is much more flexible for ongoing business development

GSK now has one of the best business development teams in pharma (AstraZeneca’s former BD team, basically)

GSK is now much better at developing drugs than it was 9 years ago

There’s actually a ton of optionality in the existing pipeline, but much of the nearer-term stuff is in areas that aren’t particularly fashionable right now - things like chronic cough, anti-infectives, HBV, vaccines etc

There’s intense scepticism currently as to whether GSK can meet its 2031 sales ambition of “more than £40bn”. But if it can, there’s a pretty clear path to ~6% EPS growth in the coming years. I’d also note they’ve done a good job of beating their own targets, consistently revising them upwards in the last five years or so. And if the shares can re-rate to a more sensible earnings multiple (let’s say 14x - no need to get greedy1) the returns could be handsome. But will the shares re-rate? I suspect investors might be more open to that possibility under Miels.

Let’s get going.

Emma’s Leadership: 2017-2025

Here’s what Emma inherited back in 2017, when she took over:

Chronic R&D underinvestment in pharma (~15.5% of sales)

Underperforming R&D organisation - on some measures of productivity the worst in the industry at the time!

Limited BD function

Debt + the Novartis consumer healthcare put option that would take debt higher

No exposure to the highest growth field in pharma (oncology)

Fortunately, it wasn’t a burning platform - she had time. Here’s the basic outline of what she did:

Significantly increased R&D investment (>19% of sales)

Undertook a root and branch cultural transformation of the R&D organisation and approach, led by Genentech veteran Hal Barron

Brought in new BD leadership

Created an enlarged consumer healthcare JV with Pfizer and spun it off (Haleon), thereby reducing debt (2022)

Launched “New GSK” focussed solely on pharma and vaccines

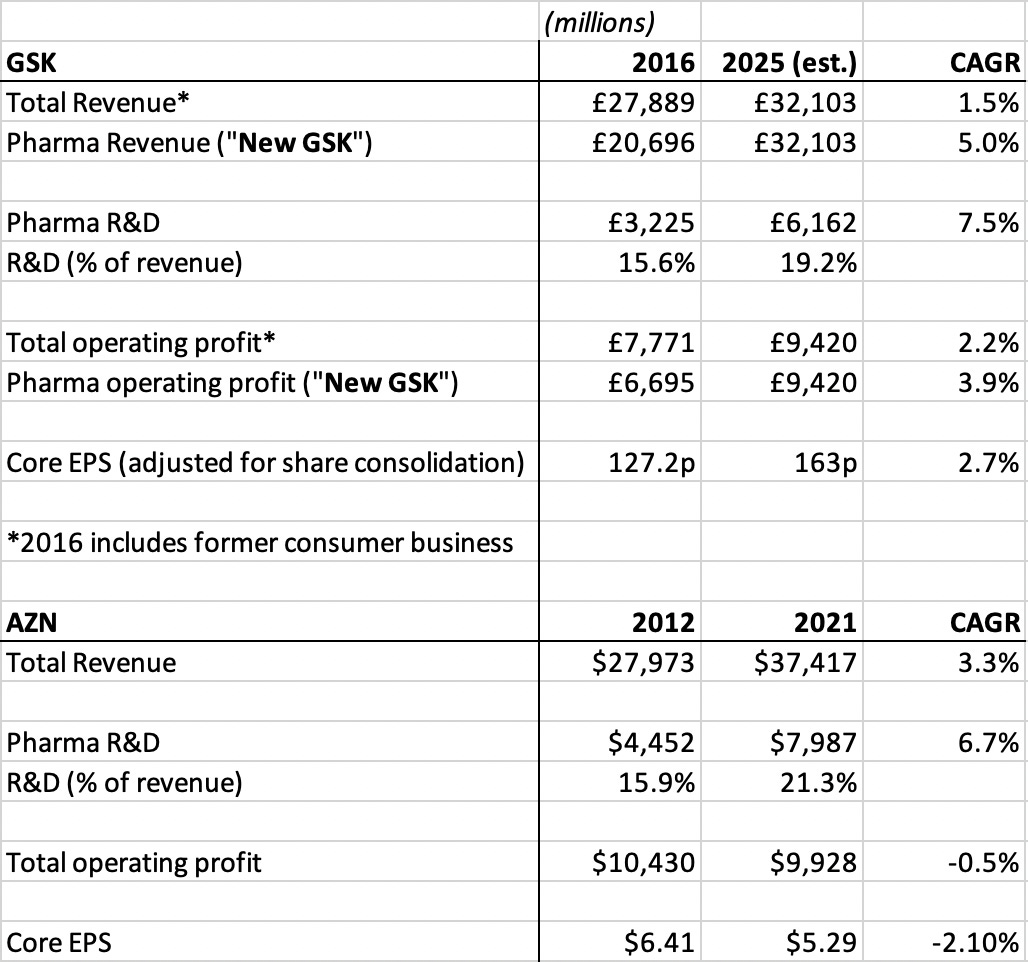

In the first four years, operating profit more or less went sideways. But after announcing New GSK in 2021, operating profit has compounded at about 10% as they said it would. There’s been a lot going on beneath the surface.

Naturally, GSK gets compared to AstraZeneca (AZN). AZN, of course, had its own R&D turnaround starting 4-5 years earlier under the leadership of Pascal Soriot. So let’s compare what happened in the following 9 years after each turnaround got underway:

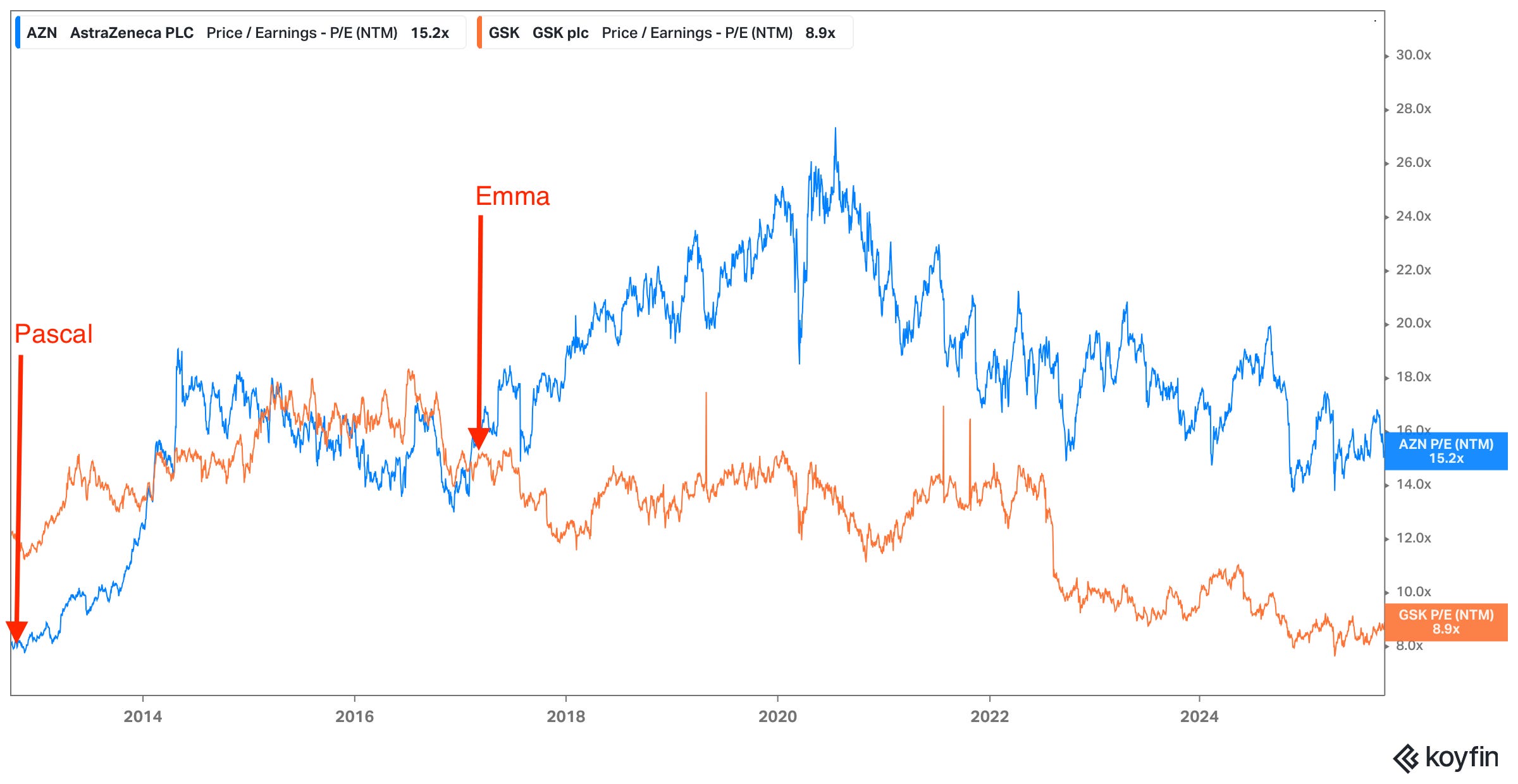

From a look at the numbers, New GSK has actually grown its profits at a respectable, if somewhat pedestrian, pace. And that’s with the significant headwind from growing R&D well ahead of revenue. They even managed to grow total EPS despite spinning off £10bn in revenue. And neither was GSK in a position to do any major transformative M&A in this time. But curiously, it’s still better than Soriot did in his first 9 years. You certainly wouldn’t know it from the two companies’ total shareholder return: +60% for GSK2 and +250% for AZN! It just goes to show how important investor perception is at the points where you start and finish:

AZN started at ~8x P/E and finished near 22x in 2021. Whereas GSK started at ~15x in 2017 and finished around 8.5x before the leadership announcement this week. Soriot has unquestionably done amazingly well at AZN and started with a steep patent cliff, but on the other hand he had more to work with on the R&D side - for example, Tagrisso, Farxiga and Imfinzi (AZN’s biggest sellers today) were already in development. Other than Shingrix, there wasn’t really anything like this on the books at GSK when Walsmely started as CEO (that we know of). Similarly, Soriot was somewhat less constrained by debt.

Given the similar market valuations, it’s tempting to compare GSK’s prospective position today to AZN’s back in 2012. And I would argue it’s in a much stronger position. In 2012 50%+ of AZN’s revenue was going off patent within a period of four years, some of it imminently (Crestor, Nexium and Seroquel). Today, investors are equally concerned about GSK’s IP position with a similar percentage of revenue at risk, hence the fears. But it seems to me that the situation is much less bleak:

There’s more of a staggered timeframe on LOEs from 2027 to 2031

The IP situation isn’t sharply defined - protection is likely to run past 2031 in some cases

Most importantly, GSK already has like-for-like replacement assets lined up in numerous cases

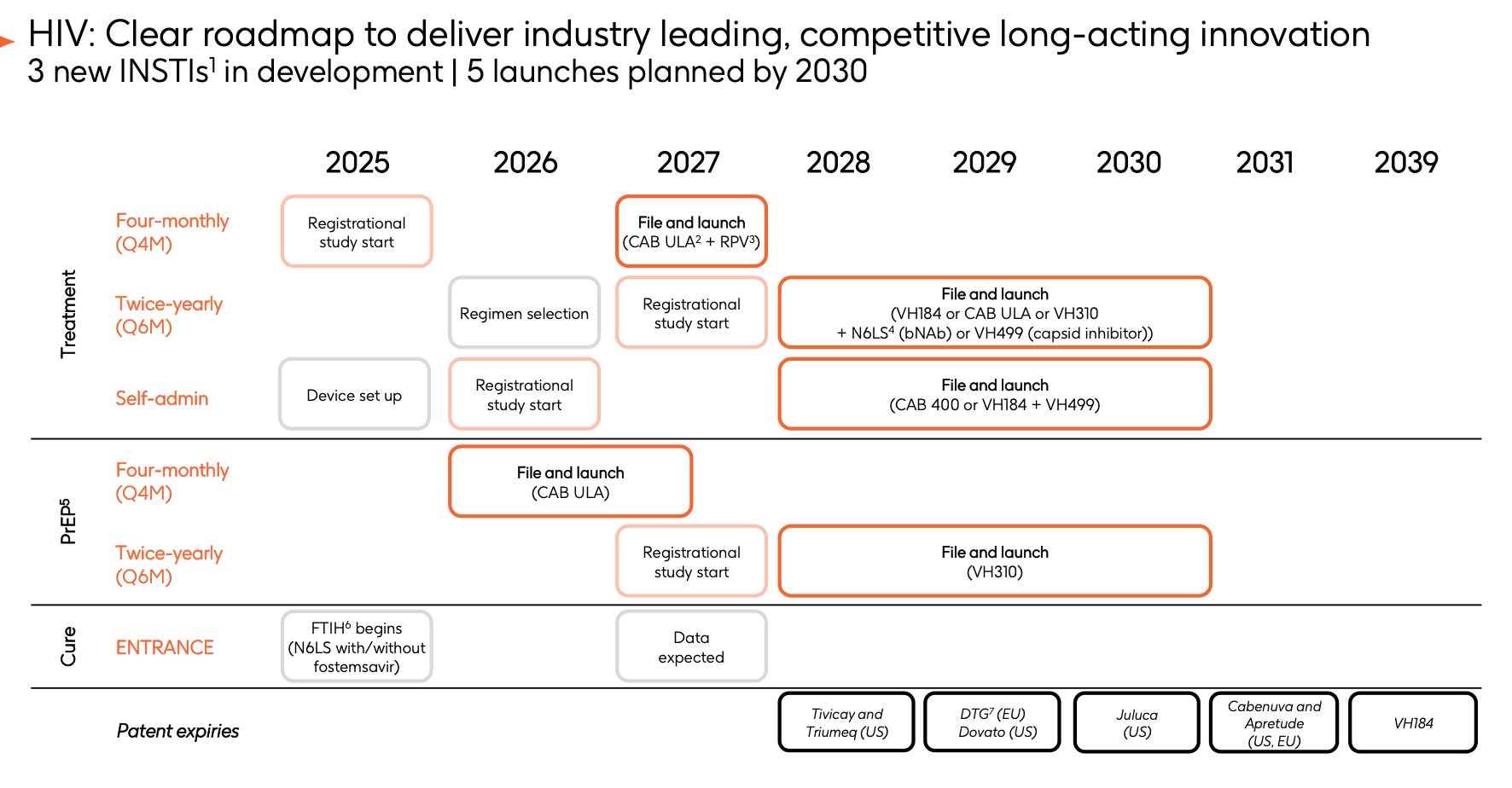

The thing that tends to worry investors most at the moment is expiry of some HIV patents between 2028-2031, accounting for almost 25% of revenue. For their part, GSK maintain they’ll be able to “significantly replace” lost revenue through launching increasingly long-acting treatments. By the end of the decade GSK will have a once every six months injection on the market and it seems likely to become the standard of care - even if the adoption curve isn’t fast enough to immediately offset the LOEs3.

One of the other larger LOEs is Nucala, an IL-5 mAb for inflammatory diseases. Its replacement is an ultra long-acting version of the same (depemokimab) and it’s already coming to market.

I won’t spend much time on pipeline here, but in my view, GSK does have some genuine nearer-term wildcards in the pipeline and we’ll just have to see how they play out (not to mention plentiful earlier-stage assets). Here are just a few:

Multiple Myeloma: expectations for Blenrep are currently low. Currently approved ex-US, the US review date is coming up this month. GSK see it as a >£3bn PYS drug.

HBV: patient population ~300m. GSK’s bepirovirsen has been first to show a practical functional cure, albeit initially at modest rates. The thing to monitor in the next couple of years is if they can materially increase cure rates through combination with in-licensed siRNAs from Arrowhead (see later). GSK see monotherapy as >£2bn PYS.

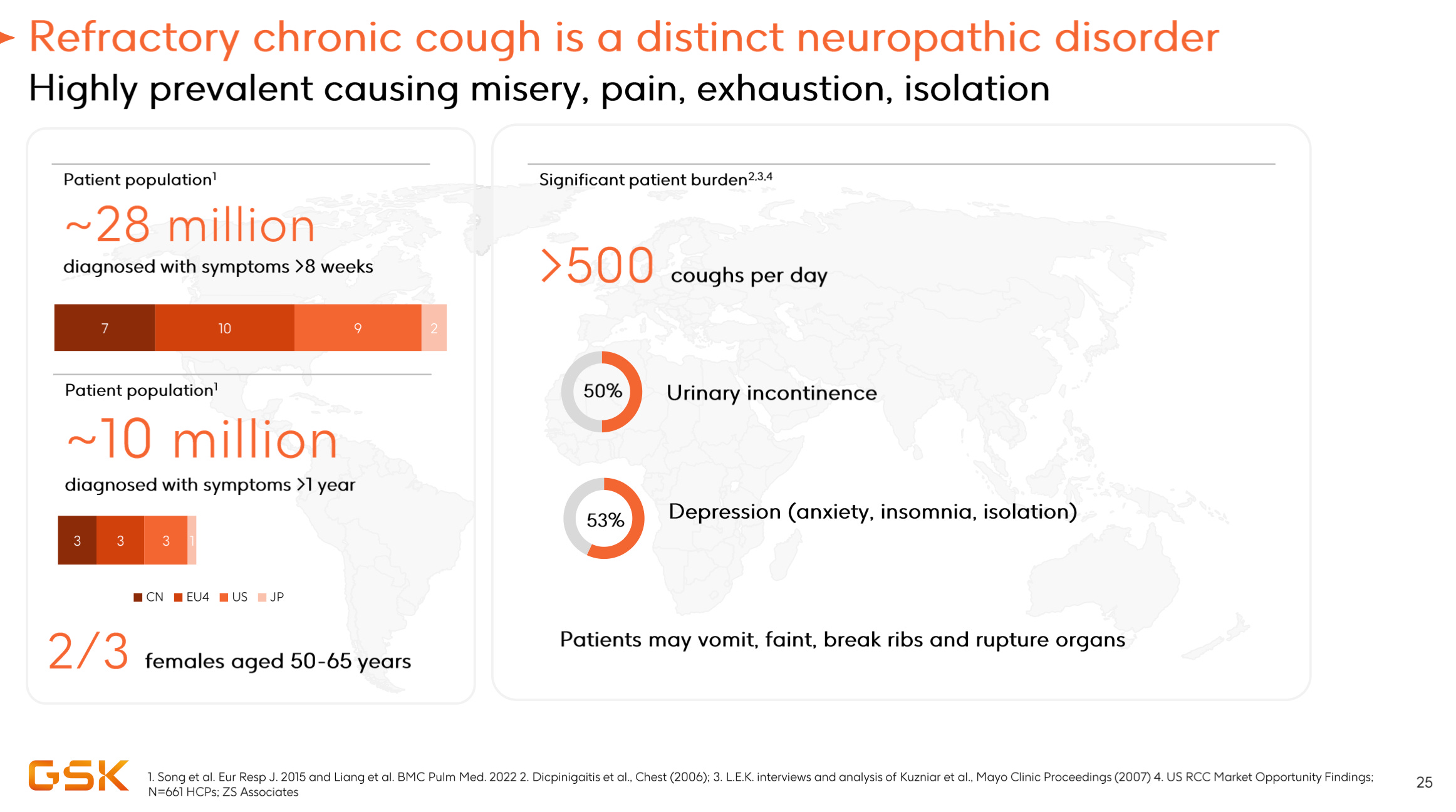

Refractory Chronic Cough: a patient population of 10m+ where there are currently no approved targeted therapies. Camlipixant has so far shown a 34% placebo-adjusted reduction in cough frequency and without the taste-related discontinuations suffered by a competitor. GSK PYS >£2.5bn.

Circling back to Emma: Could some other CEO have played the hand better? It’s an interesting question.

Pharmaceutical development takes a great deal of time and involves a fair amount of luck. For all the good that Hal Barron did with the R&D organisation (more below), his BD track record at GSK does look questionable - although perhaps it’s easier to say that with hindsight. Numerous later-stage oncology assets that might have amounted to something, turned out to be relative disappointments or outright duds: Zejula, bintrafusp alfa and belrestotug for example. Much of the BD he did was earlier stage and is still playing out - we’ll have to wait and see.

With the balance sheet in the condition it was, major acquisitions were off the cards- unless funded through issuing shares. In fact, over the last 10 years, GSK is practically alone among big pharma and major biotech in not having done any major deals in the ~$10bn dollar range (the largest was Tesaro at $5bn). My suspicion is that most pharma CEOs in Emma’s position would have attempted a large deal funded with shares - and we know how value-destructive those can be. So to have grown New GSK profits in the mid-single digits, while growing R&D ahead of revenue is not to be completely brushed aside in my view. Moreover, with Haleon she created arguably the highest performing consumer business in its category - growing sales organically 4-6% through both volume and price.

My feeling is that her talents lie in persuading, motivating and recruiting. She recruited Barron from Google subsidiary Calico, which of itself was a surprise to many - and she stuck him on the board to signal how serious she was about science and technology. She poached Soriot’s protégé Luke Miels - prompting AZN to sue GSK. She replaced large swathes of senior management in her early years, including bringing in Hal Barron’s eventual replacement Tony Wood from Pfizer. GSK had, and still has, an outside reputation for being a hopelessly stodgy old big pharma - and that’s not a great starting point from which to recruit the best. So it’s pretty interesting, to me, that she managed it anyway - there are signals that GSK’s reputation may not currently cohere so much with reality as it used to.

One of Barron’s major initiatives was to take GSK further into functional genomics in order to improve success rates (he wanted to double them). And one of the things he did, with Tony Wood, was to build out a dedicated AI and machine learning group inside GSK - starting in 2019. And it’s one of the most interesting things about GSK that I’m pretty sure most people don’t know about. Led by Kim Branson, who is certainly one of the leaders in applying AI/ML to systems biology, GSK has probably the most sophisticated and well-resourced AI/ML group in pharma. GSK, of all places, has become a desirable career destination for talented machine learning specialists with an interest in curing disease. And you don’t have to take my word for it. Here’s Chris Austin SVP of Research Technologies speaking recently about why he decided to leave his job as CEO of his own biotech (and CEO-Partner at Flagship Pioneering) to join GSK:

The reason that I decided to leave biotech and come to GSK is the ability to create fit-for-purpose data. We’ve made a huge amount of progress with public sector data and if we look at ChatGPT it’s a good example - that was all built on public sector written word so that’s why they’re so effective (very large data sets). In biology we tend not to have those and it’s become evident over the last few years that no matter how good the algorithms are they get limited unless you have large fit-for-purpose data sets that can drive the algorithms to increase productivity. The only place that can combine very sophisticated data tech computation, AI, ML, generative AI and the ability to generate enormous data sets fit-for-purpose, to drive the increased effectiveness and accuracy of those algorithms is a company like GSK. And GSK has made in my view the greatest investments into data and data analysis and data generation and it’s that opportunity that made me decide to leave running my own biotech to come to GSK because I am confident that we have the whole recipe that’s required to really drive breakthrough therapies for untreatable diseases more rapidly than has ever been possible before. That’s why GSK is such an exciting place to be now, it’s just electric

What is so exciting about GSK is, it is allowing me as an exemplar perhaps of the whole field to bring together decades of deep drug development experience with the most modern up-to-date and high throughput data generation capacities with unprecedented computation and data tech capabilities. Those things have tended to exist in different sectors - some have been good in the public sector and government or in biotech or in Pharma - but what I’m finding at GSK is all the individual things that I valued so much and bringing everything together that’s required to develop a treatment for people is all present in GSK.

Barron once said that the functional genomics and AI strategies were probably a 10-year project towards showing tangible results - such are the difficulties, complexities and timescales of pharma development. But it is already showing results in terms of speeding up development and increasing the probability of success, e.g.:

Increasing patient recruitment seven-fold.

Accelerating clinical development - they took depemokimab from phase 1 straight to phase 3 in four indications.

Dramatic speed-up in drug discovery.

Reducing target identification by two to five years.

It’s difficult to conclude how much of a better job someone else might have done as CEO - I suspect many would have done worse though with the same constraints. But, in my view, Luke is taking on something potentially quite interesting - an organisation that is far more capable at finding and developing drugs than it used to be.

Luke’s Leadership: 2025+

I started paying more attention to Luke after Hal left in 2022 and took his BD lieutenant with him - this marked a BD regime change. At this time, Luke started dedicating significant time to BD in conjunction with Tony Wood. He also brought across former colleagues Chris Sheldon, Garrett Rhyasen and others from BD at AZN - perhaps the most highly regarded big pharma in terms of BD. The people who brought Calquence and Enhertu to AZN, now work at GSK.

Luke spelled out some of his thoughts and philosophy around BD to the FT at the end of 2022:

He likes under-appreciated assets in the $1bn to $2.5bn range - assets “hiding in plain sight”

He avoids bidding wars

“Hal did a lot of work on the early stage, which we needed to do, fix the discovery machinery. Tony and I are very focused on: what else do we need now? Right now? And let’s bring it in.”

Chris Sheldon goes into more detail about the BD strategy here:

Notably he talks about how their focus at the moment is on revenue at the end of the decade. This is why I’m confident they’ll hit that £40bn sales in 2031 number, despite whatever concerns there are around LOEs. There’s been a massive pick-up in activity since 2022. Moreover, none of it is panic buying of the sort you typically see at big pharma - they’re well-considered deals for specific assets and capabilities at comparatively low transaction values:

Late stage / Phase III (PYS >£6.5bn):

Sierra (2022) - Approved 2023, PYS >£1bn (GSK)

Spero (2022) - Anticipated launch 2026, PYS >£0.5bn (GSK)

Bellus Health (2023) - Anticipated launch 2027, PYS >£2.5bn (GSK)

Scynexis (2023) - Anticipated launch 2027, PYS >£0.5bn (GSK)

Boston Pharma (2025) - Anticipated launch 2029 ,PYS >£2bn (NFTBC)

Sierra was an excellent acquisition and the asset (Ojjaara in myelofibrosis) is already generating fast-ramping revenue at low cost. Bellus is looking compelling too - that’s the chronic cough asset. Spero and Scynexis are anti-infectives acquired very cheaply but with the potential to contribute materially.

Mid / Phase II (PYS: £multi-billions):

Arrowhead (2023) - Anticipated launch 2029+ (GSK)

Hansoh (2023) - Pivotal studies starting 2025/2026

Aiolos Bio (2024)

IDRx, Inc (2025) - Pivotal study starting 2025

Mid-stage assets are also looking to be additive to revenue before the end of the decades.

Early / Phase I / pre-clinical:

Last there are platform and alliance deals which are more of Tony’s doing (he likes platforms), early stage and longer-term investments:

Wave (2022)

Flagship Pioneering (2024)

Relation (2024)

Muna Therapeutics (2024)

Rgenta Therapeutics (2024)

Elsie (2024)

Hengrui (2025)

ABL Bio (2025)

At the time of writing, biotech stocks seem like they might be coming back into favour after several years out in the cold - we’ll have to wait and see if that holds and what it means for the level of GSK BD activity from here if prices are going higher. Note how active they’ve been in China (Hansoh, Wuxi, Duality, Chimagen, Hengrui) where compelling earlier-stage assets have been available at modest prices.

Concluding Thoughts

Under Emma Walmsley GSK sentiment never quite managed to break out - despite one or two false dawns. There was always something that came along to knock things off track: Blenrep getting pulled off the market, narrowing of ACIP recommendations on RSV vaccination, Zantac litigation, RFK Jr etc - it goes on.

Whether fairly or unfairly, Emma Walsmley also took a lot of heat over the years for not having a science or pharma education and background. With a degree in biology and a career in pharma, Luke Miels doesn’t have that problem. I think there’s a good chance investors will give him the benefit of the doubt - he’s coming into the role as a proven operator in this domain. And in fact on the day of the announcement, the shares did jump. I’ll be watching with interest as to what adaptations he makes to Emma’s strategy. For her part, Emma has said this week she definitely intends to take on one more leadership role, so I’ll also be curious to see where she turns up next.

Thanks for reading.

As always, get in touch if you have any comments or questions. I know that many of you are closer to some of these issues than me, so I’d be interested to hear your thoughts.

EPS does not, of course, necessarily equate to free cash flow or owner earnings. But that’s how most of us look at the world. When GSK was at 8.5x P/E prior to the announcement you can translate that to ~10x P/FCF for the next twelve months based on management’s targets - I find this broadly comparable to other big pharmas where you should add 1-2 turns to the P/E as a rule of thumb.

Includes distribution of Haleon shares.

6-month dosing is not currently in the £40bn sales ambition.