Ottobock SE & Co. KGaA (OBCK)

A 100-year old medtech Hidden Champion has debuted on the market. I take a good look at the moat, the growth opportunities and share some thoughts on the shares.

Friends of NFTBC

When I started looking at recently listed Ottobock (Ticker: OBCK) I was immediately intrigued, so I decided to write about it. Additionally, my impression is that global investors might not yet be especially aware of this German ‘hidden champion’. OBCK, with a market cap of around EUR 3.5bn, is the market leader in human bionics - most notably prosthetics, but also in tangential fields. The business itself has a long and colourful (if not especially public) history and its family owners have, I believe, built some quite compelling moats around it.

For various reasons I’m slightly behind schedule on getting this post out the door. Part of the reason for that is that I have been looking at OBCK fresh and the more I learnt, the more questions I had. There are numerous moving parts to understanding this business1 and various dynamics at play - I wanted to be sufficiently comfortable about them before writing to you about it all. Having done this now, one thing seems clear to me: OBCK is a very hard business to compete with and may even be a candidate for the most moaty business I’ve written about so far at NFTBC. In some instances, OBCK has exceptional pricing power. But I’m also pleased to note that in such instances its products bring tremendous value to their users - so long as reimbursement and access can be established. That’s all part of the story too. It’s also a largely recurring revenue business model with plenty of avenues towards durable growth - we’ll go into all of this.

My aim with this post is to try to bring OBCK newcomers up to speed in 40 minutes or so and to point you in the right directions should you decide to follow up with your own research. As a business with many thousands of SKUs, there is a lot that I won’t cover here, but I’m happy to continue the conversation elsewhere. Here’s what the basic layout will look like:

Introduction (free to read)

Background (partly free to read)

Basic thesis: Strategy, Moats & Optionality

Governance Structure & Management

The Business Today: Overview, Financials & Competitors

B2B: Products & Markets

B2C: Ottobock Patient Care

Risks / FAQ

Conclusions: 2026 & Beyond, Initial Thoughts on Valuation

While I do not yet currently own OBCK, I shall discuss later some of the conditions that could lead me to take action - potentially in the near term. As always, I will inform paying subscribers when and why I decide to acquire OBCK shares - should that time come. If you’re new to NFTBC, please check out this page for more information about the NFTBC approach and what to expect. I’ll no doubt make some mistakes in this post, which I shall endeavour to correct over time. With that, let’s get going.

[NFTBC does not give advice - please do your own research. I do not currently own Ottobock shares].

Introduction

For the last 100 years, OBCK has led the field in developing and commercialising next generation prosthetics. Most notably, in recent times, important developments include the microprocessor knee (MPK) - a breakthrough innovation that enables above-the-knee amputees to move with a more natural gait, safely tackle everyday tasks and even engage in much more adventurous pursuits. Today OBCK is the largest and most important prosthetics OEM by a wide margin - about 40% market share. Additionally, OBCK has been investing heavily into tangential fields in order to open up new and potentially even larger markets - more on that later.

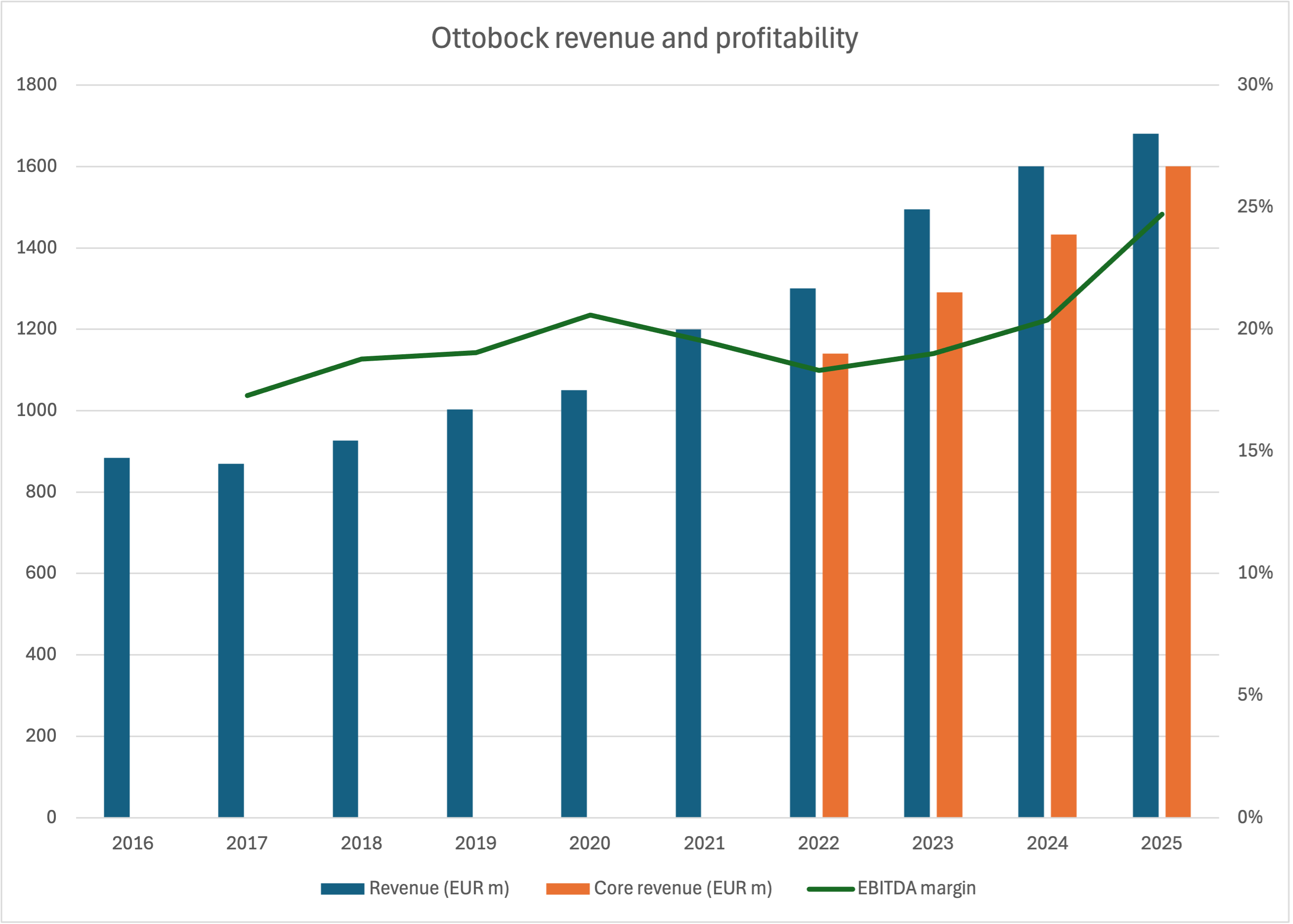

While the company has only been listed since October 2025, we have sufficient information to know that OBCK has been a relatively consistent 7-8% top line grower for a long time. Revenue was under EUR 100m (equivalent) in 1990 - implying around 17x in 35 years or greater than 8% CAGR.

The numbers in the last several years also mask a more promising underlying story of 3-year ‘core’ organic revenue growth of 11%. With the company now close to having completed a series of non-core divestments, these revenue figures are now converging. Another compelling dynamic at play is the recent trend of margin expansion, which management expect to continue - we’ll get into some of the reasons behind that later. But first, some background…

Background: History, the Näders, EQT & IPO

A Little History

For the particularly keen, there is a three volume book on the history of Ottobock. I’m afraid I haven’t read it - but I don’t think we need to go into deep history here.

The founder, Otto Bock, started the business in Germany in the wake of World War I. At the time, prosthetics were one-off crafted items, and as far as processes go, this one was highly inefficient given the elevated need at that time. Bock industrialised the process turning it into the serialised mass production of components. In time, the business came to be managed by Bock’s son-in-law Max Näder. Under Näder the business continued to launch a series of important innovations including the breakthrough Jupa knee joint with braking mechanism, myoelectrics that help users grab objects, plastic prosthetics as well as the modular system that underpins modern prosthetics today. In 1990, at the age of 28, Hans Georg Näder took charge as CEO - the grandson of Bock and the son of Max Näder.

Hans Georg Näder (HGN)

Given the various Näders involved in this story, I shall refer to Hans Georg as HGN from hereon to avoid confusion.

HGN has taken a fair bit of heat in the German business media over the years, for example for apparently taking cash out the business, raising debt and for buying shipyards, breweries and such others things that eccentric billionaires are wont to do. There’s even a website dedicated2 to posting largely negative content about the man - if you decide to research OBCK you’ll probably find it quite quickly. I’m inclined to leave such tittle tattle to one side. For one thing, up until the point when EQT acquired a 20% stake in OBCK, HGN basically owned the business outright and was free to run his affairs in any way he saw fit. One thing worth noting (and that OBCK commented on some years ago) is the importance of drawing a distinction between Ottobock SE & Co. KGaA (i.e. OBCK) and the family holding entity Otto Bock Holding GmbH & Co. KG - it seems journalists have not always done this. In the end, the latter changed its name to Näder Holding GmbH & Co. KG perhaps in part to help address the confusion. Needless to say, the affairs of the holding company and the other assets it owns, are not directly relevant to OBCK shareholders except to the extent I shall identify shortly.

With that out of the way, let us now consider some of the great strategic decisions made by HGN - if you’ll pardon me for going off on a brief tangent. The biggest risk with successful family owned businesses is the possibility of dilution to management quality over time. So it’s notable that the grandson of the founder has been able to act with great strategic foresight. OBCK’s most important product of the last 25 years has been the C-Leg microprocessor knee. The first ever fully adaptive MPK, it’s been fitted more than 100,000 times and continues to be the market leader (after numerous iterations and branching products). Since the turn of the century, OBCK has compounded MPK units at 20% per year. While they don’t break it out, I think we can infer that the C-Leg is a substantial percentage of total revenue. The MPK was originally pioneered by maverick Canadian engineer Kelly James in the early 1990s. Per Ottobock lore, HGN waltzed into a prosthetics trade fair and penned a deal with James there and then, having recognised the significance of the technology.

The OBCK PR department seem to make a big deal out of this in various places, which made me kind of suspicious and drove me to try and verify it. And… it’s true: Kelly James independently retold the same in an interview with his alma mater University of Alberta 15 years ago. The context is telling and worth expanding on:

[Kelly James] travelled around the world to conferences trying to sell his leg to a manufacturer. At trade shows, he walked from booth to booth with his prototype slung over his shoulder. But most manufacturers were reluctant. What James was selling was, in retrospect, ahead of its time. “They all said, ‘I don’t know, it’s pretty complicated.’ Remember, in 1992 people didn’t know anything about computers.” James persevered, even when people in the prosthetics field told him the idea was crazy. But in 1992, German prosthetics manufacturer Otto Bock approached James at a trade show. In a closed-room meeting with the company’s owner and top engineers, they made James a deal for the leg, on the spot. “What really surprised me about the meeting was that they were so respectful of the leg. After I had talked to all the American companies and they had just slammed the door in my face, I spoke to the German company and they were so, ‘Wow, this is really amazing, and how did you do it?’”

But there were obstacles to overcome along the way. Otto Bock nearly decided not to manufacture and sell the leg after one doctor’s experience. The doctor, an amputee, was impressed with the leg after wearing it around for a couple of hours. But when he took it off to put his old prosthesis back on, he fell down the stairs. The C-Leg was too good in the sense that it was dangerous for someone to readjust to a less-sophisticated prosthesis. Otto Bock executives were upset, says James. “They were saying, ‘This is a no-brainer, we’re not going to build this knee … we can’t put amputees at risk.’”

James managed to convince them otherwise. “Let’s just change the number of phases the knee goes through during a step,” he said. The idea of easily tweaking a few lines of code for the knee’s microchip was an eye-opener for Otto Bock. Over time, the phases of the knee evolved, eventually eliminating any phase where the knee is locked and anything that made the knee too complicated for users to figure out. The knee’s simplicity is one of its main selling points. “You don’t read a manual, you don’t understand it, you don’t think about it—you just walk,” says James.

It’s kind of interesting to me because HGN was still relatively young and had only been in charge a couple of years. Would a professional salaried CEO have made the same decision? Kelly seems to suggest not. In the event, OBCK spent 5 years in development and launched the C-Leg in 1997. And it’s taken decades to build the case for reimbursement and grow access - a journey that continues. It’s tough to imagine these sorts of long-range investments being made by a non-family controlled business.

Keep reading with a 7-day free trial

Subscribe to Notes From The Beauty Contest to keep reading this post and get 7 days of free access to the full post archives.