Regeneron: "Past performance SHOULD be the strongest indicator of future performance"

Reflections following Q1 '26 and the recent investor Rountable

Friends of NFTBC

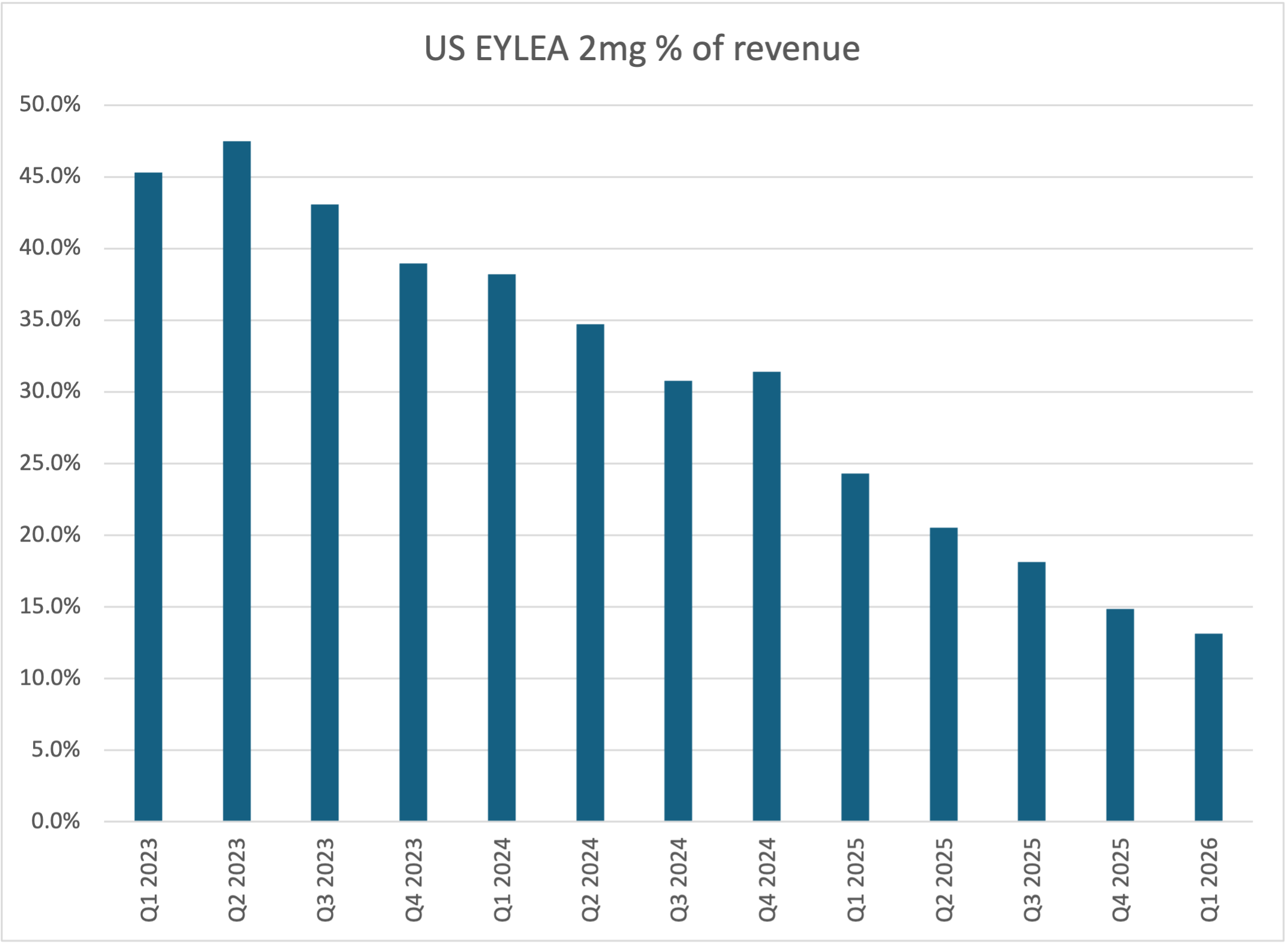

For as long as I have been looking at Regeneron, investors have been fixated on Eylea - specifically on its loss of exclusivity and the threat of competitors. So it’s notable to observe that yesterday REGN reported record Q1 revenue - up 14% on the prior record set in Q1 ‘23 (actually +23% if you rightly exclude one-off COVID revenue). During the same time, Eylea sales have declined from a hair-raising 47% of revenue to 13% today.

Yet, in a clean break with all convention, REGN did not elect to buy their way out of trouble - instead, all of the offsets (Dupixent, Eylea HD, Libtayo etc) came out of their own labs. But with the Eylea LOE eventually turning out to be a relative non-event, investors have now landed on a new fixation: the 2031 Dupixent LOE. In 2031 Dupi starts to lose some of its key patents and the bears are demanding their pound of flesh five years ahead of time. No matter that Dupi is still growing 20-30% with plenty of runway to go, nor that its IP might stretch a bit longer in the end. If you look at REGN through a conventional biopharma lens, there’s no escaping the conventional diagnosis: major LOEs can only be addressed through M&A or major business development. Trying to actually innovate your way out of such a hole is recklessness of the highest order and should not go unpunished:

This exchange from yesterday captures the dynamic very well:

Analyst

Len and George, my question is for you. So Regeneron spends aggressively on R&D, but the investment community lacks confidence that the company’s candidates will move the needle commercially, in particular versus established competitors. So could you please highlight the pipeline candidates in late-stage development that we’ll have cards turning over in the near term or relative near term, i.e., in the next, I don’t know, 18 months or so that you have the greatest confidence in that can generate multibillion-dollar peak sales that investors will be able to see more clearly in the next 18 months or so.

George Yancopoulos

Can I just say that past performance should be the strongest indicator of future performance. There’s only one company in recent history that’s had its own labs produce two $10 billion-plus blockbusters. And let me remind you that I think you, and probably a lot of other investors, never saw those coming or ignored what we were saying about them. So investor confidence, I think, should in large part be reflecting historical performance and the recognition that where blockbusters come from sometimes for the investor community can’t be directly anticipated. And the best way of producing very important big drugs is by having very exciting molecules across all stages of development that have enormous opportunity.

And if you just look at our oncology programs, whether it’s fianlimab-Libtayo, whether you look at Lynozyfic, whether you also look at odronextamab in follicular lymphoma. These are all potential blockbusters. The C5 franchise is a pipeline in a product, multiple blockbuster opportunities there. Our Factor XI customized approaches are looking more and more exciting, especially based on competitor data using, we think, inferior and less convenient approaches. And we just covered the obesity opportunity, which arguably could become the preferred obesity approach that not only addresses obesity, but more aggressively addresses cardiovascular morbidity.

So I don’t know, it’s hard to think of a more exciting pipeline in the entire industry.

Which is it then: a) the indefensible squandering of company money on R&D or b) one of the most exciting pipelines in the industry? These two poles could hardly be further apart! And perhaps we won’t get a definitive answer until hindsight offers us a helping hand.

With the remainder of this post, we’ll have a look at some of the notable points that came out of REGN’s earnings yesterday as well as the recent C5 Rountable event.

[NFTBC does not give advice - please do your own research. I currently own Regeneron shares].