Regeneron

Thoughts Following Q1 '25

Notes From The Beauty Contest is a new investment blog that views current market dynamics through Keynes' newspaper beauty contest analogy. At NFTBC we will share deep dives on stocks, emphasizing a philosophy of "faithfulness" rather than trying to play the game.

Friends of NFTBC. Those of you who follow REGN will probably have seen yesterday’s Regeneron results - you can find them at this link and the presentation slides here. For anyone new to NFTBC, I would suggest checking out the NFTBC intro, as well as the REGN deep dive (as always, please do your own research):

Regeneron Pharmaceuticals (REGN)

Notes From The Beauty Contest is a new investment blog that views current market dynamics through Keynes' newspaper beauty contest analogy. At NFTBC we will share deep dives on stocks, emphasizing a philosophy of "faithfulness" rather than trying to play the game.

REGN First Quarter 2025

Outside of Dupixent (which we already knew about via Sanofi), the results were unexpectedly weak on both the top (-3.7%) and bottom line (EPS -14%). Although it’s always worth remembering that management never give sales or earnings guidance, so investors are left to calibrate their own expectations. REGN almost always exceeds the market’s expectations so yesterday was a big exception.

I don’t intend to do a full rehash here as that would add little value to what is already out there. We’ll focus instead on some of the more notable points and also consider if there is any long-term signal lurking among the noise.

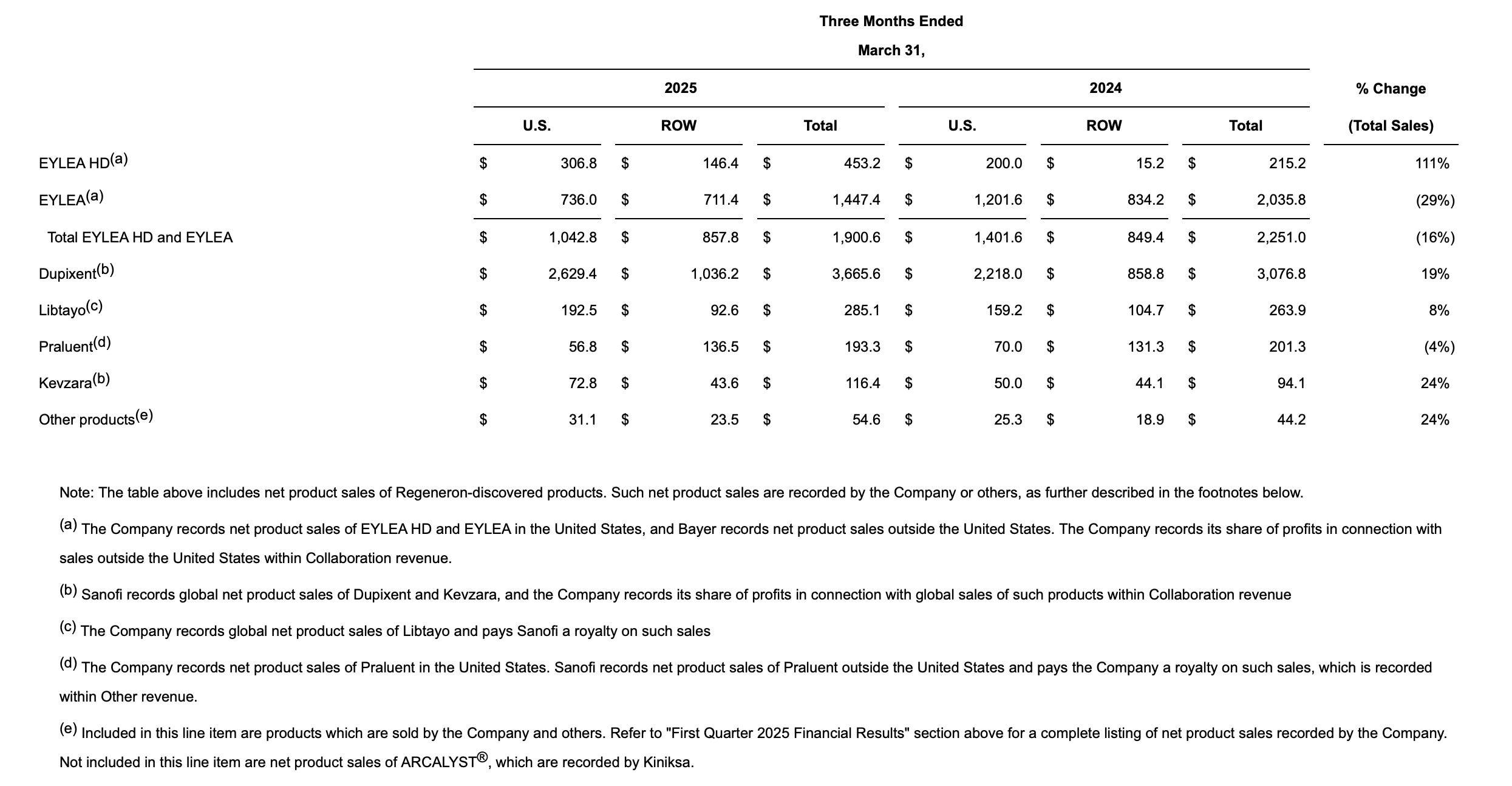

Eylea

Total US Eylea franchise sales declined by 26% relative to expectations of nearer 17%. In particular Eylea 2mg declined by an extraordinary 39%. If you’ll forgive the positive spin, one of the first things that occurred to me is that it’s kind of impressive that REGN’s total revenue should only decline by 3.7% at a time when the very line-item that has defined the company for over a decade should suffer a drop of such sudden violence. It confirms what the company has been trying to tell us for some time - there’s more to REGN than Eylea. So what happened?

We already knew about the elevated inventory at Q4 and about the increasing competition, so no need to discuss those. We had a brief preview when Roche reported its Q1 earnings recently (Roche being the main branded competitor with their drug Vabysmo) - Vabysmo missed expectations and unexpectedly declined quarter-over-quarter. Roche attributed the miss to a funding gap arising in charitable foundations for co-pay assistance in the US - with less assistance available to those who need it, some patients have been forced to switch to cheap off-label compounded Avastin injections (a cancer medicine that does the same thing, but not as well). More details emerged on REGN’s earnings call and it’s worth quoting Len at length:

Just for the benefit of everybody, let me just remind everybody how all this works. When you're under commercial insurance and you're younger than 65, if you have a copay in your insurance program, sponsors that people like Regeneron can directly to a patient supply copay assistance in the form of a coupon, et cetera, et cetera. When a patient turns 65 and if they go on Medicare, which most of our patients getting intravitreal injections are, those patients they are responsible for a copay typically around 20%, if they're in plan old Medicare, it varies somewhat if they're in Medicare Advantage. Some people, many people, have insurance, supplemental gap insurance, AARP, whatever you want to call it, which covers these copays. But there are still others who don't have the insurance and can't afford the copay associated with an injection of an anti- VEGF agent, for example.

The government has indicated that companies can be part of the safety net, if you will, to help patients who need financial assistance. And the way this works is that, companies and others can support independent charitable foundations, who then assist patients with retinal disease regardless of the drug they need. The foundations take in financially eligible patients and give out the assistance that they can afford to give out on a first come first serve basis. And so there is no direct relationship. If we give money to a foundation, it could go to support VABYSMO, it could go to support PAVBLU, it could go to support EYLEA, it could go to support, in fact, in these funds as they're constructed today, it could go to support the drugs for geographic atrophy.

There's no connection as there shouldn't be in what we give and then how the foundations build out the resources. We would like to help as many patients as we can. And it turns out, we probably was the, if not the sole, the vast supporter of these foundations in the recent history, we're talking about having given large sums of money in the neighborhood of over $400 million last year to do this charitable work. As our commercial outlook in the field has changed, as our resources have changed, we looked at this and said, we'd like to continue doing this, but we can't do it all ourselves. We'd like to help as many people as possible. And so we're trying to come up with a way where others and Regeneron could make sure that people in need get the drug copay support without regard to what drug they actually choose or the doctors choose.

And one of the things that we've come up with is sort of a standard thing that's done. We all have seen this in our charitable philanthropic efforts. We're considering a matching program where Regeneron would put up and say, we'll put up X dollars to some amount, and that people – depending upon other people putting up, we would match their contributions. We would hope that this might stimulate others to be more philanthropic than they've been. We are working through the mechanics of this with the foundation. When this all can get launched, we hope in the not-too-distant future. Whether or not others will step up to the plate, I'm not sure, but we certainly hope because patients do need this.

The context here is that Vabysmo has now taken over leadership from Eylea 2mg. And the translation: REGN is sick of funding a disproportionate share of Vabysmo’s growth and they’re pulling the plug until Roche starts being more civically-minded. With a 6 percentage point share gain for Avastin in Q1, both REGN and Roche suffered headwinds (although it’s worth noting that Eylea HD was the only branded drug in the category to grow quarter-on-quarter). Clearly, REGN is trying to force behaviour change at Roche. Will it work? We’ll see.

The second banana skin to land in front of Eylea was the announcement that the FDA has issued a Complete Response Letter for the Eylea-HD pre-filled syringe. Due for approval in the US around the mid-year point, the HD PFS is the single most thing that will level the playing field with Vabysmo and re-accelerate the franchise, so to see a CRL show up is frustrating. It’s worth quoting Len at length again:

I think, you have to understand a little bit of detail on the processes and what happens, in that when the FDA is reviewing your submission for an approval of a new device, we don't necessarily make all the components. And in this case, we don't make all the components. You might be buying a stopper from somebody, some glass from somebody else, a needle from somebody else and so forth. And we have the design and then we have an assembly. When the FDA has questions about one of the components, that's what's referred to as a drug master file. They go to the holder of that drug master file. Let's say, it's somebody who makes one of the components, the FDA has a question, well, how do you guys do this, and then the holder of the master file responds to the FDA.

By rule, we are not partied to that up and back between the FDA and the third-party component supplier. The reason we're not partied is because, most of the time these questions relate to general practices in which the supplier is not only supplying Regeneron, they might be supplying 20 other pharmaceutical companies, which is, in fact, the case in some of these DMFs we're dealing with here.

So that's the general tone of things, the questions get asked. In this particular case, based on our phone calls after we received the CRL last Wednesday, we realized that nobody had gotten these questions until the day of the CRL or a day before, literally after the CRL. In any case, based on our conversations with the FDA, we believe that there's one key issue that is left to resolve. There are few other minor ones, which I think were just clarifications.

But the one key issue relates to a supplier, and the supplier has told us that the FDA asked for some data. They have all the data. They expeditiously supplied it. Now of course, we don't know the data because we can't be involved by rule in that process. We take it, that word, that they think that they have satisfied the agency. Of course, the FDA has to review this. They could be up and back. You said this, well, we really wanted that, maybe have more of this and so forth. So that leads to a little bit of uncertainty on how fast this could all get resolved. We do have commitments from the FDA that they will move expeditiously as well, that doesn't mean they'll approve it, but they will review quickly the data that's submitted and have a up and back, because they recognize, I think, the importance in advance of the prefilled syringe being a better way of administering the product than out of a vial for patients getting intravitreal injections.

So boil all that down, how long can this take? It could go quickly. As you said, the last time this happened, it took a few months. It could go longer. We don't think there's a reinspection involved. It's not an issue related to that. So we don't think there will be these in turn of a long timelines for that. But we'll know more in the coming weeks or months, and we will hopefully get it across the finish line in a short while, but we'll try and keep you posted once we know what the FDA is really up to. I'm sorry that that's a little indefinite, Tyler, but that's the nature of the process.

The bottom line is that the issue appears to be well on its way to resolution - there are no questions about the drug or its efficacy, for example. Further questioning on the call elicited that exactly the same syringe device (with the same components) is the one that is currently approved and marketed in Europe. As Len says, hopefully they’ll get it across the finish line soon.

Margins

One thing that stood out was the decline in earnings relative to revenue. Eylea 2mg is, itself, a very profitable product so that’s part of the story, but only the minor part. It’s no surprise that REGN continue to invest heavily in R&D (+6%), so that’s a big part of it. But the surprise was the decline in gross margin from 89% to 85%, which in the 10Q was attributed primarily to inventory write-offs. It’s unclear what they’re writing-off however. Presumably Eylea 2mg inventory, although I note it has a shelf life of two years. Unless, perhaps, they still had some leftover REGEN-COV sitting around just in case. The good news is that the big earnings hit seems to have less to do with operating leverage around the 2mg decline, and more to do with one-offs and future investment. I suspect many peers would have simply ‘adjusted’ the write-off out of headline earnings.

Pipeline Notables

One of the things that has caught my eye this year is the emergence of itepekimab (REGN’s IL-33 antibody) as a possible new ‘pipeline in a molecule’. Itepekimab (which is shared with Sanofi) is due to report pivotal data in COPD this year, and with a potentially larger applicable patient population than Dupixent in that disease. The news this quarter was that they’re taking itepekimab into phase III for chronic rhinosinusitis with nasal polyposis, and that’s in addition to PoC trials for chronic rhinosinusitis without nasal polyposis and non-cystic fibrosis bronchiectasis. And, per comments by made George yesterday:

We're also very excited about the opportunity in asthma because the data is very strong there. And I think that, depending on the COPD results, we might be considering moving into that space as well because the genetics there is also very, very strong.

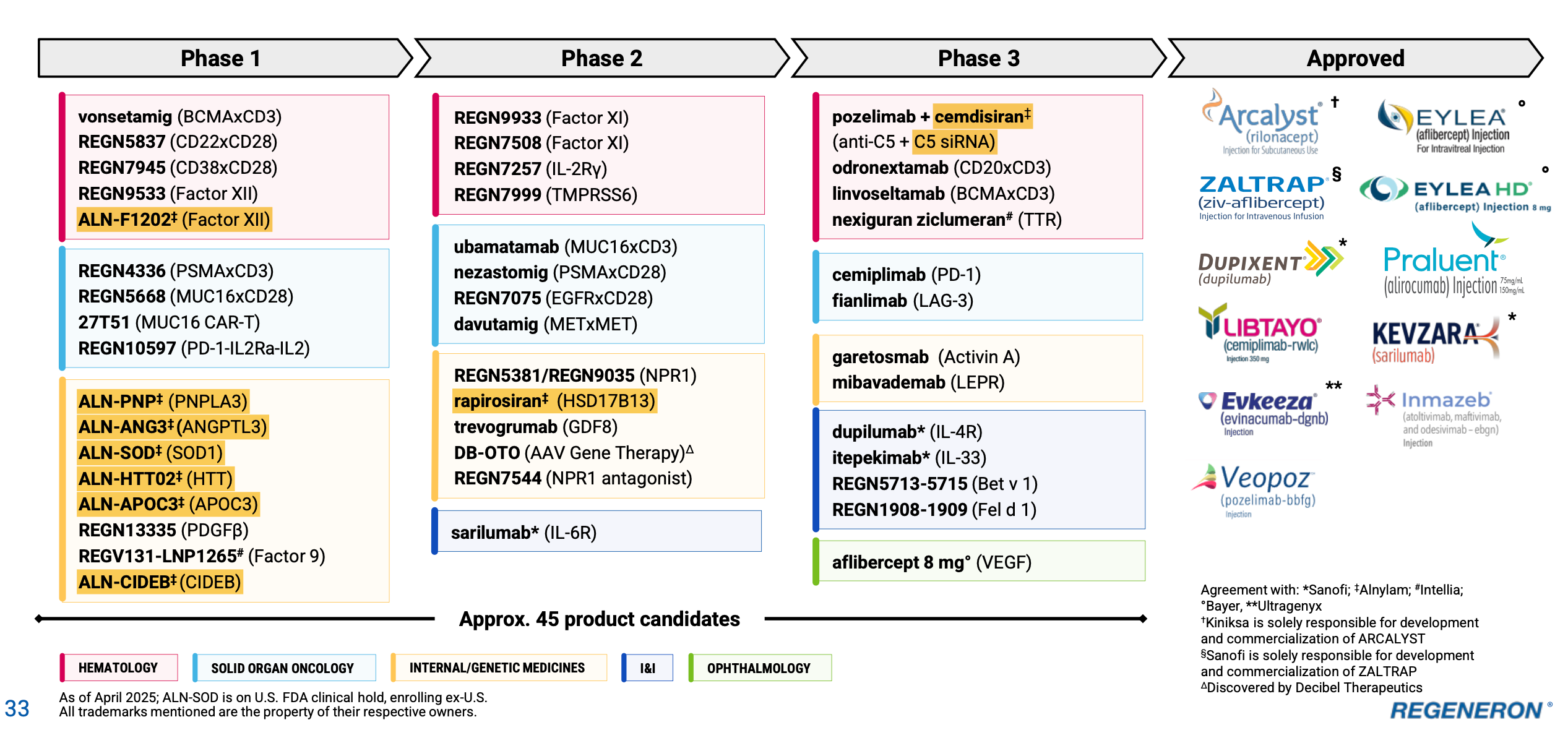

A second thing that’s really starting to draw my attention, at this stage, is just how many siRNAs they have coming into the pipeline (highlighted yellow):

There are currently 9, up from 7 last quarter - the two new ones are CIDEB and Factor XII. All of these arise out of REGN’s partnership with Alnylam, which I did not visit in much detail in my deep dive - it’s an emerging story and driven very much by insights from the Regeneron Genetic Center (which I did cover). Alnylam is worth a deep dive in its own right, being of comparable quality to REGN in terms of R&D productivity - and this collaboration is something certainly to monitor in increasing detail from here. REGN is currently known as an antibody company, but it probably has the third biggest siRNA pipeline now (after Alnylam and Arrowhead) - correct me if I’m wrong. While it’s hard to model with any kind of precision, this part of the pipeline could well evolve into one of the most valuable parts of REGN in future, yet there is next to no value ascribed to it today - with siRNAs constituting ~40% of the phase I pipeline, it only makes sense to view it this way. You might also notice on slide 32 of the Q1 deck two additional siRNAs highlighted as pre-clinical (MAPT and SNCA), while RGC has recently suggested they’re working on a pain siRNA too. It’s increasingly difficult not to notice all these siRNAs!

The last thing I’d like to bring up here is REGN5381, an NPR1 agonist. This one has been in the back of my mind for a while. During a sell-side conference in 2022, Len was asked if there was something exciting in the pipeline that investors weren’t paying attention to. This was his answer:

There are lots of things. Shall I pick one for you? I think we have a very interesting early play in the heart failure arena, which nobody is paying attention to.

He was talking about REGN5381. I don’t think there has been a single question about it in the last three years in the dozens of investor and sell-side calls, yet Len says it’s one of the things he’s most excited about! This is how REGN works - there can be something quietly sitting the pipeline for a while and then suddenly it leaps out into the spotlight with major promise. The Factor XI antibodies are a recent example of this. I wonder if 5381 could be another and I’m bringing it up now because in addition to heart failure, REGN have just begun PoC trials in hypertension, a potentially massive indication. And it probably comes as no surprise that RGC has genetic validation on this target, as you can read about in this recent Nature paper.

Where Next?

When I posted the deep dive in February I suggested (without predicting) that the shares could fall another 25%. As I write, we’re around the minus 15% mark. Could we go lower? Quite possibly - I don’t know. As noted by JM Keynes, there are two principal lenses through which one might try to pick stocks. The first is the ‘beauty contest’ approach where one endeavours to predict where a share price will go from one week/month/quarter to the next, depending on what you anticipate other investors might do. I would argue this approach is the prime determinant of REGN’s share price fortunes today or for the time being. The other approach is to employ a philosophy of ‘faithfulness’ and to hold onto businesses you believe in through periods of disillusionment - given the inherently unpredictable nature of the world, it’s a fairly rational approach, especially as regards those businesses that have a knack of skewing uncertainty in their favour. As a company that figuratively prints lottery tickets, REGN is masterfully good at this. Come what may we will eventually cross the Eylea gap and emerge somewhere quite interesting. There’s also some exciting pipeline news coming up, and no doubt we’ll talk about that in due course. In the meantime, REGN has about 25% of its market cap in net cash - it seems like an excellent time for them to step up the share repurchases with staunch intention.

Thanks again. I don't want to throw a cliché at you here, but it seems incredibly complex to estimate the value of even 1 product in the pipeline. So many uncertainties: is it effective in phase 3, what does the competition do, what is the expected compensation to name a few. This then times 10-20 to evaluate all phase 3 IMPs. Let alone pre-clinical to phase 2. Not a investor but the current PE ratio doesn't seem to factor in much growth. Most 'standard' metrics are quite conservative compared to other biotechnology companies. Seems like the market sees Regeneron like a potential Moderna/BioNTech?