Procept Biorobotics (PRCT)

Niche player or new gold standard? Weighing up the arguments, reflections on the strategy, thoughts on valuation.

Friends of NFTBC

I must say I never envisaged writing to you on the topic of benign prostatic hyperplasia (i.e. enlarged prostates), yet this is precisely where I find myself today. Investing frequently leads in unexpected directions which is, of course, part of the fun.

We are going to talk about Procept Biorobotics (PRCT), the developer of an innovative automated surgical system for treating BPH. PRCT believes that this system is sufficiently disruptive to become a new ‘gold standard’ in BPH treatment. Currently, the vast majority of those tens of millions of men around the world seeking help for BPH are directed to pharmaceuticals - imperfect ones. With surgical procedures currently only a very small proportion of the overall treatment landscape, there’s potentially a sizeable business to be had if just a little share can be taken from pharmaceuticals - that’s PRCT’s longer-term strategy in a nutshell.

Technically PRCT’s system is a robot and, yes, one that uses AI. The business has been on a trajectory of rapid growth, with revenue for 2025 due to come in around 9.5 times higher than at the time of IPO in 2021. Rapid growth, robots, AI - you’d think these conditions would be ripe for investor enthusiasm. And you’d be right. Following a successful follow-on share issue in late 2024, PRCT investors could scarcely be more excited until just over a year ago. But over the course of 2025 PRCT stock quickly reversed to such an extent where anyone making the bull case risks looking silly.

Despite PRCT’s growth, there are various uncertainties at play. Just to help set the scene, the basic ones include:

PRCT is losing money - when will it stop?

How profitable might the company be and when?

The hyper growth is tapering - what might be a more sustainable rate?

How big is the TAM anyway / is PRCT unrealistic in its stated ambitions?

There had been some signs that PRCT might start to more or less breakeven at the end of 2025, but the company now has a new CEO who has signalled even higher investment levels in the months ahead.

I think it’s an interesting time to be learning about this business - and I mean specifically between now and the end of February. The new CEO, Larry Wood, is the reason I starting looking at PRCT, having followed him over from his previous long-term role at Edwards Lifesciences. At Edwards Larry grew their pioneering TAVR technology into a multi-billion dollar business - progressively building it into a new gold standard in the treatment of aortic stenosis. While very different medical domains, he sees certain parallels with what PRCT is trying to do, having also sat on PRCT’s board for a year before signing on as CEO. It was enough to get me listening anyway. In late February Larry will host an investor day where he will give multi-year revenue guidance and profitability targets. We’ll also get some more information about his sales and marketing strategy as well as updates on clinical data and strategy. I have no detailed predictions for you on how he’s going to set his longer-term targets, except to say that they are likely to be ambitious. So whatever ambitions he spells out next month, I think we should entertain them at the very least.

With that, it’s worth recapping some of the dynamics I like to look for in stocks, here at NFTBC:

Businesses that are trying something differentiated - something worthwhile that is not yet perceived as valuable

Credible and capable leadership who can make it happen

The presence of uncertainty (which investors tend to avoid)

The necessity of patience to let the situation work itself out

Optionality

PRCT seems to fit the bill here. We have: 1) a business that is trying to disrupt current practices in BPH treatment and grow the market in the process; 2) a CEO who has very successfully done something similar before albeit in a different medical domain; 3) doubts about whether it will actually happen or to what extent and when and 4) potentially a very large and long runway depending how well they execute and a strategy to expand into a sizeable adjacency. All in all it could be an interesting multi-year story - and so these are the reasons I’m keen to write about it. The basic plan is to explore these four issues - to kick the tires, as they say. I aim to leave any possible hype to one side and to try to take a sober look at things. I think this is one of those situations where reasonable-sounding arguments can be made by both the bulls and the bears - we’ll look at some of both. That said, I am leaning bullish and have taken a small position.

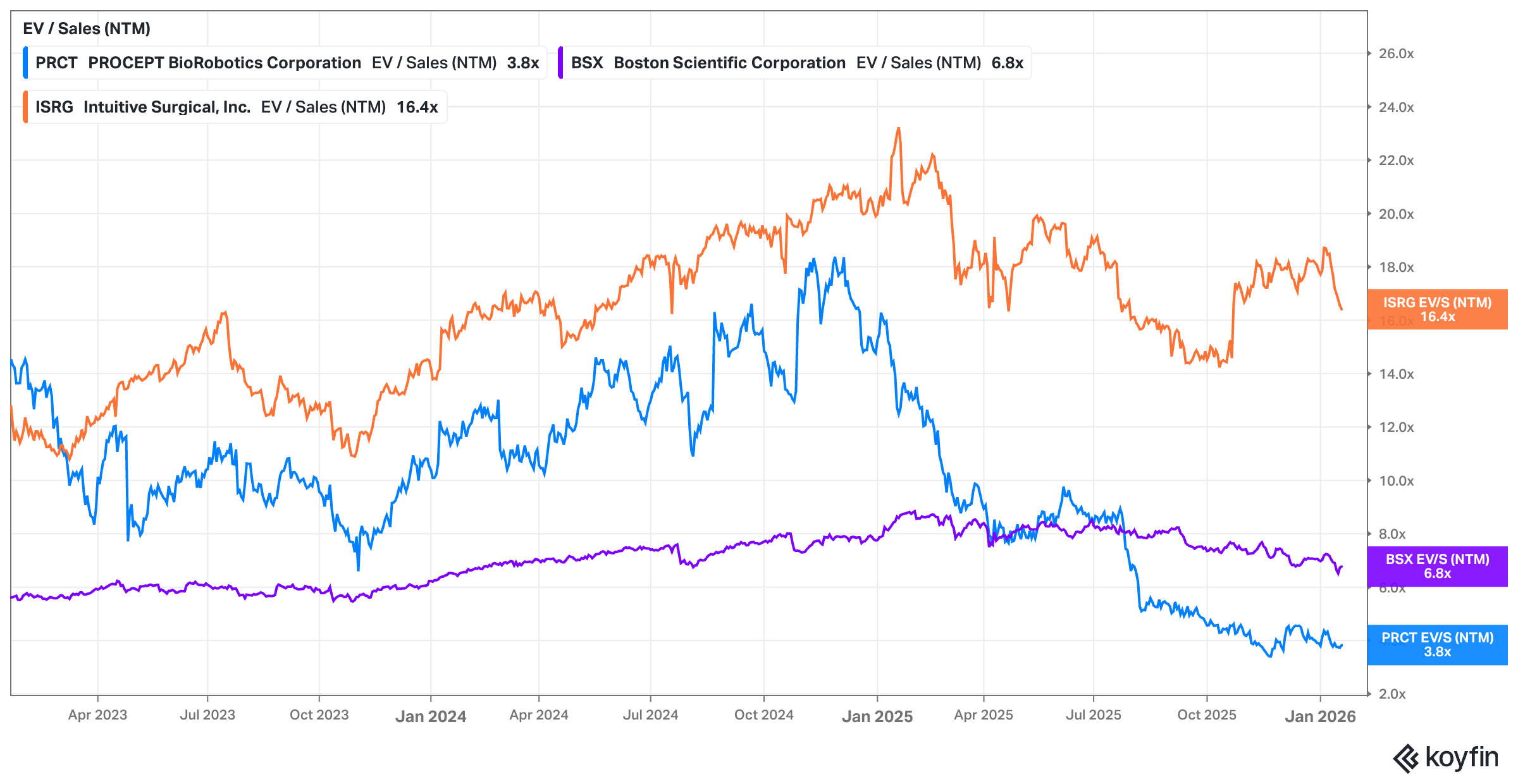

Before we get going, some of you will no doubt already be wondering what PRCT might be worth. This does, of course, depend on the variables highlighted above. We will get into that later and I will share some of my ideas. The good news is that management certainly do intend to make the business profitable in the not-so-distant future, and I think Larry Wood is likely to confirm this next month. But not yet having any earnings to speak of, I can’t show you any earnings-based multiples. So let’s look at EV/sales:

I have included Intuitive Surgical (ISRG) here simply as the largest, most obvious and most successful robotic surgery comparator.1 I have also included Boston Scientific (BSX) as a second comparator. I suspect that PRCT might be acquired before we get a chance to see the story play out - BSX is perhaps the most logical acquirer as a large medtech that operates in the same general space as PRCT. In 2026 PRCT is expected to grow about twice as fast as ISRG and three times as fast as BSX - just to give you a relative sense of where things are.

This post won’t be quite as long as typical NFTBC deep dives, although I anticipate there being more to say in future - including next month. Consider this an exploratory or thinking-out-loud exercise, as part of a longer journey. I will undoubtedly get things wrong, and will endeavour to clear up such issues over time. With that, let’s get going.

[NFTBC does not give advice - please do your own research. I currently own shares in PRCT].

Keep reading with a 7-day free trial

Subscribe to Notes From The Beauty Contest to keep reading this post and get 7 days of free access to the full post archives.