PTC Inc - A Deep Dive (Part 1)

"Putting more wood behind the arrow" / Blessed is the man whose quiver is full of them

Friends of NFTBC. Welcome to deep dive number five.

Thus far at Notes From The Beauty Contest, the ‘Notes’ have primarily concerned severely out-of-favour stocks. Not so many years ago PTC was one such stock which, of itself, makes it an interesting case study for NFTBC. More importantly, the PTC story is still playing out - PTC is in its strongest competitive position since the early/mid 1990s. But what makes things more interesting this time round is that the moat is far more entrenched and growth drivers are multivariate rather than univariate. The durability of PTC’s growth remains under-appreciated in my view.

Introduction

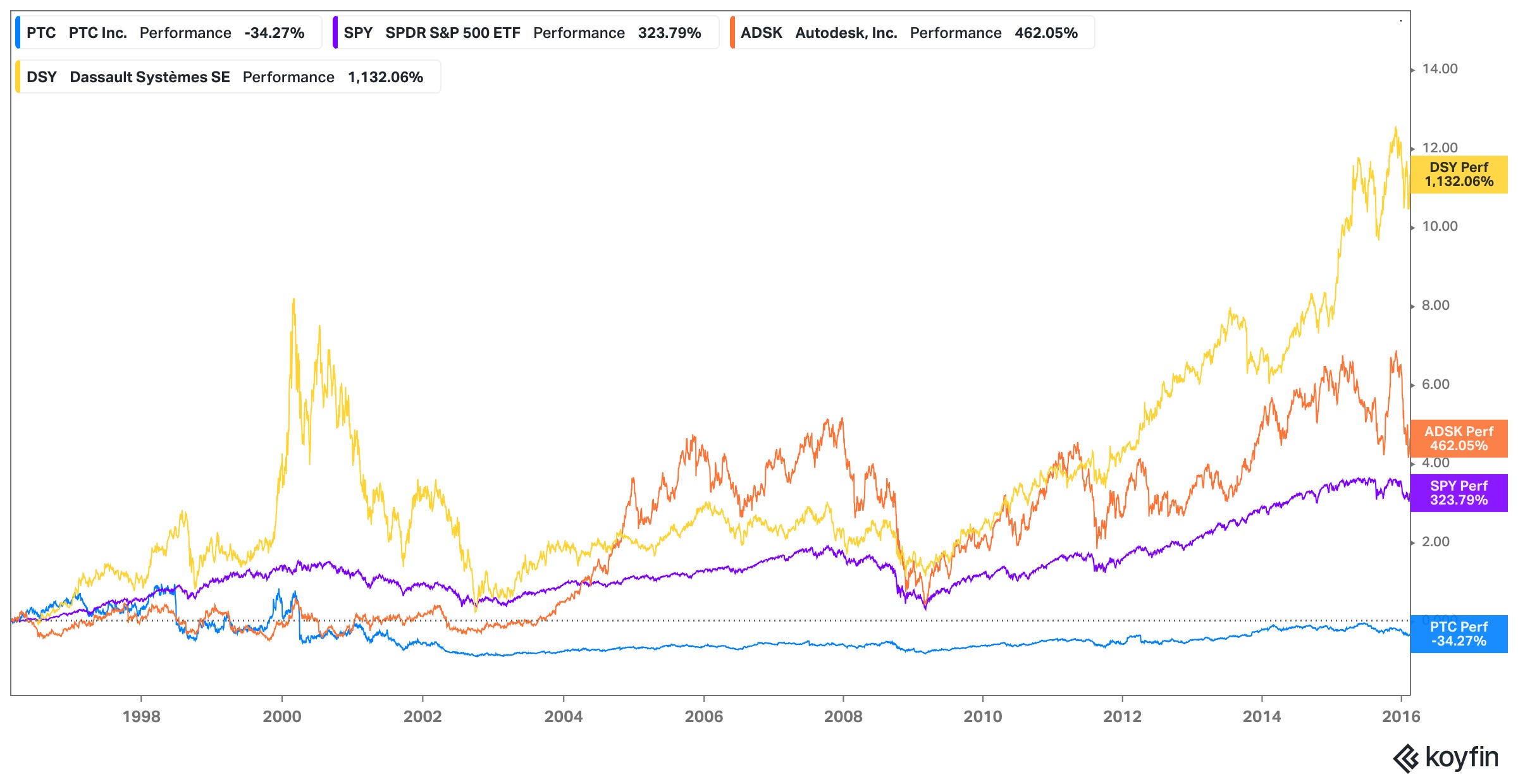

For those not yet particularly familiar, PTC is an industrial software business and a leading vendor of computer-aided design (CAD) and product lifecycle management software (PLM) to customers who design and manufacture products. 10 or so years ago PTC stock was an extraordinary dog, having underperformed its peers and market indices by an extraordinary margin over an extraordinarily long time:

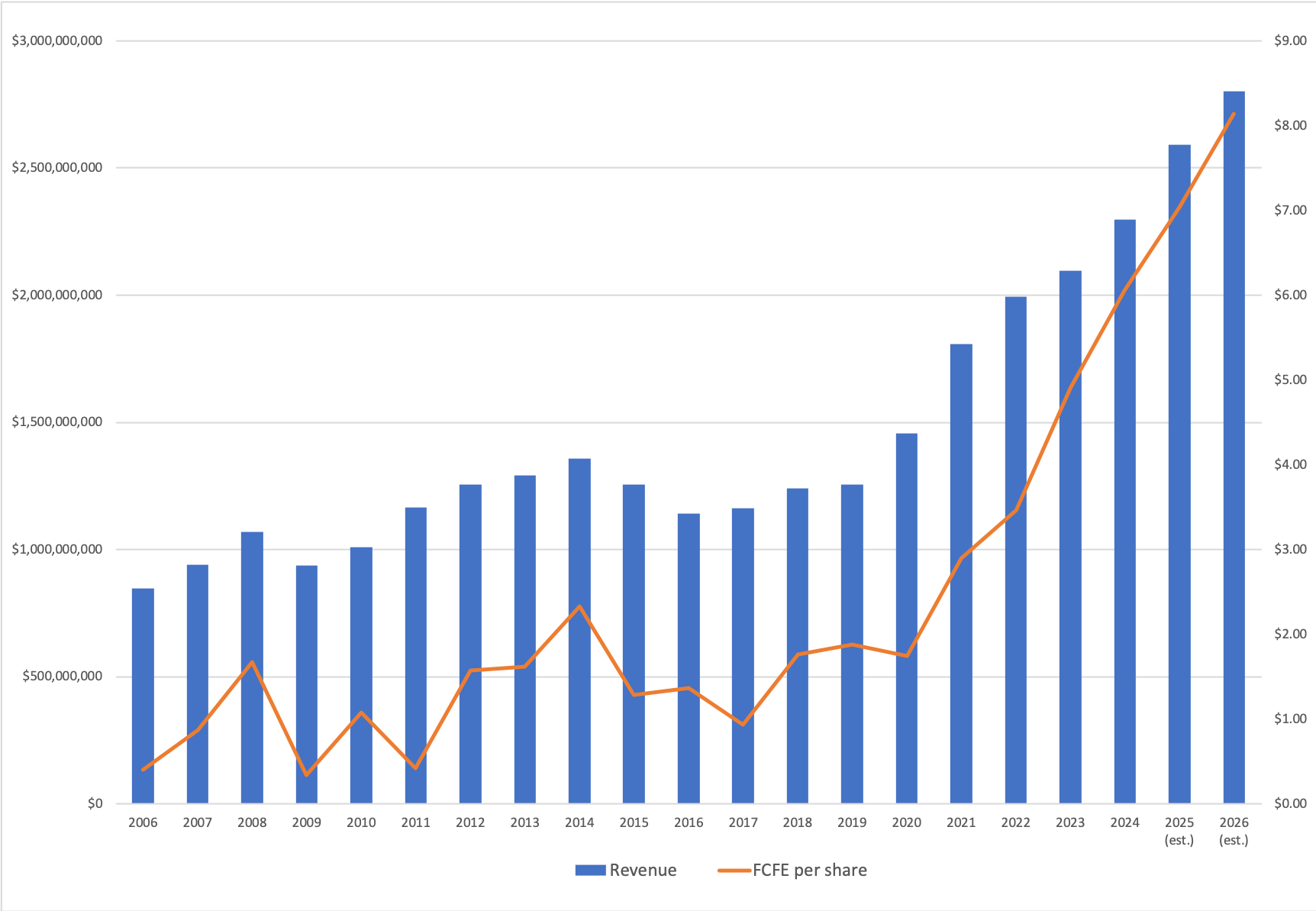

Having once been a hot stock itself and the disruptor in a fast-moving field, PTC had itself been disrupted, facing years of headwinds. We’ll cover all that later. Incredibly, in its 36 years as a listed business, PTC has spent the majority of its time in the doghouse. With a change of leadership and strategy, there eventually started to be cause for hope and some investors began to pay attention starting around 2017. But it would still take years to become fully manifest in the financials. In the meantime, scepticism remained and short sellers continued to make their case.1 Then this happened:

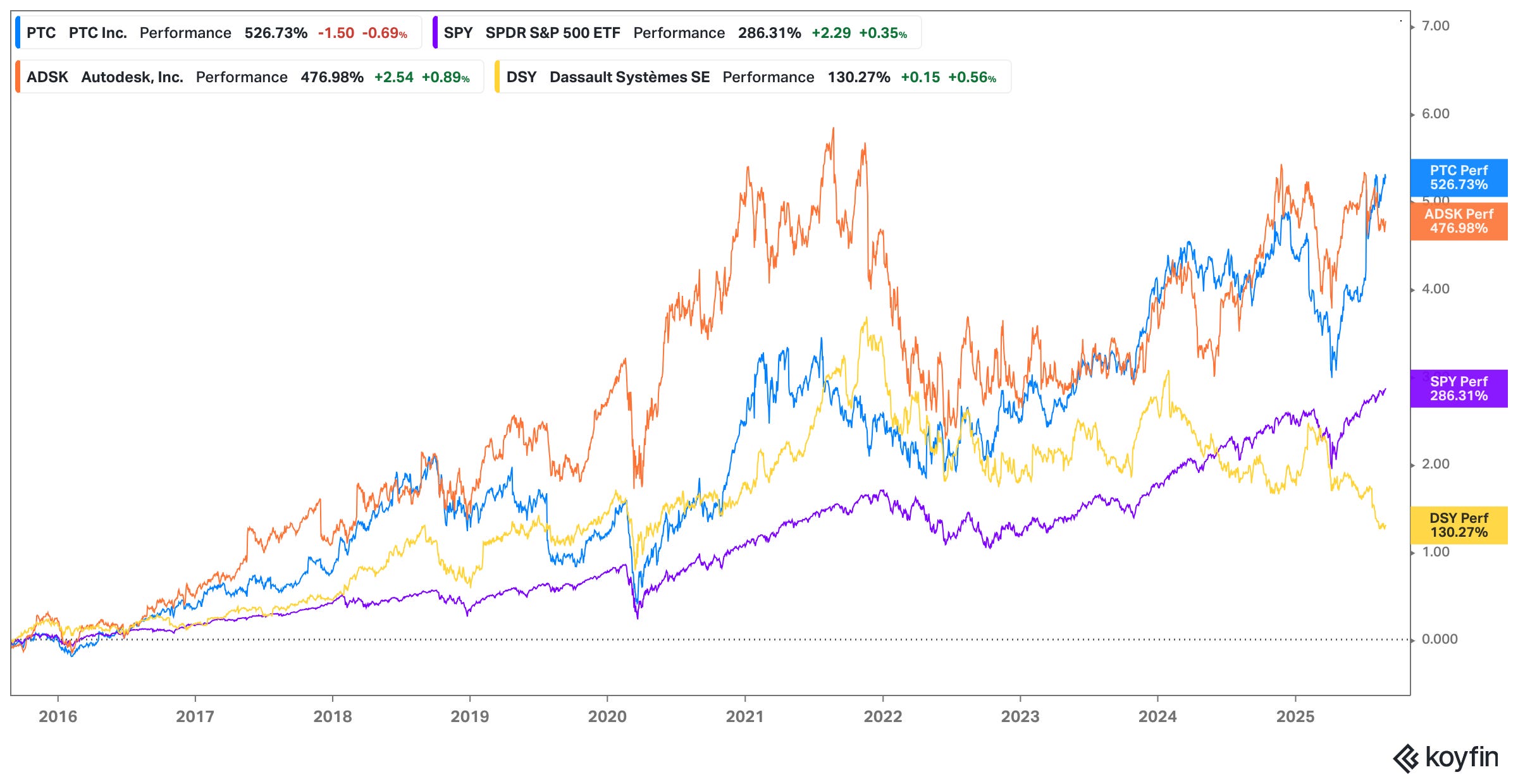

And this:

In the years I’ve been following PTC it has always remained in the shadow of Autodesk (ADSK) and Dassault Systèmes (DSY). Even today with the obvious turnaround in fortunes, investors still don’t seem to talk about it quite as much as the others - and that’s partly why I’ve decided to write this post. As recently as early April 2025 you could have bought PTC shares at a sharp discount to both ADSK and DSY as measured by price-to-free cash flow. In early July rumours began to emerge of ADSK’s interest in acquiring PTC, which caused a significant bump in PTC’s share price - curiously, with ADSK now having distanced itself from any such ambitions, PTC shares have not reverted to pre-rumour levels.

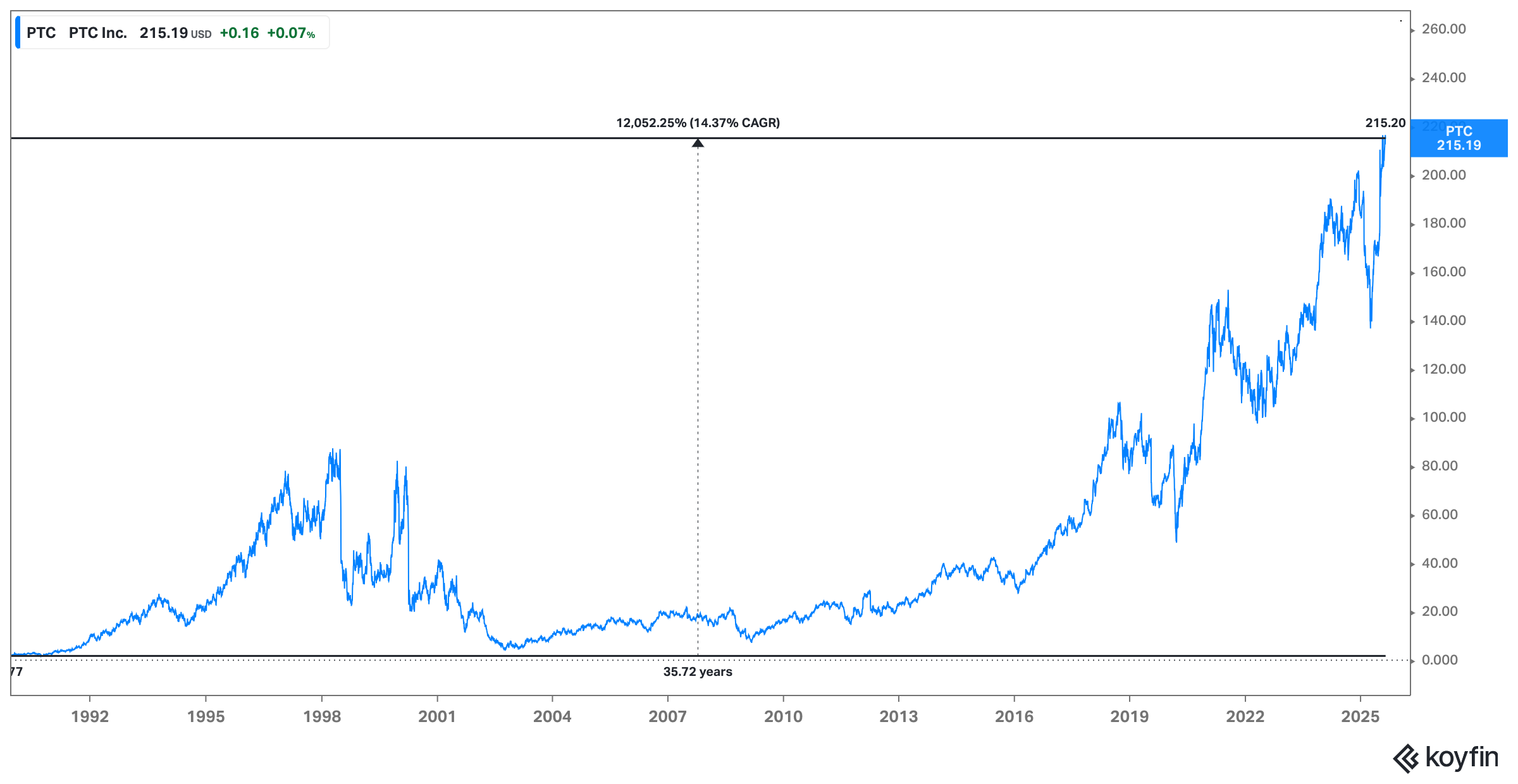

PTC is certainly a business with a bit of history and a bit of baggage - it’s not one of those beautiful compounders that has done 20% year-in-year-out since IPO. But even with 20 years spent out in the cold, PTC has still somehow compounded at more than 14%, which isn’t bad.

In this deep dive I’ll start by reviewing how PTC got to where it is today. Notably, PTC’s software has always been the benchmark in parametric CAD modelling capabilities (the clue’s in the name: Parametric Technology Corporation). Even during PTC’s darkest years of disruption, the company managed to hang onto a foundation of large customers who were there for those capabilities - an important indicator of the incredible stickiness of CAD software. But there are lessons too: being the best at one thing isn’t enough, even if that thing is an important one. So what I really want to talk about is PTC’s present and its future - this is the focus for Part I.

PTC’s last CEO, Jim Heppelmann, was a strategic visionary and spent years assembling the most complete and coherent portfolio among peers. Grounded in inter-operability and the creation of a ‘digital thread’, PTC’s solutions help manufacturing companies to act with increased agility across the entire lifecycle of their products from design through to servicing. And in a world increasingly defined by software, regulation and ever-faster moving competition, product companies are faced with a choice: sink or swim. PTC provides the tools to help them swim. And thus, PTC has completely transformed its defensible position relative to the past while growing in both CAD and PLM well above-market over the last six years. From this position of strength, PTC can continue to execute on its playbook for above-market growth:

Up-sell

Seat expansion

Cross-sell

SaaS conversion of existing customer base

displacing legacy/outdated software

digitalising previously undigitalised processes

taking share from traditional rivals

As it stands today PTC is a high margin business with the vast majority of that business recurring in nature. Additionally the growth algorithm is robust and the runway long for double digit ARR growth ahead of costs. But did Heppelmann get everything right? Perhaps not. In the 1990s and early 2000s, PTC had an over-optimised sales strategy, run at the expense of technology and innovation - ultimately leading to years of underperformance. Arguably under Heppelmann things went just a little too far in the other direction. PTC’s new CEO, Neil Barua, believes that PTC could be performing even better than it has been, with a re-orientation of the sales strategy and aligning the business around key verticals in order to better serve customers - “putting more wood behind the arrow” as he often likes to say. And PTC isn’t short of arrows either, so we can add a little extra sparkle to Barua’s corny metaphor: Blessed is the man whose quiver is full of them (Psalm 127:4–5). Multiple growth drivers plus a possible acceleration if Barua and his team can execute well.

Thesis

The thing about long runways is that we investors tend undervalue the genuine ones. My purpose with this deep dive is to explain why I think PTC’s is one of the genuine ones. But there is more - PTC has several important layers of additional optionality, which aren’t currently at the forefront of the discussion:

Keep reading with a 7-day free trial

Subscribe to Notes From The Beauty Contest to keep reading this post and get 7 days of free access to the full post archives.