The Regeneron Deep Dive: One Year On

And some thoughts on the recent quarter (Q4 2025): 'Supi-Dupi', revisiting failed blockbusters, capex, outlook, valuation and more.

Friends of NFTBC

It has been exactly one year since I launched the blog with the REGN deep dive. I thought I would mark the occasion by offering a few reflections on the original post. I have also taken the paywall off for February, so have a read of the REGN deep dive if you haven’t yet and would like to. After that, I shall go into some 2025/2026 commentary for full NFTBC subscribers.

Deep Dive Reflections

The thought occurred to me recently that it might be interesting to do an updated version at some stage. But reading through it again last weekend for the first time in a while, I don’t think that time has arrived yet - most of it I would probably leave as it is. I still believe REGN to be a very special business, and the reasons for that, as outlined, haven’t changed.

In early 2025 I was cautious about the outlook for Eylea but offered no particular predictions for its path that year - naturally, I had little idea that we’d be here one year later with the 8mg pre-filled syringe still yet to be approved in the US. The good news is that approval is finally coming into view - April, we are told. Neither did I forecast 2025’s other negative surprise - the mixed Phase III for itepekimab. But, again, neither did I make much of itepekimab in the deep dive, as it didn’t feel to me like a major driver of the company’s long-term value. Maybe I’ll change my mind about that in future, but I would also note that REGN only has 50% of the economics anyway.

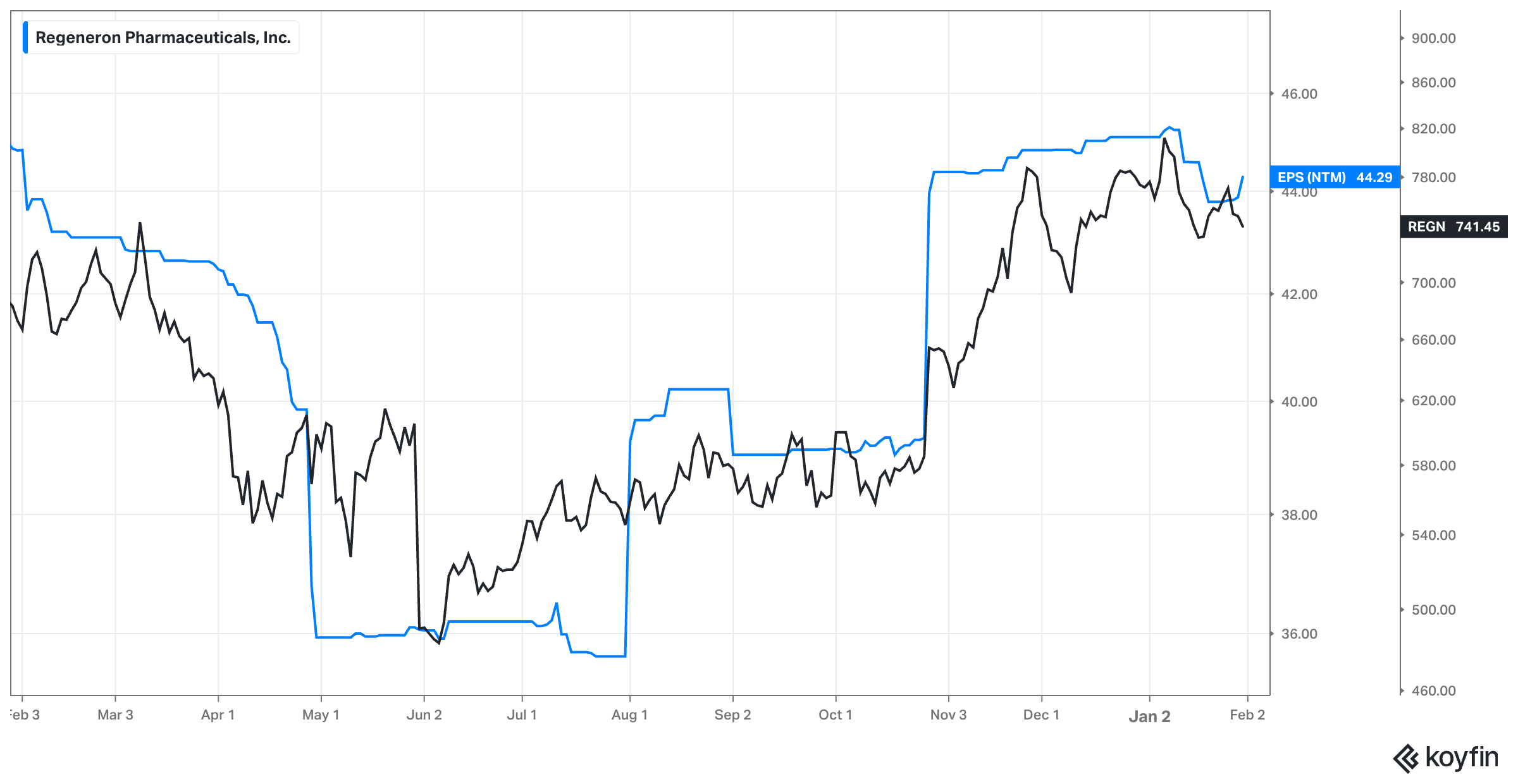

One thing that’s clear is that these events took us on a wild ride with massive swings in analyst expectations for near-term EPS. In the deep dive I noted consensus 2025 EPS of $44.43. In the end EPS came in at $44.45 (adding back the $0.14 non-cash charge from acquired IPR&D - an adjustment that REGN does not itself make but many would). One might even say 2025 was a whole lot of fuss over nothing.

Let’s now talk about some of my more significant reflections, such as they relate to the REGN of the future - specifically where I have changed my mind somewhat or where I might have done things differently. Starting with my 2035 illustration, here’s what I wrote:

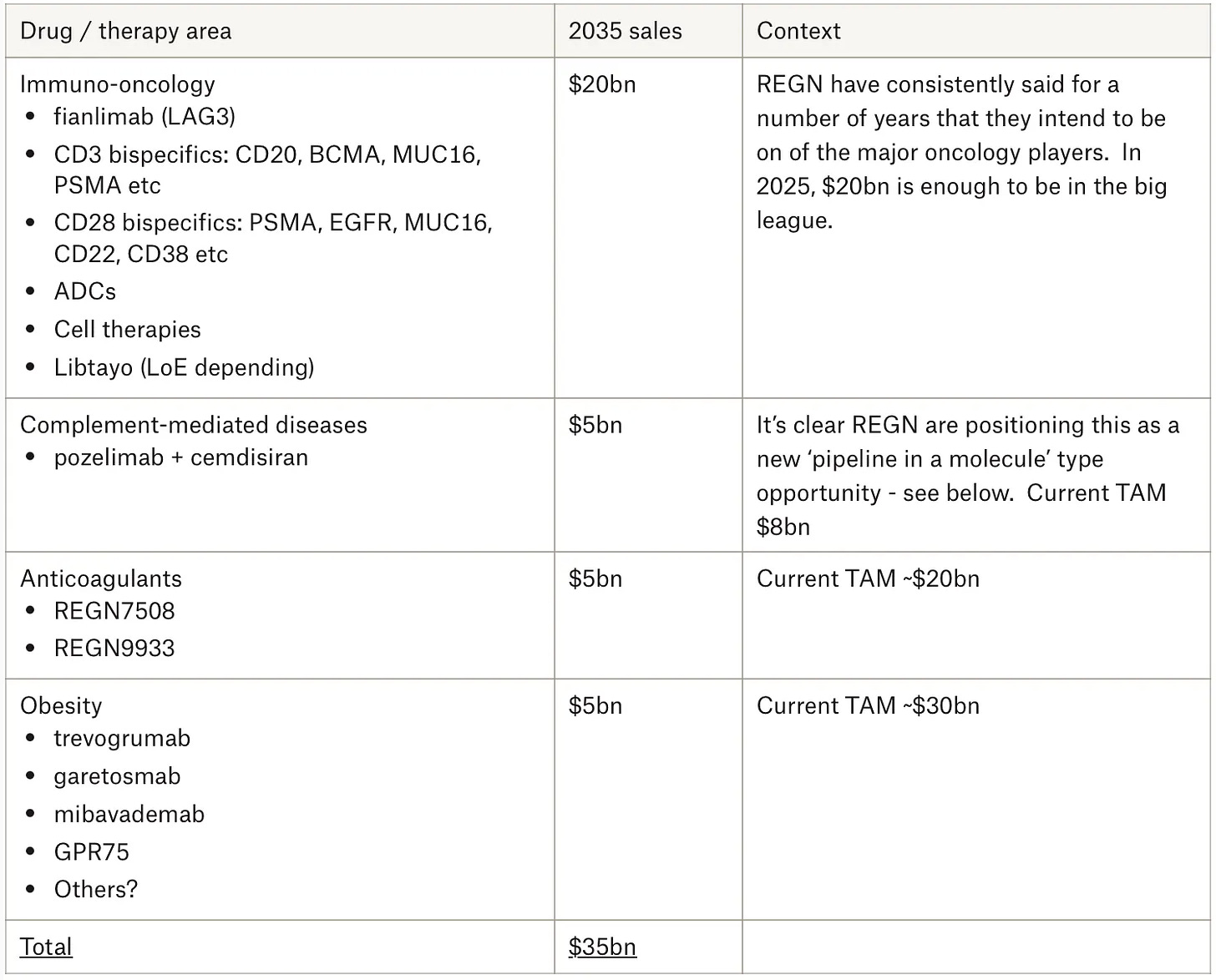

Dream with me for a moment. Let’s imagine the year is 2035 and this is what REGN’s business looks like. It should go without saying that this is not a forecast, so please don’t take it as one - it’s an illustration. Note there’s no Eylea revenue in there, no Dupixent, no additional siRNAs from the Alnylam partnership. I’m leaving a lot out - stuff that most likely shouldn’t be left out and some of which could be sizeable. I’m just following a select few areas that REGN are signalling about and really going after to show that it doesn’t take too much imagination at all to see REGN as a $35bn business in 10 years:

Let’s not quibble over the $35bn. One thing we know for sure is that it’s wrong. I actually suspect it will be higher, although I also note that consensus estimates (the ones that even go that far) put 2035 nearer $19bn. Only time will tell. I think it’s more interesting to ponder some of the ways in which things have developed in the last year. To reiterate, I don’t consider myself an expert in any of these matters, I merely take my cues from what REGN tells us and hints at - as to why that’s an appropriate strategy, I hope I successfully conveyed that in the deep dive.

Areas where I was too enthusiastic, perhaps.

I think the main one here, for me, is the CD28 costimulatory bispecific antibodies. At one stage it seemed as if REGN was going to have a steady flow of these into the pipeline as part of a ‘plug-and-play’ combinatorial approach with CD3 bispecifics and Libtayo - to ‘extend’ and ‘enhance’ the efficacy of immuno-oncology approaches. Their enthusiasm was high and that drove mine as well. For a while the prostate cancer data (PSMA) looked like it could be game-changing for the field. But here’s how Israel Lowy (who’s in charge of developing these assets) put it in November:

One thing that we have is we have a whole co-stimulatory bispecific panel of agents where we’ve been the pioneer. It’s been -- it’s conceptually really elegant -- and we’ve seen different types of efficacy in different settings. In the prostate cancer field, we saw really promising efficacy, but some problematic immune-related adverse events. We are continuing to move forward in that area, looking at combinations with PSMAxCD28, that can widen that therapeutic window and allow us to actually continue to deliver some of the striking responses we’ve had. We have a MUC16xCD28. We have an EGFRxCD28. Those so far have been relatively modest in terms of delivering clear-cut benefit, which I think speaks more to the lack of understanding we have about how to optimally develop this area. But we are pushing forward. And as I said at the beginning, we do this with the idea of having conceptually appealing combinations.

While work clearly continues, the degree to which the CD28s come up now in investors discussions is sharply reduced - something that really stood out to me in 2025. But whether that’s due to reduced expectations internally at REGN, or because of the emerging volume of other interesting things to talk about is unclear (perhaps both).

Areas where I wasn’t dreaming big enough

As 2025 progressed, it’s clear I wasn’t dreaming nearly big enough regarding Lynozyfic (BCMAxCD3 bispecific) for the treatment of multiple myeloma and precursor conditions. It’s now abundantly clear that REGN have huge ambitions here backed up by an array of pivotal trials reading out from 2027 onwards. I won’t re-cover ground I have visited in prior posts, but I recommend the recent Lynozyfic roundtable event if you want to get up to speed on this one. In my mind I had pegged Lynozyfic as perhaps a low-single digit billion peak year sales asset, but it very much feels like REGN has different ideas. I’m getting a similar impression regarding Ordspono as well (CD20xCD3).

So where does that put the $20bn oncology revenue in 2035? Appropriate or wildly ambitious? If I was writing the illustration again today, perhaps I would dial the $20bn down a bit. Again, only time will tell.

Similarly, as 2025 progressed it became increasingly clear that REGN has exceptionally bold ambitions with the FXI anti-coagulant program, as evidenced by another array of pivotal trials enrolling over 30,000 patients in total - it’s a massive investment. These start reading out from 2027 onwards. The scale of it all is starting to suggest that my $5bn figure could be too stingy. You can listen to the recent FXI roundtable for more.

For the avoidance of any doubt here, these are, of course, unproven assets until they have sufficiently succeeded in their various pivotal trials and demonstrated commercial relevance. I would just draw your attention to REGN’s track record in phase III trials relative to currently very modest expectations (e.g. sub-$1bn peak year sales estimates for Lynozyfic).

Areas where, perhaps, I was appropriately enthusiastic

Regeneron’s C5 program (cemdisiran +/- pozelimab) in complement-mediated diseases was amazingly under-followed this time last year, but I felt we had enough signal from REGN, along with later stage progress, to add it as a material contributor in the 2035 illustration. In the end, the phase III results in August 2025 in gMG were particularly impressive and differentiated. There are further readouts coming up this year and next in geographic atrophy and PNH - it’s clear that REGN has big ambitions for another ‘pipeline-in-a-molecule’ type opportunity here and for the time being I feel like my initial enthusiasm was warranted.

I think it’s increasingly clear that REGN intends to have a meaningful obesity business. While last year I went out on a limb somewhat by including obesity in the 2035 illustration (again, merely following management’s direction), a lot has happened since. This includes proof of concept data in muscle preservation strategies, the in-licensing of a promising late-stage GLP-1/GIP agonist and recently announced plans to start studying the latter formulated with Praluent in the same auto-injector (i.e. weight loss and lower cholesterol in one treatment). Insofar as REGN is coming to the table with obesity treatments, the goal is to do something differentiated - to offer some kind of benefit that the other approaches do not rather than to compete on narrow weight loss metrics. I think it’s clear we should expect further developments from here.

Other comments

Another unanticipated (and under-discussed) development last year was the return of focus to REGN’s cat and birch allergy programs, which produced excellent phase III results. Len included both of these in a list of potential blockbusters. Both are going into confirmatory phase III trials with data anticipated in 2027. Were I to produce a new version of the 2035 illustration I would include these as incremental contributors.

Perhaps more importantly, it’s worth noting that the exclusion of Eylea and Dupixent from the 2035 illustration is highly unrealistic. I now believe this to be the case even more so than last year - particularly with regard to Dupixent. Around mid-2025 it started to become clear that REGN had some kind of follow-up brewing for Dupixent (or Dupi 2.0 as I called it). We now know, that REGN has a whole suite of approaches for extending dosing intervals and potentially even improving on the efficacy. These include (among others) an accelerated development program for an IL-13 mAb, and even a ‘Supi-Dupi’ (as they put it) - a naturally selected successor molecule that is potentially even better. I hadn’t foreseen any of this a year ago.

Something else I’d do differently

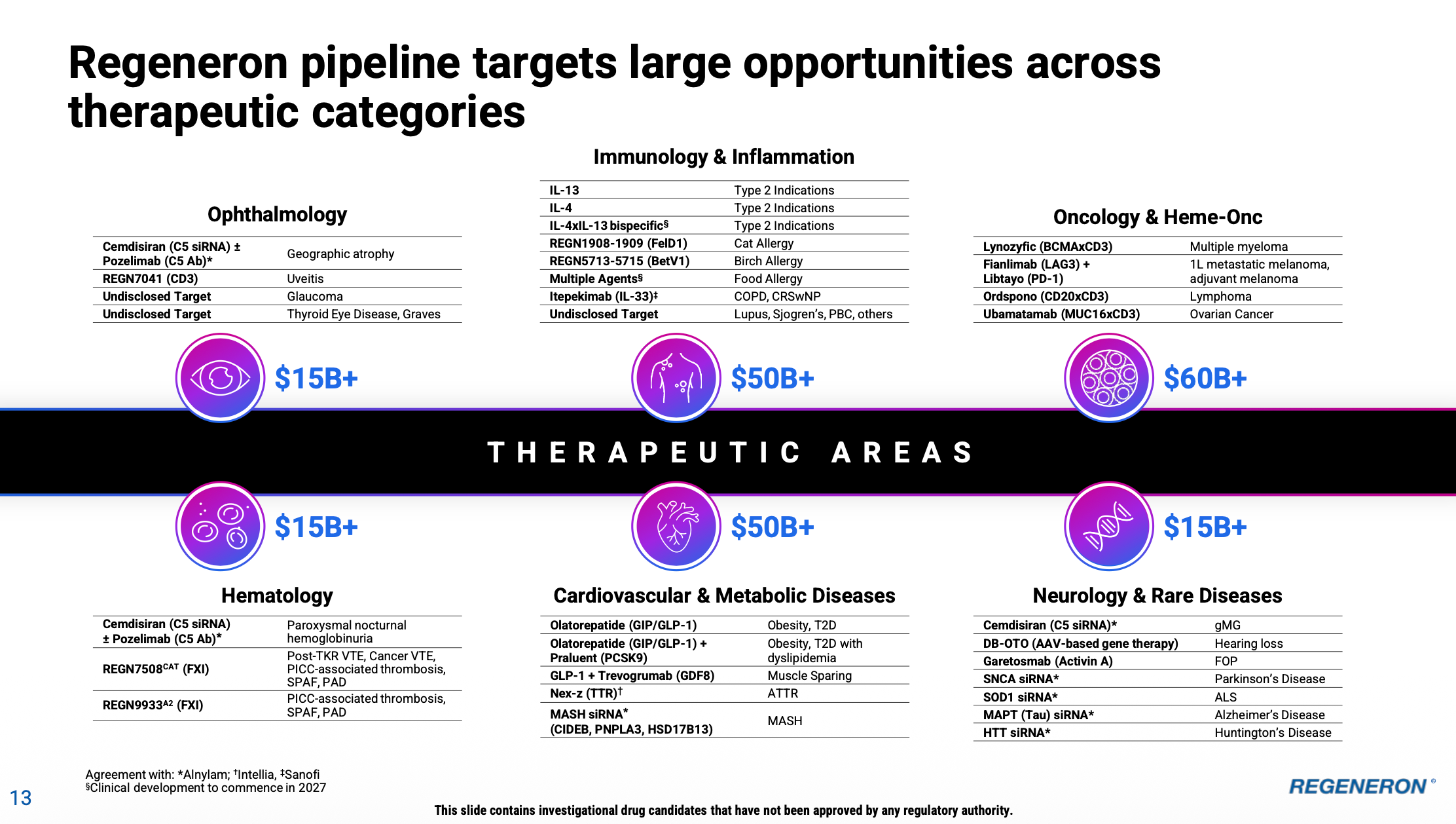

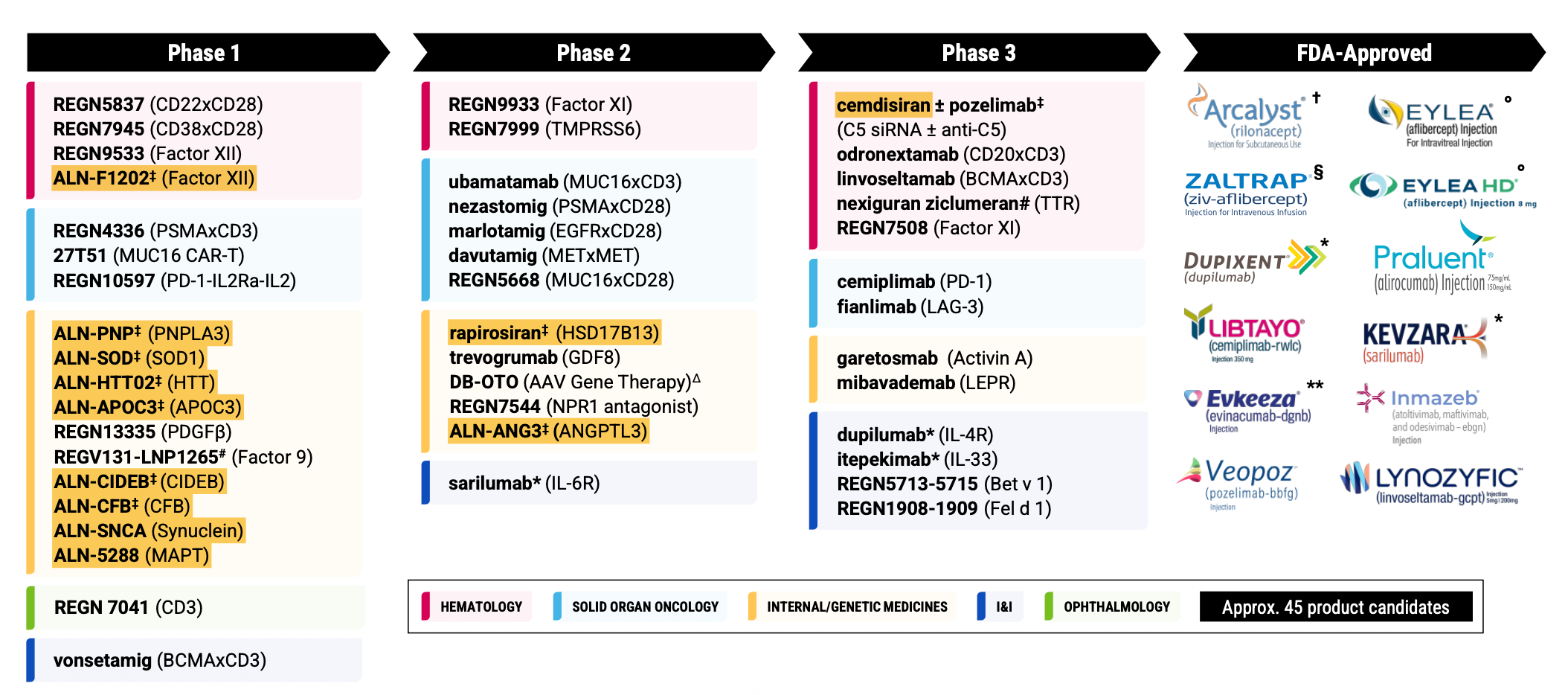

On reflection, I don’t think I made quite enough of the Regeneron-Alnylam partnership in the deep dive. As the months ticked by in 2025, the depth of the partnership became increasingly hard to ignore with a stream of shared assets entering the clinic. I follow Alnylam pretty closely too so I knew this was coming, but most of these programs are still years away from any potential approvals (other than cemdisiran), and therefore perhaps relatively meaningless to most investors. I think this will change as we start to approach the end of the decade - just something to keep in back of mind. Here’s REGN’s pipeline that I showed you one year ago:

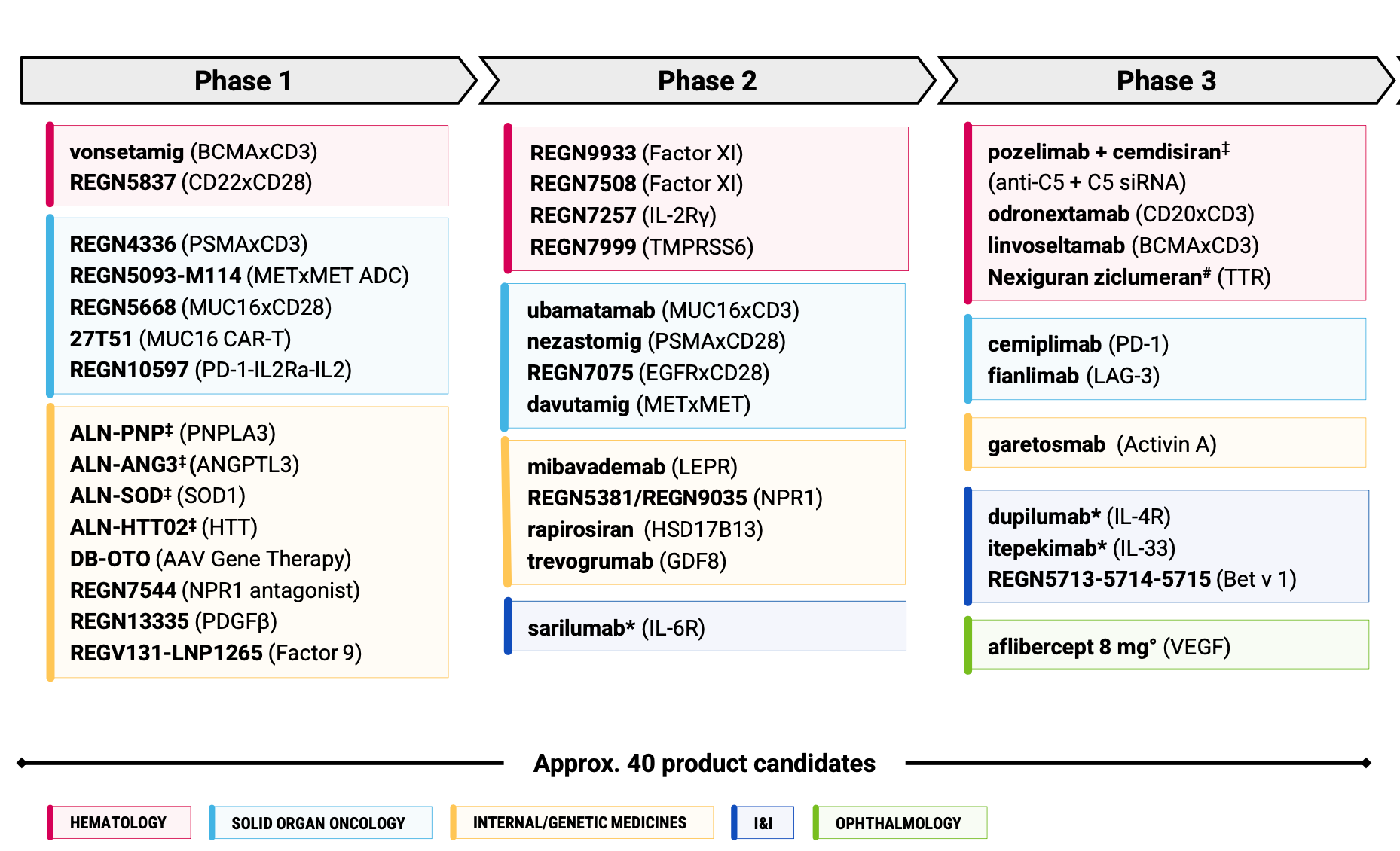

REGN doubled its number of Alnylam-partnered siRNAs in 2025 from 6 to 12. There will likely be more coming in 2026 too.

After Alnylam and Arrowhead, I think REGN is probably the third biggest siRNA player in the world at this stage. And with siRNAs almost at 50% of the phase I pipeline, you’d think they will eventually become a material part of the late-stage pipeline too. Naturally, phase I assets tend to have a high attrition rate on average, just bear this in mind however: one of the few biopharmas with a comparable hit rate to REGN is Alnylam. As far as phase I assets go, I suspect we could see an unusually high percentage of these make it all the way.

Thanks for reading. Time to have a look at the recent earnings and talk about the outlook.