WPP

...Multibagger?

Welcome to the second published stock idea, here at NFTBC. It’s WPP. For more context about this substack, please head over to the NFTBC intro piece. My gratitude to everyone who has read my work so far. If you like what you read, I would be grateful if you share it around. You can also find me on X/Twitter.

[Full disclosure: I have small portfolio holding in WPP and I may dial up or down depending on how things evolve - as posited below. Disclaimer: my work is not intended to be advice - please do your own research].

Thesis

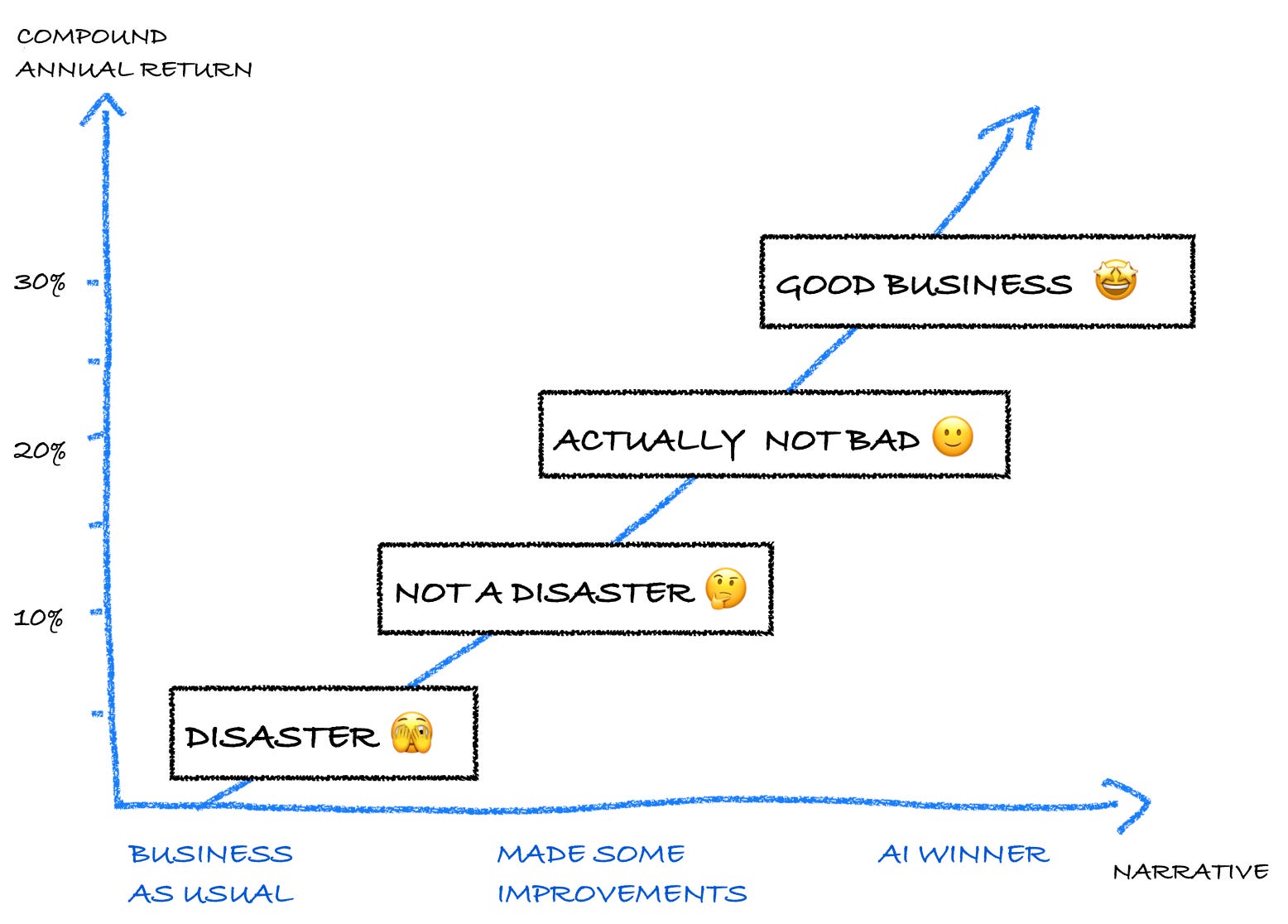

My thesis is conceptually quite simple, yet layered. The simple can be visualised in a graphic, but the layers will require more explanation. Here’s the graphic:

To boil it down, if WPP can prove itself merely to be ‘not a disaster’ then the returns from here should be decent - WPP is perceived to be the laggard in a tough industry, so expectations are very low. I would rate the odds of a narrative upgrade here as highly favourable. But things get more interesting the further we move up the curve. As we shall see, WPP has undergone years of heavy lifting, with the intention of improving its business and competitive position. If management can hit the pretty modest medium-term targets they have set, then the returns get better still. I still like the odds of this - I believe the evidence is mounting, even if not yet present in trailing numbers. Most interesting of all is the topic du jour: AI. As I set out in the NFTBC intro, I am particularly interested in unexpected beneficiaries of the AI revolution. I think WPP could be one of those. While the vast majority of businesses have been behaving reactively to events following the launch of ChatGPT in November 2022, WPP has been pushing on the AI door for years. Of legacy, non-digital native businesses, I haven’t found many that have been more proactive than WPP when it comes to AI, and perhaps genAI in particular. It’s not an exaggeration to say that WPP have put AI at the very centre of their business model.

The combined advertising, media and marketing industries have undergone many shifts over the decades - in the last 20 or so years such shifts have generally worked to the detriment of the legacy players. It’s generally assumed that future trends won’t be positive either. But WPP has been working hard to reassert its value and bargaining power within industry workflows, all within the context of a seismic AI-driven shift currently hitting the world at large. WPP’s management think that the marketing industry is on the verge of disruptive change and they intend to be a disruptor rather than the disrupted. If they get it right, then the revenue model of the industry could change, allowing for greater volumes of business and at higher margins. This part is less certain - it’s interesting and exciting but no one really know how things will unfold even if WPP’s ambitions are clear and its strategy coherent. I will be watching and updating as things progress.

Why WPP now? I think the inflection draws near. WPP has faced headwinds in the last couple of years and the share price implies these will be ongoing. Per CEO Mark Read, 2025 will be the “year of execution”. From the various signals we’ve had the business is about to start growing again, even if just moderately to begin with. We should therefore be able to build confidence this year as to whether we are taking the first step up the curve - perhaps we’ll learn more at WPP’s earnings event next week. To be clear, giant strides up the curve seem unlikely. If we do keep heading up the curve, it will be multi-year story - hence the provocative subtitle. As an illustration: 25% compound annual return for five years gets you into multibagger territory.

Industry Background

Most readers will likely know that WPP is one of the four major ‘holding companies’ operating in the wider advertising, marketing and media industries. The other three being Publicis, Omnicom and Interpublic - soon there will be just be three when the latter two merge.

Disruption is by no means new to the industry. To begin with, one can readily identify a number of major shifts in the locus of advertising space over the last century:

Yet the industry has adapted. For example, only relatively recently has WPP begun to merge some of its iconic older brands that have existed continuously throughout this period. This includes J Walter Thompson (founded 1896) and Young & Rubicam (founded 1926). Even today, Ogilvy (founded 1850/1948) remains a core brand that will remain distinct within WPP, as does Grey (founded 1917) although as a sub-brand of AKQA. It's a similar story at the other holding companies. The industry, has in the past, operated quite different models too - with different incentives and economics. In the years when David Ogilvy cooked up his legendary series of Man in the Hathaway Shirt ads (see picture at top), agencies were ‘full service’ and ran on commission, typically 15%. The agencies would buy up the media space and re-sell it to clients with commission and bundled creative services. The incentive therefore was to sell more media space, which was more likely to happen if the agency made good ads - agency gets paid well and client is happy. Moreover, the creative and media functions would operate hand-in-hand.

As it happens David Ogilvy is typically credited with introducing the ‘billable hours’ system (input-based pricing) to the industry in the 1960s, although it didn’t really get going until the 1980s by which time the holding company industry structure had emerged. In the early 1990s the agencies began to ‘unbundle’ creative and media functions - the reasons are various, whether it’s the rise of specialist and media boutiques (potential acquirers), a changing media landscape and then ultimately the rise of the internet. The result was a decisive shift from billings-based compensation (commission) to fee-based compensation, notably billable hours although various other forms exist.

With the rise of billable hours, a secondary consequence has been more work for less compensation. And a tertiary consequence has been higher client churn - clients typically now put their accounts up for competitive bids every few years, forcing the agencies to compete on pricing. In the past, it was pretty common for clients to stick with their agency for many years, so long as the work was good. It’s a well known problem in the industry and insiders are constantly looking for ways out. Perhaps no one talks about this more than Michael Farmer (check out his substack):

The holding companies ultimately ended up reacquiring the majority of the media business, but the creative and media functions have largely remained separate rather than reintegrated.

Another element of the industry backdrop is the emergence of new competitors from outside the industry. One is the encroachment of consultants onto the agencies’ turf. The other (and larger) is the shift from traditional media to digital. For example, global ad spend has more than doubled in the last decade - but the vast majority of this value has been captured by Alphabet and Meta in particular. Organic growth at the holding companies has been significantly below-market. Part of the reason has been the growth in digital advertising by SMEs who tend not to engage large global agencies, but it also pertains to consultants, compensation structure and some lack of self-help frankly. Nevertheless, the holding companies remain very much an essential element of the global marketing ecosystem - they have not been disintermediated. The holding companies have also remained quite profitable, albeit through cost-cutting and working employees hard, rather than through operating leverage.

WPP - History and Transformation

WPP’s story begins in 1985, involving shopping baskets, a BMW, fish and chips and a 40 year old Martin Sorrell - the specifics aren’t important, but the curious can read about them here. Sorrell then went on a 33-year shopping spree, acquiring hundreds of businesses - he’s surely one of the most acquisitive leaders in business history. In 2018 he was ultimately deposed, in ignominious circumstances. What Sorrell left behind was a mess. Yes, some great iconic brands and capabilities, the word’s largest media agency and thousands of talented people, but a mess. There were hundreds of brands, thousands of legal entities, hundreds of office locations, dozens of IT systems and practically no integration. Moreover, through running the business too hard for margin, Sorrell had underinvested in WPP’s largest market (the US) and underinvested in employees. Multinationals were also squeezing marketing budgets due to a passing fad in zero-based budgeting. The business was indebted too. When WPP’s share price was riding high in 2017, its business was already on the turn - margins were diving and revenue growth had stopped.

This is what current CEO Mark Read inherited and thus far he has pretty much delivered on what he promised in late 2018. Most notably:

Simpler business (fewer, more integrated companies)

Common technology

More integrated solutions for clients

More investment in employee compensation

By early 2024, this shows how far WPP had progressed:

Read has retired ~300 brands, eliminated 1400 legal entities, switched off 70 ERP instances and closed 840 office locations. The majority of employees now work together in campuses, versus practically none in 2018. He has disposed of >90 businesses and reduced debt. The restructuring cash outlays to make all of this happen have been significant, but the result is a more efficient and better integrated business. And despite heavy investments in staff costs and technology (more later), operating margins are now settling into an upwards trend. Additionally, with restructuring increasingly in the rear-view mirror, cash conversion is set to improve markedly from this year and beyond.

To give a little more colour on WPP’s business:

Global Integrated Agencies

GroupM: WPP’s media business - the world’s largest. GroupM provides media planning, buying (>$60bn annual billings), performance measurement services and data products helping businesses decide where and when to advertise, ensuring their ads reach the right audience through TV, online platforms, and other channels. ~40,000 people. Growing mid-single digits and ~40% of net sales.

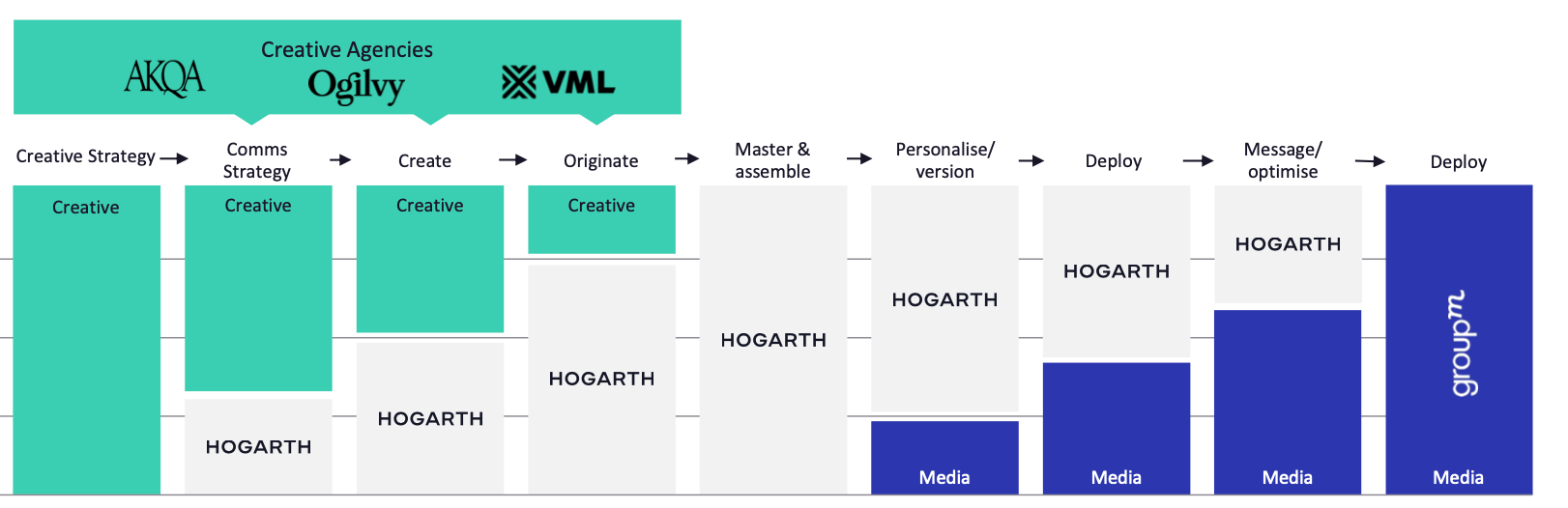

Creative Agencies: Ogilvy, VML and AKQA - it’s not just advertising but includes a spectrum of creative capabilities such as marketing, experience and design, social, consulting, projects etc. ~50,000 people. Growing low-single digit and ~40% of net sales.

Production: Hogarth, the world’s biggest marketing production company - putting creative ideas into production. ~6,500 people. Growing high-single / low-double digits and ~5% of net sales.

PR & Specialist Agencies - roughly 15% of net sales. I’m going to largely gloss over this part of WPP as I consider it non-core, as does WPP as demonstrated by the recent sale of FGS (strategic communications) to KKR.

Putting it all together, WPP has moved from operating in silos towards globally integrated, end-to-end marketing solutions for clients. A much simpler, and in theory, more effective proposition.

But is it working?

‘Not A Disaster’ - Coca-Cola

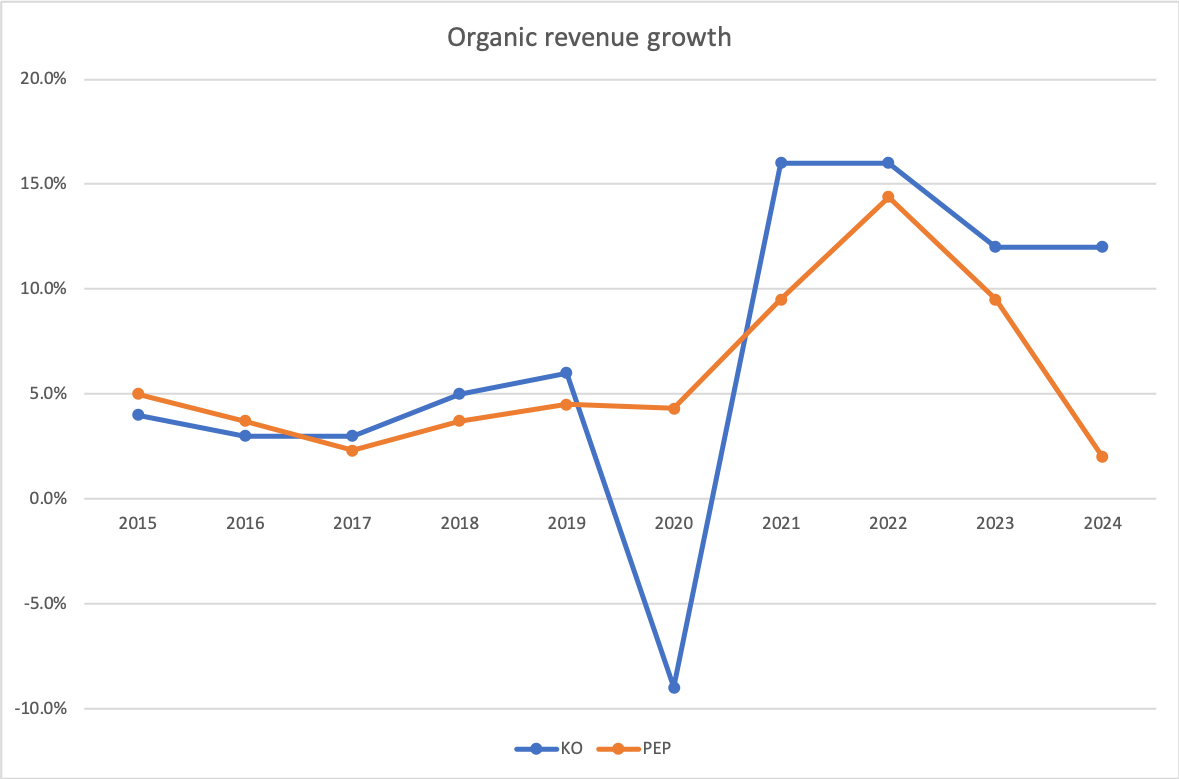

Relative to its peers, Coca-Cola (KO) has been on a tremendous streak in the last several years:

KO and Pepsi used to grow at similar rates, then we had the disruption from the pandemic and spillover into inflation. But in the last several years, KO has really entered its stride, while peers struggle to get the balance between price/mix and volumes right. Pepsi is not alone here. So what has gone so right at KO? If you listen to KO’s management, they very consistently talk about their global marketing transformation that began in late 2021 as one of the central drivers of their recent success.

Here’s CEO James Quincey speaking at CAGNY this February:

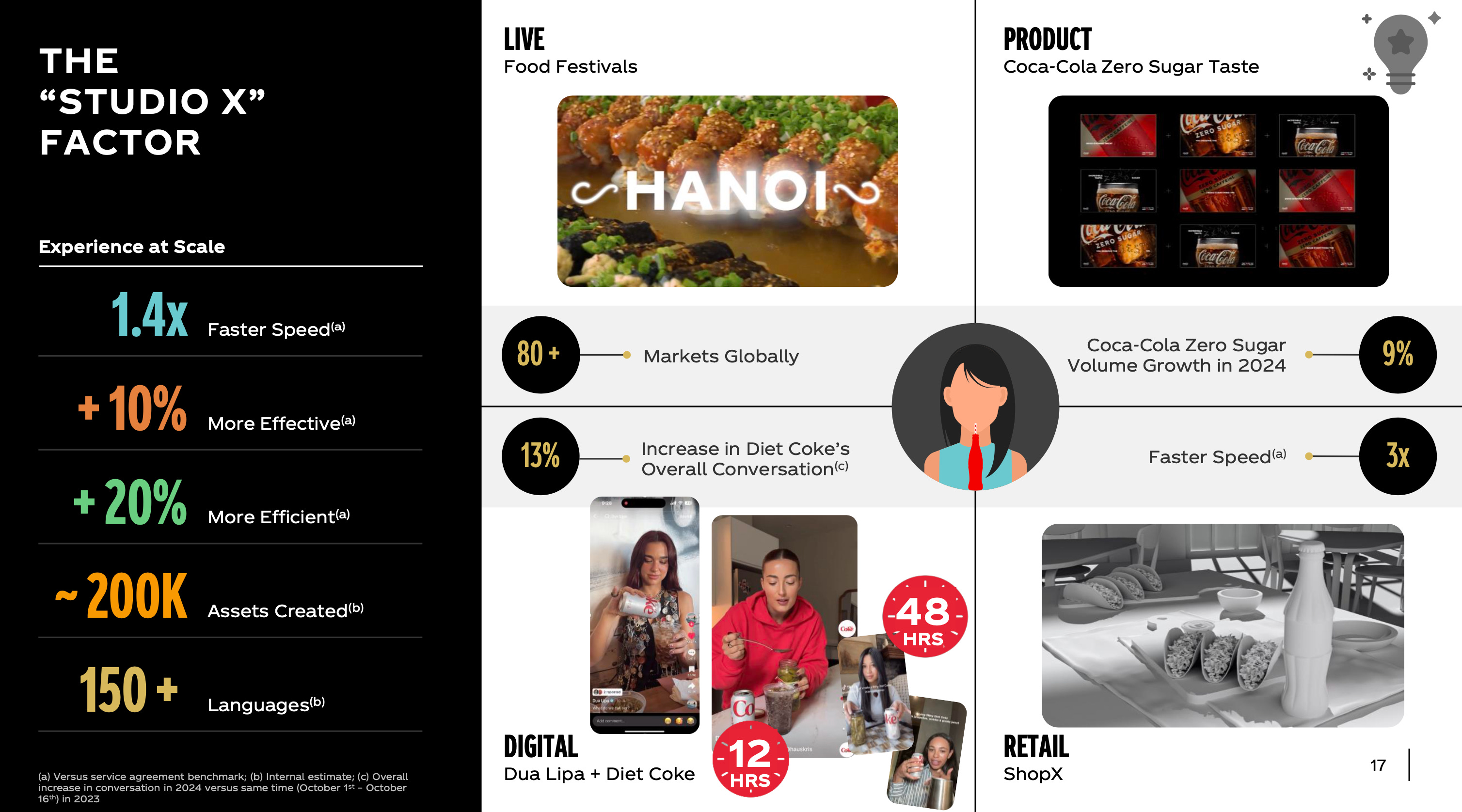

We've talked about Studio X a number of times before, but it's really been a key component in helping unlock our marketing transformation. In essence, there are nine studios around the world all interconnected, and nine, because we have nine operating units that of course are increasingly using the digital ecosystem around them to deliver experiences as they drive growth. There are not many things you can come on to the stage and talk about where you get all of the first three things on the left hand side [note: see slides below]. It has made our marketing faster from idea inception to execution. It has made it more effective with consumers and it is more efficient, i.e., cheaper. Not many things can deliver on all those three and actually come to life at scale.

And so it's been a huge help to unlock the obvious speed, effectiveness and productivity… So really the Studio X, the implementation of this both through the things that we do, the things that we connect into and can amplify, has really allowed us to go on the marketing transformation journey. And as we talked earlier or last week in the earnings call, we're starting to see some of those productivity benefits come through, not just by driving the top line, but some of those in the back half of the year into the P&L as well.

What is StudioX I hear you ask? It’s the creative execution arm of WPP OpenX, a bespoke global agency that WPP set up when it won the KO brief in late 2021. The brief being, to transform KO’s marketing and be a catalyst for growth. OpenX has more than 5,000 people working across WPP’s agencies across 200 brands and territories. It brings together all capabilities from creative, through production and to media. Importantly, it’s not a walled garden - OpenX can and does draw on the capabilities of external agencies when necessary. It’s abundantly clear that it’s been transformational for KO and a core element of their success - to the extent that WPP frequently gets named dropped at investor events and conference calls . I think we can reasonably draw at least two conclusion from this: 1) OpenX is now integral to KO, and KO is unlikely to put this account up for competitive bid and 2) it’s highly unlikely that KO’s success is going unnoticed by other prospective clients.

the easiest way to get new clients is to do good advertising

-David Ogilvy

One of principal reasons for WPP’s sluggish revenue performance in 2024 has been the loss of a couple of big client accounts (notably Pfizer) at a time when new business wins have not yet fed through to revenue in sufficient offsetting quantity. The first layer of my thesis therefore, is that this dynamic is not terminal. As we shall see, margins have bottomed and are now increasing, while the example of KO demonstrates that WPP’s simplification is working. In other words, WPP is not a disaster.

WPP Open - ‘Actually Not Bad’

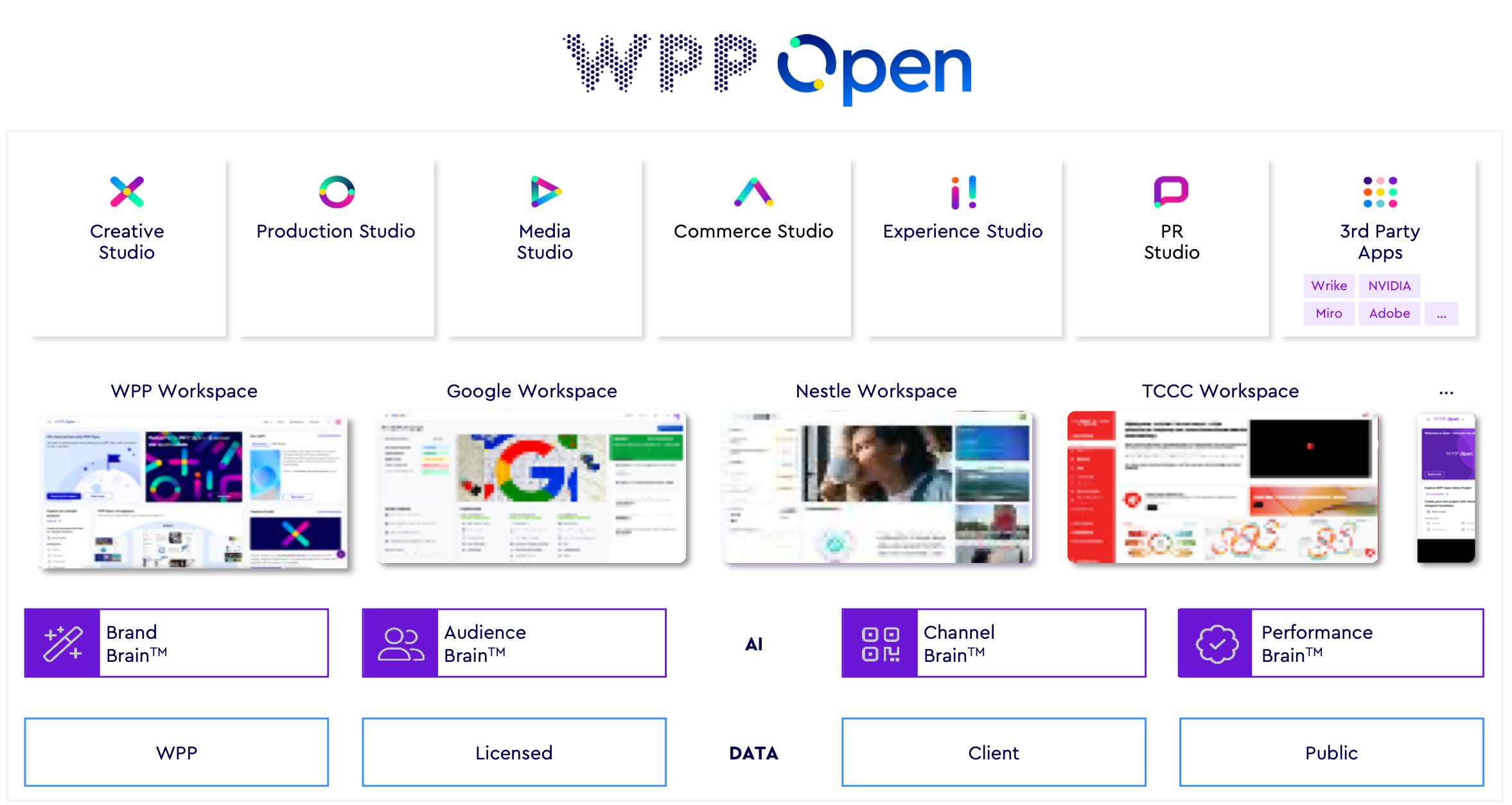

We now arrive at one of the most important elements of this thesis. WPP has built a single ‘marketing operating system’ software stack that powers all of WPP’s businesses - it’s called ‘WPP Open’ (not to be confused with OpenX). Moreover WPP Open is customisable and available for use by clients as well, effectively as their own ‘white label’ workspace. Open is comprised of core ‘Studios’ - Creative, Production, Media, Experience, Commerce and PR, designed to support the end-to-end workflows of WPP and its clients in a way that allows for integrated ways of working across the company and its functions.

From what I understand, Open runs on Google Cloud. Third-party apps are embedded into Open too, via APIs. AI functionality is central to the entire proposition - whether it’s through natural language queries, content generation, optimisation algorithms as well as WPP’s proprietary ‘Brains’ (see later). WPP has 3,500 people working on Open’s development and has invested hundreds of millions so far. We discussed earlier a key part of Mark Read’s strategy has been breaking down silos and reintegrating the business - per CTO Stephan Pretorius:

The biggest shift is that we’re no longer thinking in silos. Creative, strategy and media used to be distinct functions. Now they’re all converging within a single AI-driven system.

Here’s a nice video overview of Open. And here’s a video overview of one of the Studios (Production).

My impression is that the strategy with Open is working, even if it hasn’t yet fed through into the financials. At Q3 2024, WPP told us that monthly active users were up 107% from the start of the year (at which point they quoted 28,000 users) - so presumably Open finished the year with users well into the tens of thousands. And it’s not just WPP staff. Per WPP key clients using Open include Google, IBM, L'Oréal, LVMH, Nestlé and, of course, Coca-Cola. WPP also returned to winning big accounts on a net basis in 2024 - with Open driving new assignments, perhaps most notably with Amazon. These accounts start adding to revenue in 2025. And for some third-party validation, Forrester thinks that WPP might be displacing some of the consultants now with Open specifically rated for “joining capability dots”.

We’ll have to see how WPP’s 2024 results pan out next week and what 2025 guidance looks like, but I’m cautiously optimistic we’ll see the narrative start to improve to: ‘WPP is actually not bad’

There will be several things I’m going to be looking out for: 1) will Open continue to drive client wins in 2025? 2) What will Open do for client retention, given that it’s a software stack that embeds in clients’ workflows? Will clients want to stop using Open? Will they be able to? 3) I heard Daniel Hulme (WPP’s Chief AI Officer) say on a podcast that they’re going to launch a version of Open for SMEs to use - while I haven’t seen any announcements, it does seem like a pretty interesting growth opportunity previously unavailable.

Artificial Intelligence - ‘Good Business’..?

It will mean that 95% of what marketers use agencies, strategists, and creative professionals for today will easily, nearly instantly and at almost no cost be handled by the AI — and the AI will likely be able to test the creative against real or synthetic customer focus groups for predicting results and optimizing. Again, all free, instant, and nearly perfect. Images, videos, campaign ideas? No problem.

Sam Altman, OpenAI CEO, talking about AI

If we solve end-to-end marketing, the only differentiator for a brand is human creativity.

Daniel Hulme, WPP

If you take away the technology, it still has to be a good idea.

someone at WPP

In a narrowly defined sense, WPP has been working with AI for over a decade already - for example in programmatic advertising within GroupM where automation and optimisation algorithms are used for transacting in ad space. But it was in 2021 that WPP’s ambitions really stepped up several gears, with the acquisition of Satalia. In 2021 Satalia was a technology consultancy, building AI-based solutions to address clients’ problems. The company was founded by Daniel Hulme, a scholar and entrepreneur in the field of AI. Following the acquisition Hulme became WPP’s Chief AI Officer while Satalia essentially became WPP’s internal AI R&D lab, while also continuing to act as a consultancy. Satalia has grown from ~80 people in 2021 to around 300 today. As you know, I’m interested in how businesses are actually deploying AI in the real world - I’ve looked at quite a few. In my mind, there’s little question that WPP is in the top decile, in terms of capability and how far it has gone. When you look around the roster of ‘chief AI officers’ that are becoming increasingly common, vanishingly few are genuine experts with a deep understanding of the leading-edge research - Daniel Hulme is. And WPP is investing heavily - investments in proprietary technology to support the AI and WPP Open strategies currently amount to £250m a year, with plans to spend an incremental £50-100m in 2025. At these levels we’re talking about 2-3% of net sales going into R&D, which is something new altogether for the traditional marketing industry.

Hulme’s (and Satalia’s) expertise are in applying the right AI solutions to the right problems, and they’re doing this across the whole company. Some problems are best addressed through simple automation, some through optimisation, others through machine learning and others through generative AI. As you can imagine, they’ve built a lot of automation into WPP Open in order to make workflows more efficient, while users also have access to the best LLMs (across providers). But one area where WPP has really set itself apart is through the creation of proprietary ‘brains’ Per CTO Stephan Pretorius:

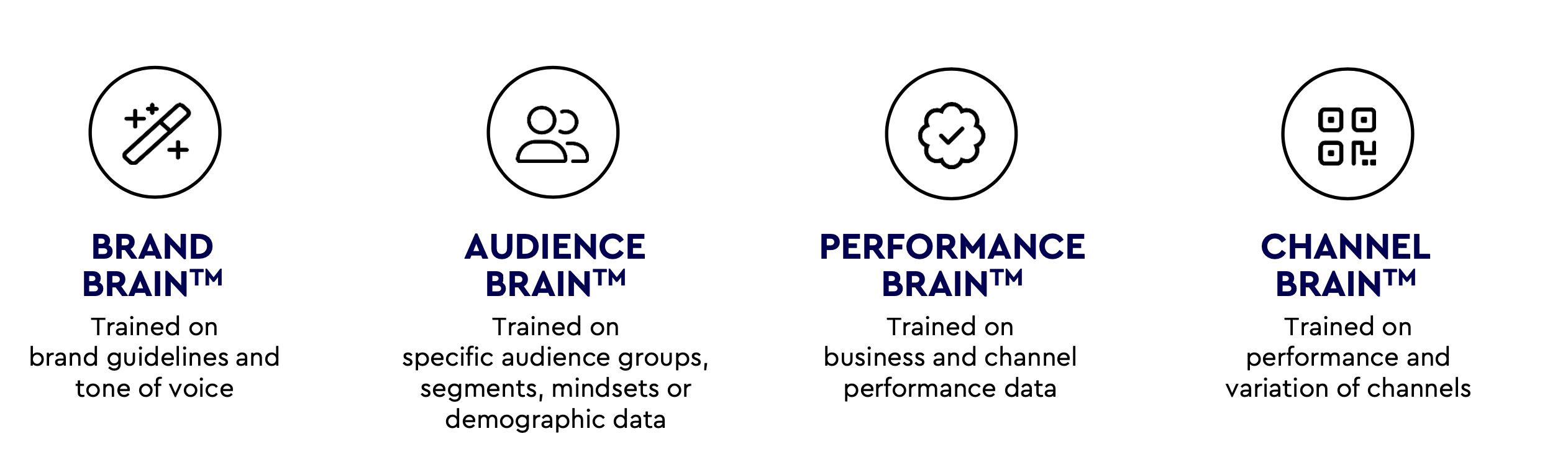

We sat down together and understood that marketing is effectively a four- part algorithm. You're connecting consumers to brands through content and channels. And so by encoding those four concepts into custom AI agents or Brains as we call them, we are now able to bring the power of AI to the entire marketing supply chain in a very structured way.

There are four categories of brain:

Brand Brains are bespoke models trained on individual brands’ tone of voice and brand elements to help produce “brand-specific, accurate, differentiated content”. Whereas widely available genAI models create generalised outputs, WPP can create highly contextualised outputs, and therein lies the difference. Similarly, Audience Brain is trained using genAI models with broad and varied data from both WPP and clients - it can be used to validate brand audiences already known to exist but also to find new audiences. Audience Brain can be asked what kind of advertising it wants to see and can then be used to create prompts for Brand Brain. Performance Brain on the other hand is trained with machine learning using data from Audience Brain as well as WPP’s existing performance data - enabling WPP to much more accurately predict activation of clicks, likes and sales etc, including the changes you need to make to create an uplift. Lastly there’s Channel Brain, which uses optimisation algorithms to deploy content into the right channel:

We have to push thousands of pieces of content across thousands of channels every second of every day. And so utilizing the bleeding-edge technologies from academia to be able to make these decisions is really what differentiates our business, particularly when it comes to media planning and buying.

I included a Sam Altman quote above - it’s been widely circulated and more or less sums up the bear case for WPP and for the industry in general. Notably, WPP has basically already achieved what he was outlining - although certainly none of this is cost-free, even if the cost of delivering the technologies is decreasing (to WPP’s benefit). But is it enough? Or does it mean that agencies are basically redundant now? Let’s pause and take stock for a moment.

What I like about WPP’s approach is you have: 1) a CEO who grasped the nature of the sea change underway, and early on tasked his CTO and CAIO with making WPP a disruptor. 2) Leaders who then set about assembling the right team to make it happen. 3) A company with unique data relevant to the task at hand (>9bn campaign records, data from 29,000 brands, details on >200k products etc) and, in WPP Open, a platform from which to bring client data into the fold. And then the crown jewel, that no competitor from outside the industry is able to replicate, is WPP’s creative talent.

In Altman’s worldview as a techno-maximalist, there’s little need for human involvement in the marketing process. Leaving aside questions of whether one would even want to live in such a world, we should ask: is he even right? Can marketing be fully automated from end-to-end? The answer seems clear: yes. But will it be good marketing? On this, I’m not persuaded at all. AI technologies work statistically, and through interpolation or extrapolation - generally based on things that have happened before. The human imagination works in fundamentally very different ways - in ways that cannot currently be replicated by AI. I don’t intend to have a debate about it here (happy to do so elsewhere), but we’re worlds away from an AI being able to dream up a man in an eye patch to sell shirts - only a deeply imaginative and eccentric mind with a talent for marketing can come up with such a thing. I would argue that with the proliferation of genAI, human creativity has never been more important for any brand wanting to stand out.

Indeed WPP is doubling-down on creativity while simultaneously building its technologies - the two are fully intended to work synergistically. By combing creativity with AI, WPP believe they will be able to produce higher volumes of work, with higher effectiveness and at lower cost. Using the technologies, creatives can iterate faster, prototype ideas and get to production faster and cheaper.

[A brief side note on the Cannes Lions (the ad industry’s version of the Oscars). Last year WPP won Creative Company of the year, as it has in three of the last four years. Also Ogilvy won Creative Network of the year (two years out of four) and Coca-Cola won Creative Brand of the year for the first time ever. While Lions don’t convert into profits, they signal that WPP is at the top of the creative game, if nothing else.]

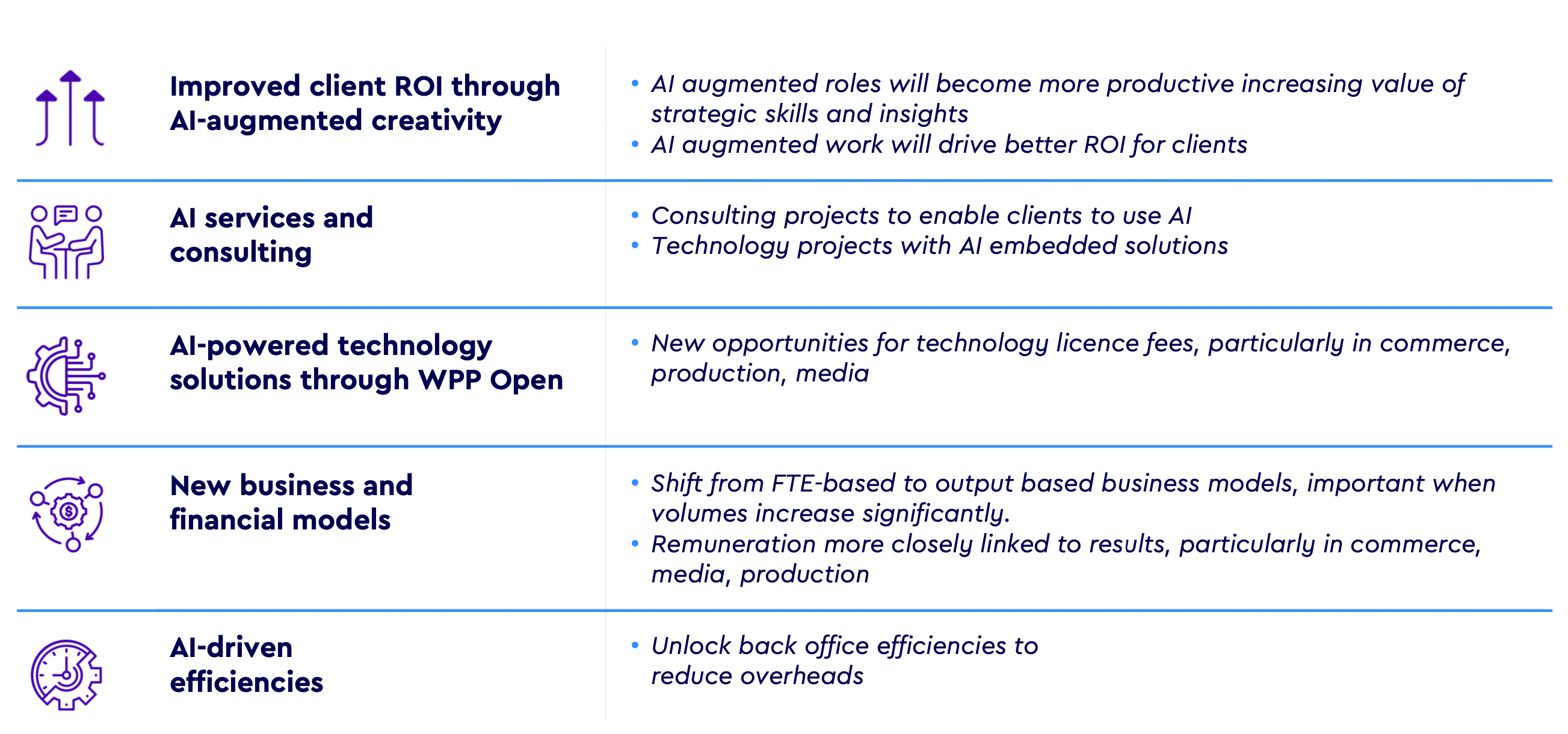

It’s too early to know how things are going to evolve for WPP, but WPP believe that the possibilities brought by AI-assisted content generation and placement, at lower marginal cost, will likely result in greater demand (dare I say it: Jevons Paradox). The natural question would then be whether WPP would be able to hold onto this higher economic value - I would argue, probably yes. We’re possibly coming to an inflection point where for all the reasons I have mentioned WPP’s structural position is improving for both churn and win-rate, resulting in less competitive pressure. We’ve also seen there are possible opportunities to expand further into selling to SMEs. And I haven’t touched on evolving pricing models yet - I’ll come to that below.

The Other Holding Companies

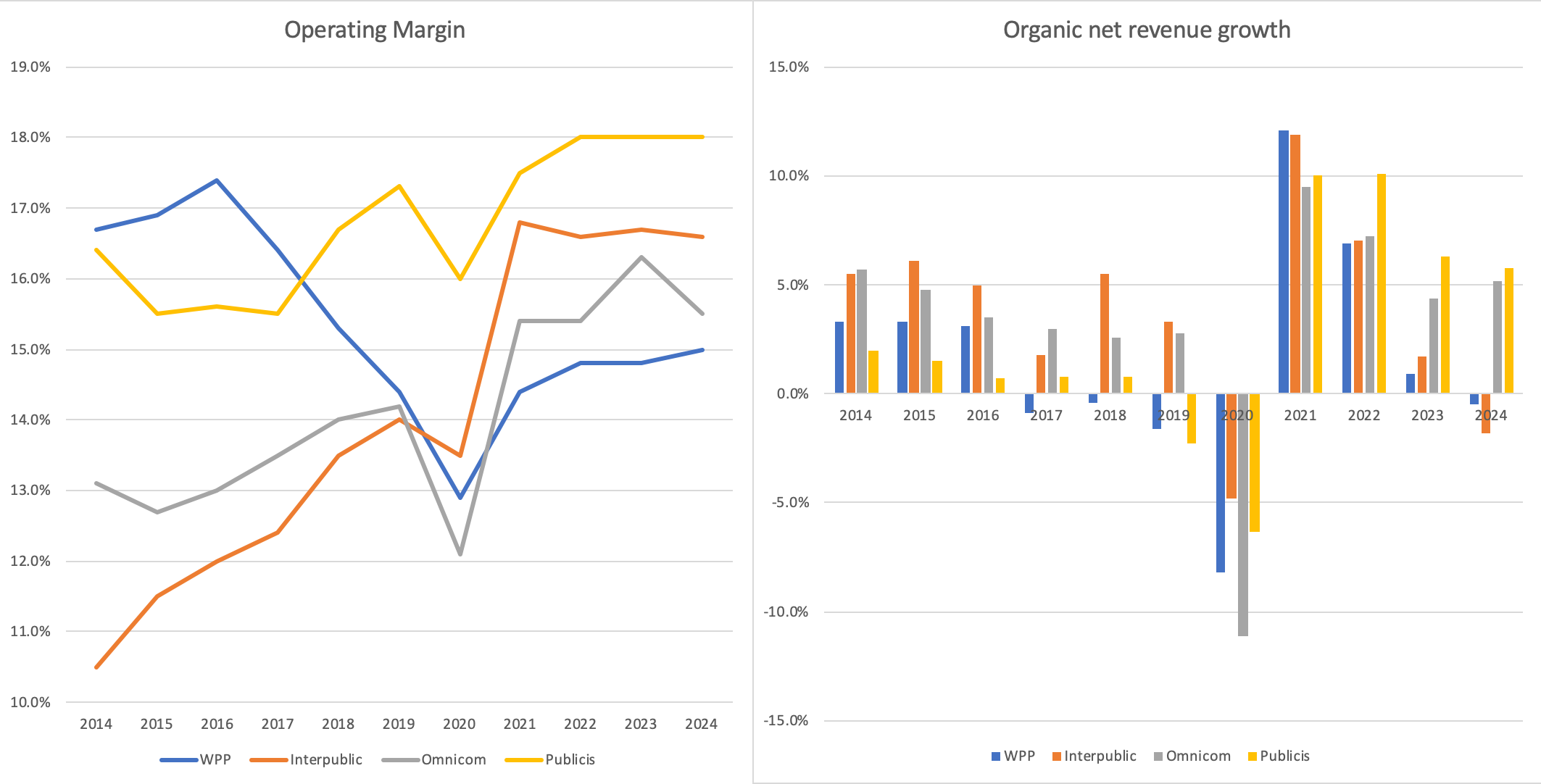

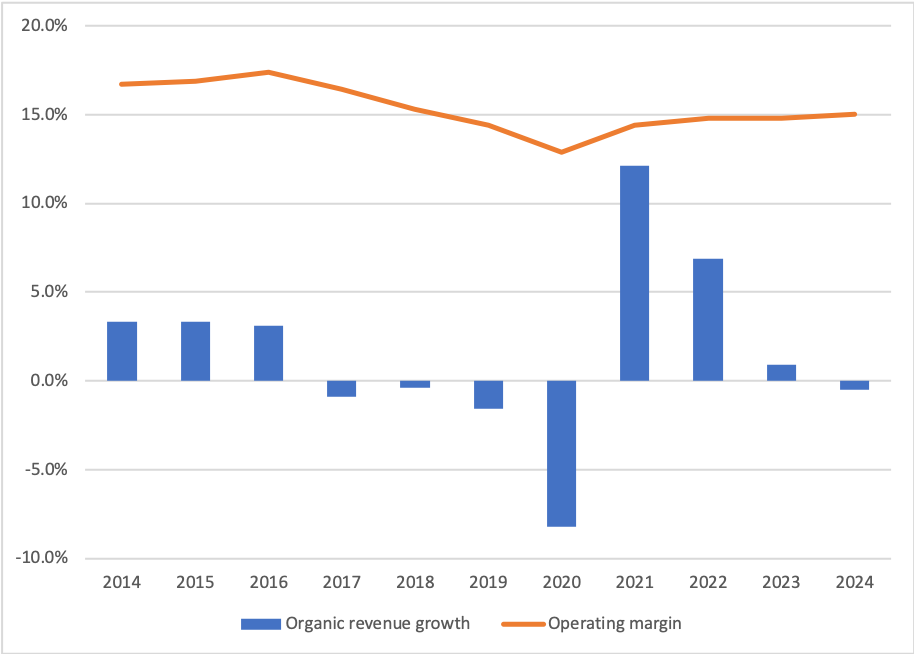

For context, it’s worth having a quick look at WPP’s holding company peers. Here are operating margins and organic revenue growth over the last decade:

Each company paints a different picture. Like WPP (and now Interpublic), Publicis (PUB) was once struggling for growth and has now emerged on the other side, having made some key acquisitions in data as well as some reorganisation. PUB has a sound strategy that is working - shareholders have been rewarded in the last few years, even if the stock remains at undemanding levels. It’s worth considering.

You can see WPP’s margins peak shortly before Sorrell’s departure, as well as slowing growth. Obviously the pandemic, 2023 client losses and cyclicality (especially in the technology sector) add some noise. In totality WPP has the lowest margins and among the lowest growth, so it’s no wonder that the stock is unpopular.

For their part, it looks like Omnicom (OMC) and Interpublic (IPG) are going to merge (pending any possible regulatory impediments) and this muddies the picture somewhat. They’ve announced significant synergies that will come through cost cutting and it’s basically a given that there’s a long and arduous integration path that lies ahead. From an investment standpoint, this makes the stocks unattractive, for me, until we can get some greater clarity on the direction of travel - which could be years away. Using WPP as the example, its transformation has taken years and only fairly recently has it become investable in my view. But needless to say, the consolidation down to three holding companies is a very positive development for the industry as it certainly means reduced competition for client accounts. And, as noted, for OMC and IPG it likely means a period of integration and client disruption stretching into years - creating opportunities for WPP and PUB.

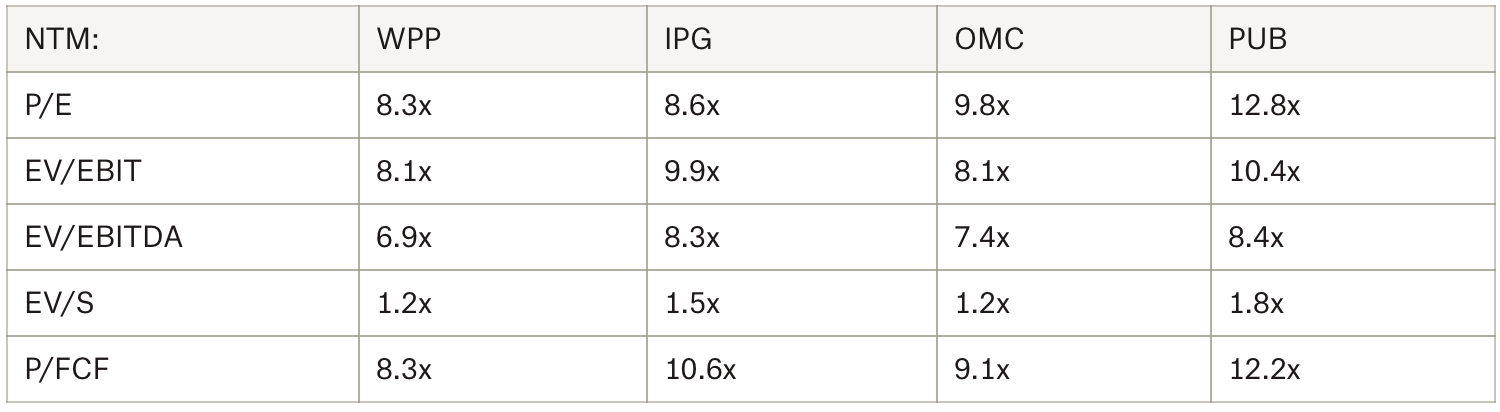

Even in a depressed sector, WPP has the lowest valuation on all fronts. But it also has the best visible prospects for margin and growth improvement. This is a potent combination in my view. Moreover, the sector itself is consolidating. If we also arrive at a situation where at least two thirds of the holding companies (PUB and WPP) are executing well, it would not then be a surprise to see the industry as a whole re-rate higher.

Before we move on, a quick note on technology and AI. I have already outlined the scale of WPP’s investments into AI, which compares to $80m for IPG in 2024 and €300 for PUB over three years. OMC have not provided a figure, so far as I can ascertain. With IPG and PUB investing <1% and sales and WPP investing 2-3%, it becomes easier to see that WPP’s lower margin does not tell the entire story. Last, it’s worth noting that OMC, IPG and PUB have ‘platforms’ too, but they’re more focussed on the data and consumer insights side of things, rather than a complete marketing ‘operating system’ like WPP Open, which is a unique proposition.

The future - economic models, growth and margins

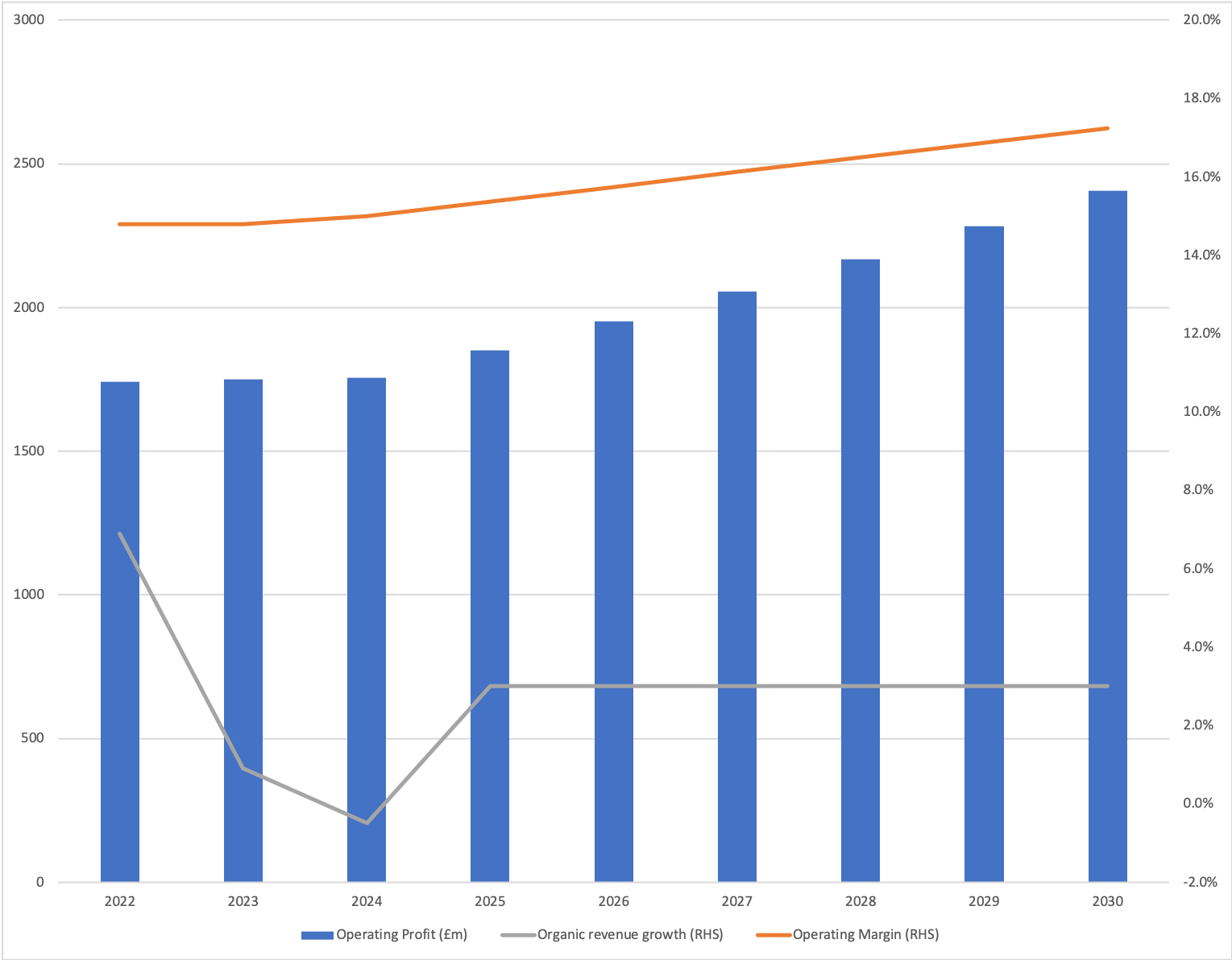

Let’s revisit the above chart, but without the noise from the other holding companies:

The question is: where next? Let’s start with what WPP’s management have said. At the beginning of 2024 they set out a “medium-term” financial framework of: 1) 3%+ organic revenue growth, 2) 16-17% operating margin and 3) potential for M&A to add up to 1% p.a. to growth. They also provided that they think of medium-term as three to five years. Additionally note that the framework was given in the context of the 2024 guide which was essentially flat revenue plus 20-40bps of margin growth.

Hitting the margin mid-point in year five (2028), as well as the baseline growth commitment, would look something like this:

And it’s a very different picture to the WPP of the last 5-10 years - we’re looking at ~5.5% annual EBIT growth compared to a business that has essentially gone nowhere in 10 years. I’ve also assumed they keep going. I can’t see consensus numbers that far out, but I’m pretty sure I’m significantly ahead. Is this reasonable? I think so. Here’s what Mark Read said at the capital markets day in January 2024:

Last and by no means least let me talk briefly on our financial commitments. So this is our medium-term financial framework and the financial commitments that Joanne will take you through later. As I said, I know we've had our challenges on the top line in 2023, but what we can control directly are margin commitments and our working capital, we've over-delivered on our guidance. We want to accelerate our growth to 3%-plus organically. We think this is our commitment to you.

And in the Q&A:

3% plus is what we think of as our commitment to. That's what we need to deliver. And I think we'd like to do better. I mean, emotionally, rationally, I sit in this presentation like you said this presentation, it should be 5%, or more. So I think that, you know, we see a good opportunity ahead of us. But I think at this point, what we want to say is 3% plus.

And here’s what he said in Semafor just this month:

After “quite a painful process… we’ve taken a lot of the hard decisions” that should start paying off in 2025.

And here he is speaking to the FT last month:

As a leadership team, we have a plan. We know what to do. And 2025 is the year about execution, and particularly execution in AI.

We’re very confident where we are with our investments in AI, and I think we’re going to see a better year in 2025 than we did in 2024.

Now they haven’t given 2025 guidance yet - that comes next week. I may well end up with egg on my face, but I feel reasonably confident WPP are good for that medium-term framework as a minimum commitment. For all the reasons I have already set out, I think the pieces are now in place for a change in WPP’s economic fortunes, and we may start to get some stronger signals next week. But beyond what they’ve already set out in the framework, it’s worth circling back to economic models again, in order to ponder about what the future may hold.

We talked earlier about pricing and how the industry had shifted from commission to input-based pricing, to its detriment. While they don’t provide a breakdown, WPP have said that “significant” parts of their business are on fee-based models (although not only billable hours), “relatively smaller” parts are on commission and a number of parts are on output-based pricing models. I don’t believe that the medium-term framework incorporates assumptions about pricing models yet (“I think it’s too early to say how [genAI] will affect the pricing model”) - but they do talk about how their strategy is likely to enable new pricing models. In particular they see scope for technology license fees as well as a shift to output-based models. For those elements of the business that could be more likely to remain fee-based, they see opportunities to increase the scope of work while improving efficiency. All of these things are net positives for margin, potentially very significantly. But we’ll have to see how things evolve.

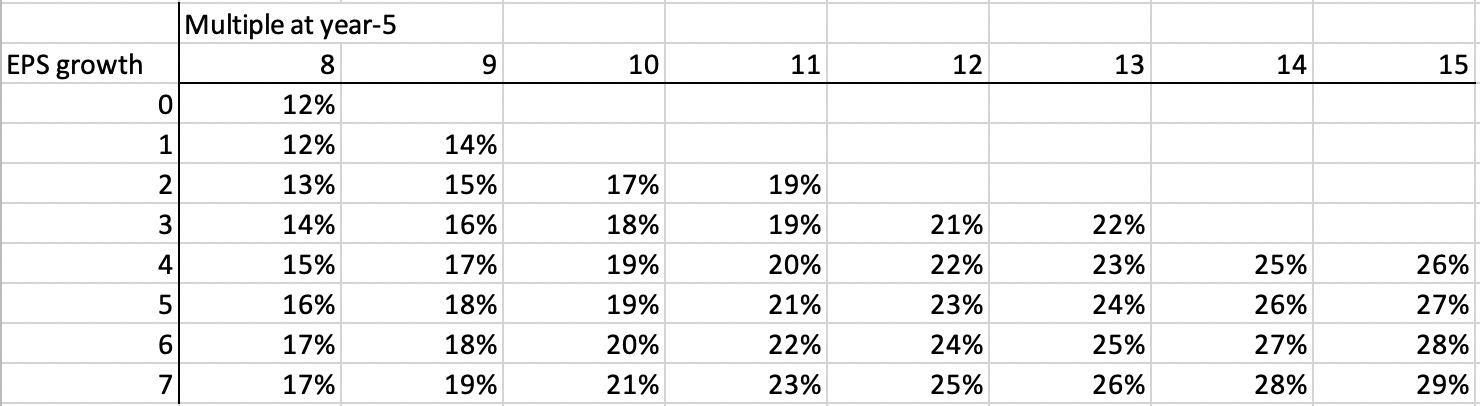

Now here’s a really basic IRR model, just to a give a notion of the possibilities from here (I’ve excluded some of the less reasonable scenarios):

First of all, you should of course take this with a pinch of salt. For example, 12% IRR with no growth assumes all the earnings/cash are paid out, which is probably not realistic. It’s purely meant to demonstrate how interesting things can be when you get a little growth combined with multiple expansion off a low base. As to exactly where things go from here - I don’t know, but I’ll be watching. But I’m happy to take the 5.5% growth (see above) combined with a Publicis-like multiple of ~13x as a reasonable base case. Is WPP a multibagger from here? Time will tell.

Thanks for reading.