WPP: Lost Cause or Cause for Hope?

WPP’s weaknesses are well known: strategic missteps, execution failures, business-model pressure and disruption risk. Less understood is the possibility of genuine renewal.

Friends of NFTBC.

It’s been seven months since I last wrote anything about WPP. It feels like the right time for a new post. Seven months ago I wondered whether WPP’s new CEO, Cindy Rose, would continue with some version of the strategy in motion at the time, or whether she would pivot to something else. The answer has now landed, and I shall come to that shortly. The stock is, of course, more or less a write-off yet WPP remains a really interesting business to think about - positioned on one of the first stretches of beach to face the AI tidal wave. That’s the perception anyway.

Even before generative AI washed onto the scene, there were some serious doubts about the sustainability of the agency holding company model, for example:

low switching costs: agencies constantly have to battle it out in competitive pitches to retain business

time and materials model: agencies capture little of the upside, even when they create major client value

pressure on client budgets: marketing came to be viewed more as a potential efficiency saving rather than a long-term growth investment. This drove expenditure to channels defined by ‘metrics’ that could be easily quantified, rather than the less quickly measurable outcomes and fat-tailed nature of creative brand and marketing campaigns. The result was ever greater share of spend captured by the digital ad platforms

Tight budgets, low switching costs and ever-greater workload for limited pay has meant generally anaemic growth and capped margins. Yet in 2026 the agency holding companies face two further existential questions:

What does it mean for a time and materials industry when work takes less time and fewer people?

Will professional marketing services even be required at all?

It should be fairly clear to most investors that we are still only in the foothills of whatever disruptive changes will be brought upon the world of business by generative AI. But we are already far enough in such that investors are beginning to ask questions about terminal values in those industries perceived to be losers - most notably, this includes software in 2026. But the marketing services industry was singled out as an obvious casualty even earlier on in the process. After all, what is the point of paying for professional marketing services in a world with Zuckerberg’s ‘black box’, Claude for Marketing, Veo and Pomelli.

Putting it all together, WPP’s highly distressed valuation implies that investors don’t hold out any hope at all. And even within this swirling tempest of uncertainties, WPP is perceived by investors to have adopted the absolute worst strategy and to be the most chronically mismanaged of the bunch:

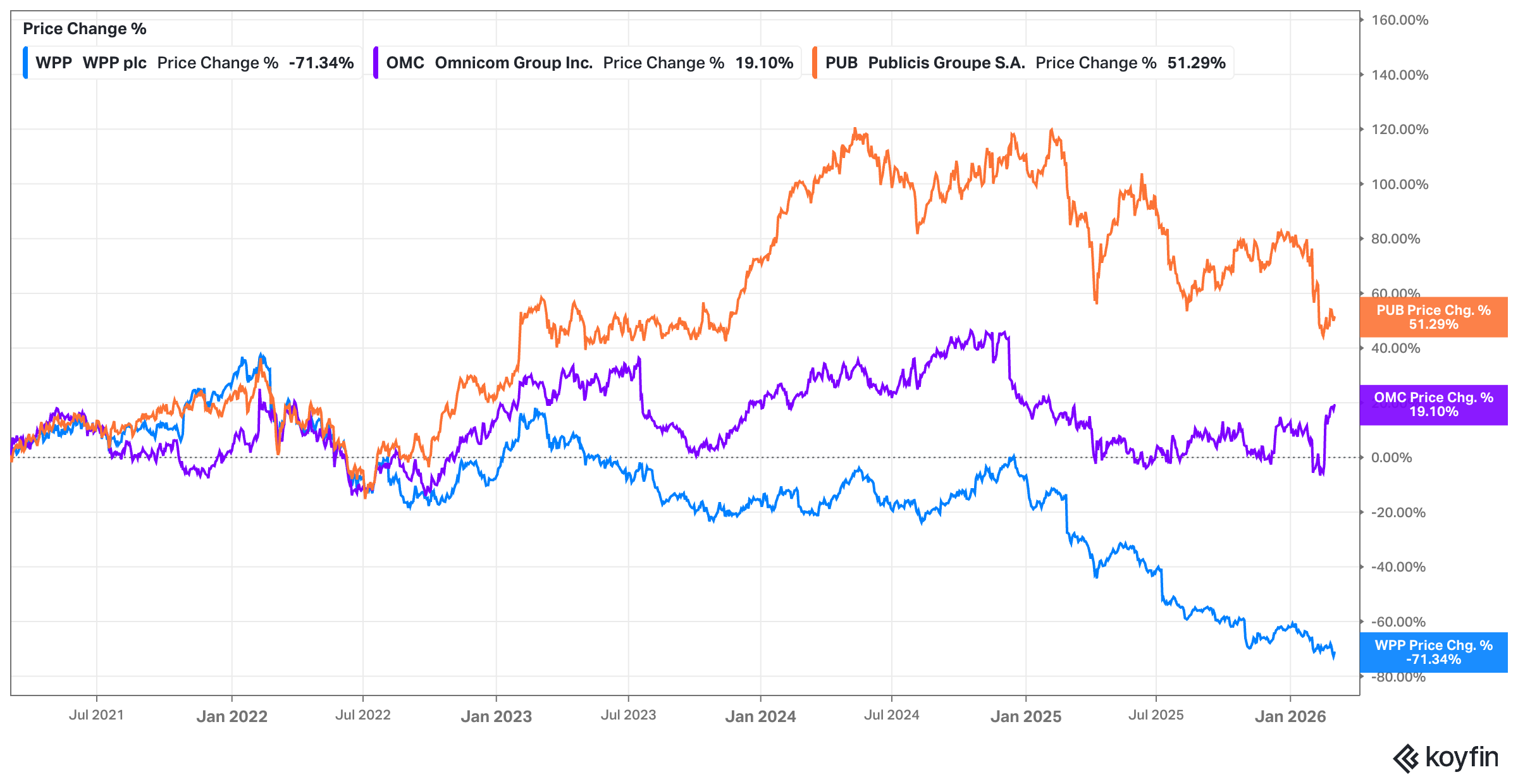

On a comparable EV/Revenue multiple WPP is at ~0.45x, compared to ~1.1x for OMC and PUB.1 This effectively puts WPP in the same valuation territory as supermarkets, notwithstanding even-currently-depressed margins that are 3-4x higher. “Perhaps there’s a looming debt crisis to cause such distress?”, I hear you ask. Nope! WPP has no covenants on its debt and all maturities in the next 12 months are covered by cash already on hand. There has been a complete collapse in confidence as to WPP’s prospects of doing anything other than spiral into rapid and terminal decline.

But what if, rather than what I outlined above, things start evolving in a direction that looks even just a bit more like this?:

I think it’s an interesting question to entertain at least, even if it’s very hard to imagine right now.

What follows is some of my musings on the current state of affairs, reflections on what went wrong last year and thoughts about where things could go next.

[NFTBC does not give advice - please do your own research. I currently have a small holding in WPP shares].

What Went Wrong

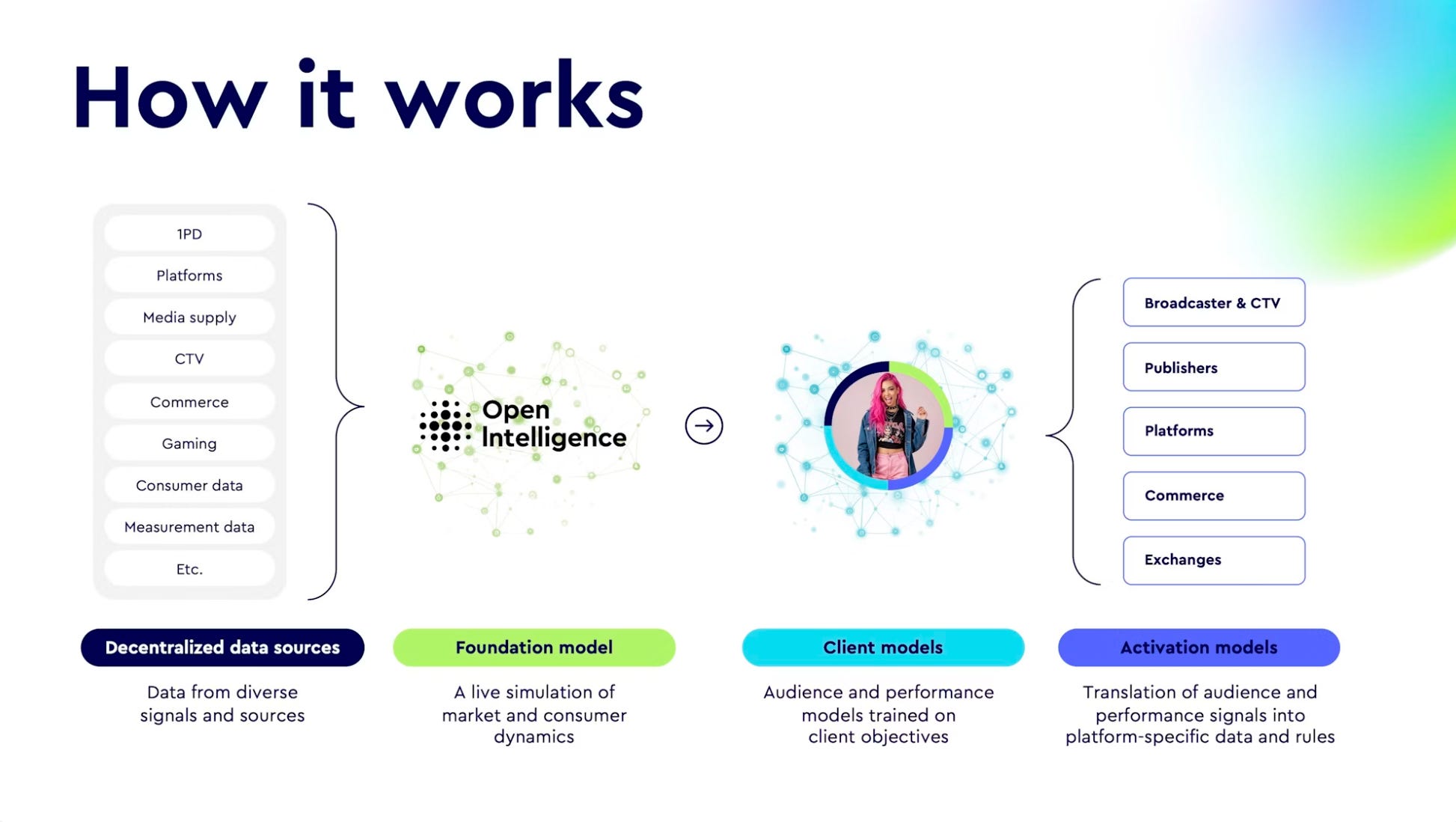

Last year, I outlined WPP’s strategy here. With hindsight I think I was perhaps around two years too early!2 Briefly, the company had undergone years of simplification in order to transition from the historic holdco model into one that is more integrated and future-facing. From around 2020/2021 they started to build their WPP Open software platform - an end-to-end AI-powered “operating system” for marketing. When ChatGPT launched in November 2022, WPP’s AI strategy was already somewhat defined and in motion - which is actually kind of impressive when you consider how many businesses still haven’t reached this stage in 2026. I won’t repeat a full description here (see the above link), except to say there’s not much else like WPP Open on the market in terms of completeness and capabilities (both internally derived and externally partnered). Already a year ago the system was rapidly maturing (see demo) and it’s now mature enough to offer as a unique self-serve SaaS end-to-end marketing platform. More recently they went live with AgentHub - a central library of verified/validated AI agents for use in internal and client workflows. WPP Open is one of two foundational layers to the business today. The problem is, I missed the other one…

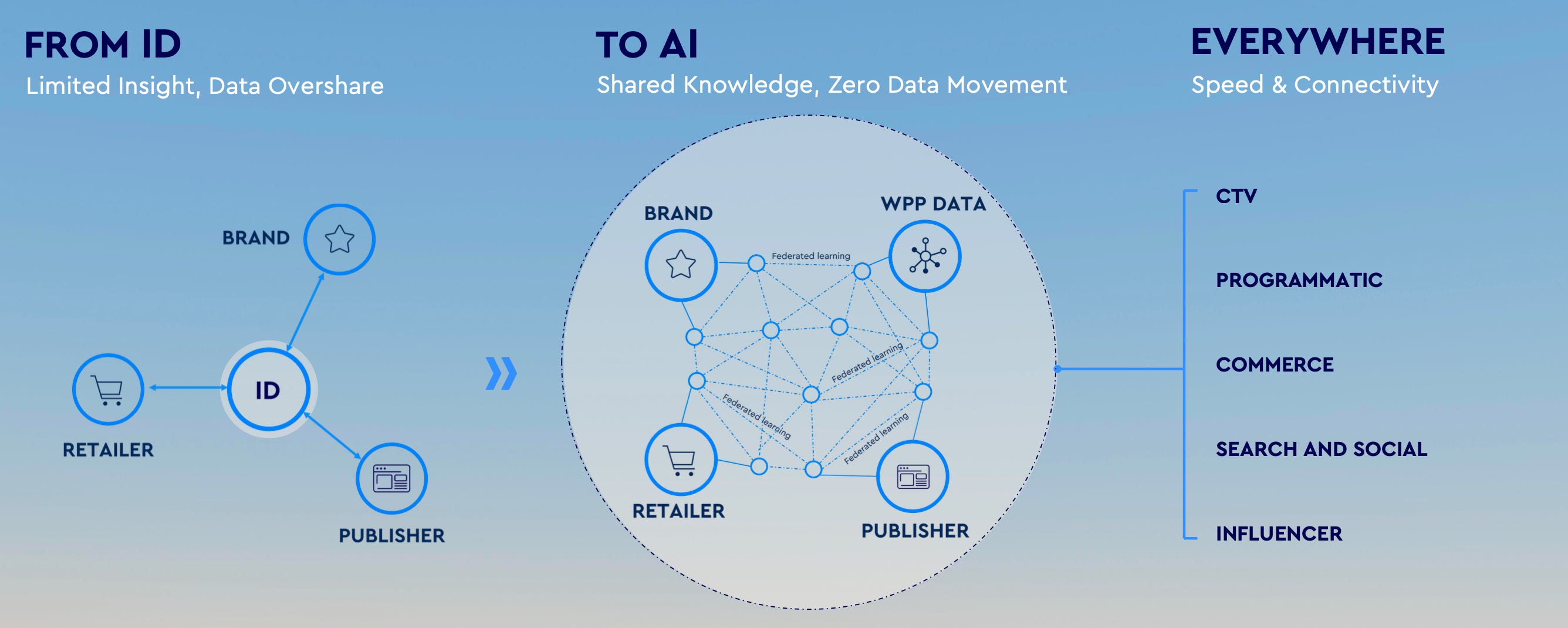

I hadn’t yet fully appreciated just how incomplete WPP’s data strategy had become in the eye of clients - especially relative to Publicis which owns some of the largest identity assets in the world for the purposes of customer ID resolution and targeting. WPP, all of a sudden, found itself looking uncompetitive in a number of defensive pitches last year and lost important accounts to Publicis. The most important step towards closing this competitiveness gap was last May’s acquisition of InfoSum, which I wrote about in detail here. InfoSum (which WPP was already partnered with) is an innovative data collaboration platform, that allows partners to collaborate on their datasets without having to move their proprietary data anywhere or upload it into a third party environment - thereby overcoming previous barriers around trust and privacy. And by breaking down the trust/privacy barrier you can bring together disparate and essentially unlimited datasets, of which traditional ID might only be one part. WPP calls this approach federated learning.

In theory, this makes for a potentially much more context-rich array of signals than ID-first approaches. From these signals WPP and clients can makes new kinds of predictions: Instead of determining “this user is X”, you can ask “given the current context, what is the probability of conversion?” You can move from targeting known customers to predicting unknown audiences.

A month after the acquisition, WPP announced Open Intelligence, which integrates InfoSum into WPP Open to make it accessible to clients and embed it into the workflow. Such an approach is, as you would expect, only limited by the number of collaboration partners you have - so they made sure to pair the launch with a decent name drop at the time. The more data partners they have, the more valuable Open Intelligence becomes.

But the thing is, Open Intelligence didn’t exactly go live in June, there was a staggered rollout over the remainder of 2025. WPP lost the Coca-Cola US media account to Publicis in March 2025, months too early to be saved. The Mars media account went right at the beginning of June - again too late. Together these two accounted for perhaps $2.5bn in billings lost to Publicis.

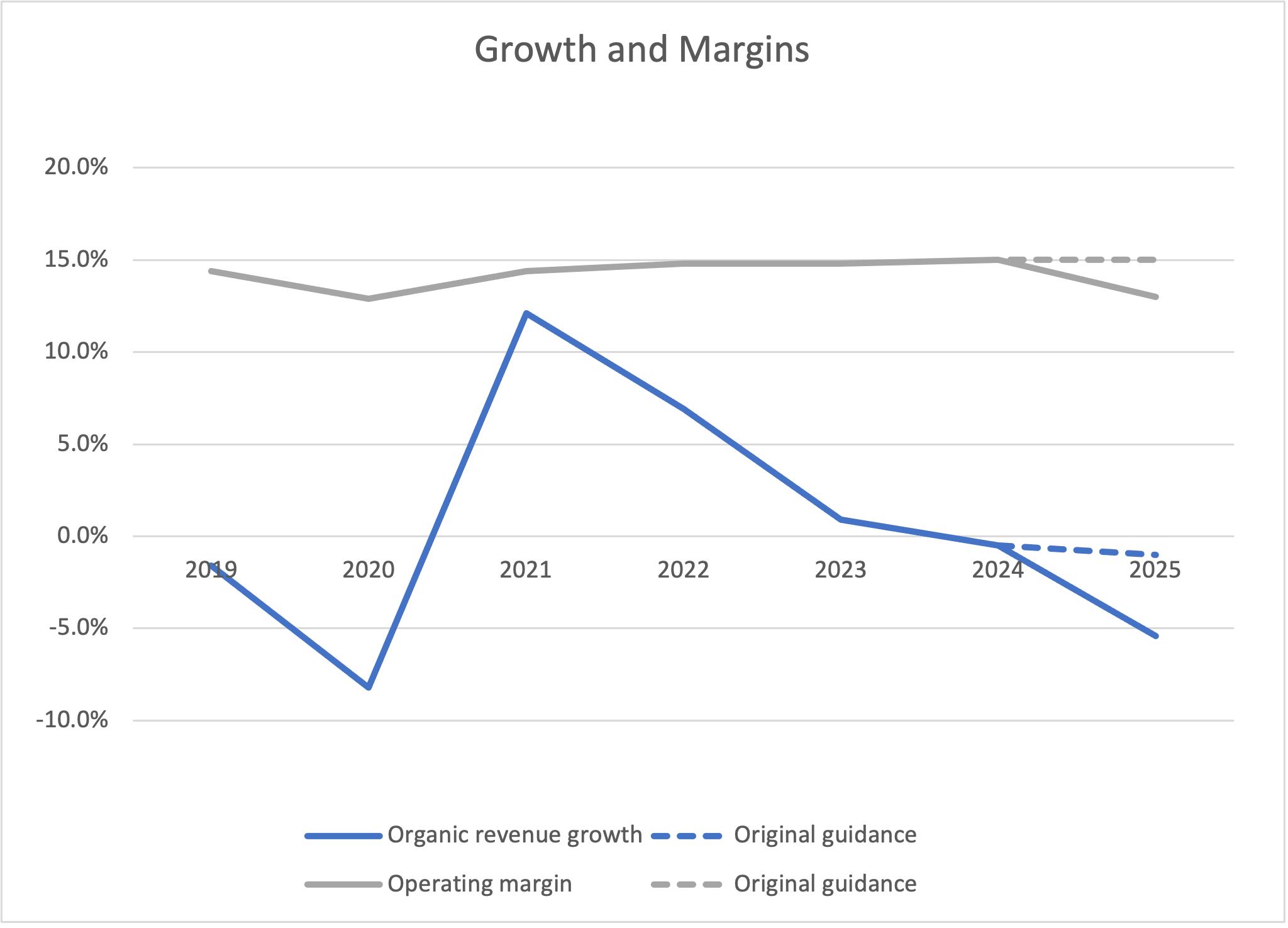

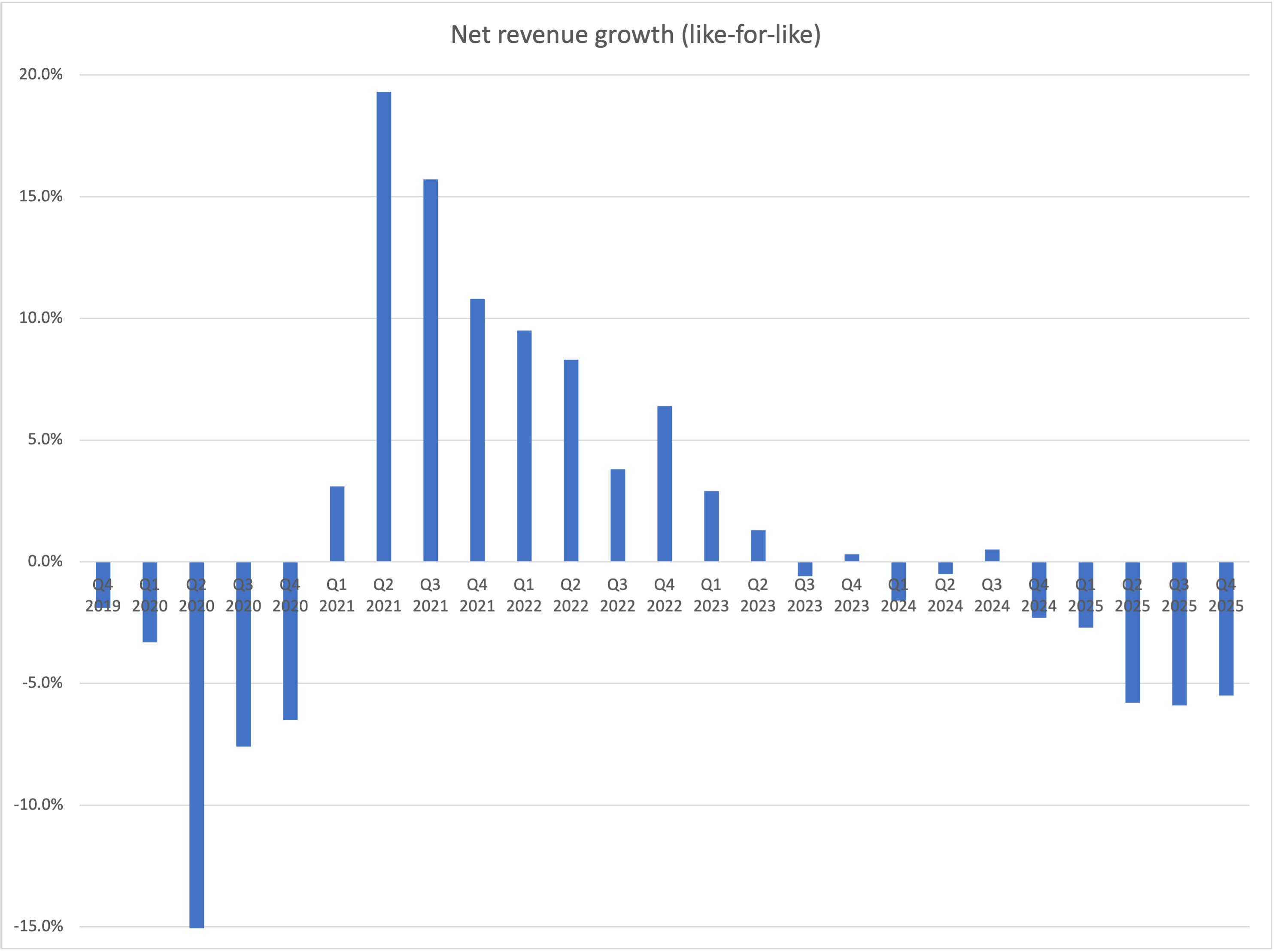

Also at the end of May 2025, WPP announced yet another restructuring in its media organisation to transition it to a single operating model (“WPP Media”), entailing yet more layoffs and disruption. They admitted on their recent Q4 results call this caused some unquantified disruption to revenue performance last year, and that’s in a year where clients were generally cutting spend due to the uncertainty around tariffs and where pitching activity was down 10% year-on-year. In 2025 WPP’s like-for-like revenue declined by 5.4%, of which 150bps was net client losses and another 400bps in cuts from existing clients - ~11pp worse than PUB!

2025 was supposed to be a transition year - roughly flat margins and growth while they made some additional technology investments and cycled some remaining client losses from the prior year. In the end growth was almost 450bps behind initial guidance, and operating margin 200bps behind (operating deleverage and 100bps in severance costs):

The impact of gross client losses in 2026 (i.e. excluding impact from wins) is expected to be a 500-600bps headwind, so from a revenue perspective WPP will have its hands tied behind its back this year. But the more important question is: can they turn their win-rate around?

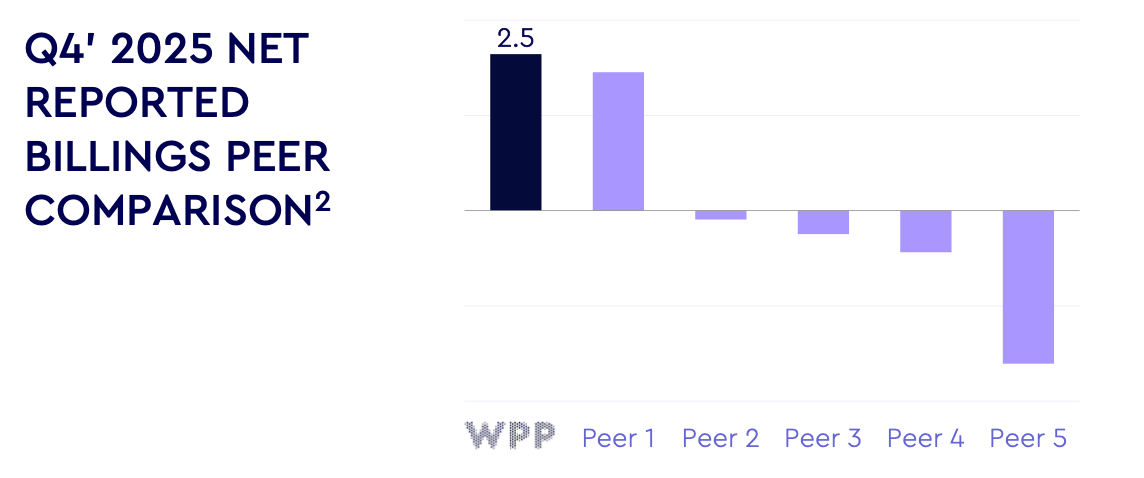

In the end, pitch performance started to turn around dramatically starting from August 2025 with the Mastercard media account, followed by Reckitt and Henkel in November and the UK Government and Jaguar Land Rover in December - among others. And this has continued into 2026 with SC Johnson and Norwegian Cruise Lines in January and Estée Lauder in February. Per JP Morgan estimates (cited by WPP), WPP had the strongest billings quarter among all of its peers in Q4 2025:

WPP say that Q4 2025 saw their strongest billings in five years. And just two months into the year the expected 2026 revenue impact from the current win pipeline already exceeds the total win-driven revenue impact seen in 2025. However, given the delayed revenue impact of all the wins and losses, H1 2026 looks like it’s going to be very ugly, with a recovery from H2 when the new business finally kicks in. The swing factor will be spend from existing clients and whether or not we see a recovery. I’ll come to guidance later.

Naturally, the next question becomes: is the recent winning streak a one-off or fluke?

Cindy’s Strategy: a single operating company

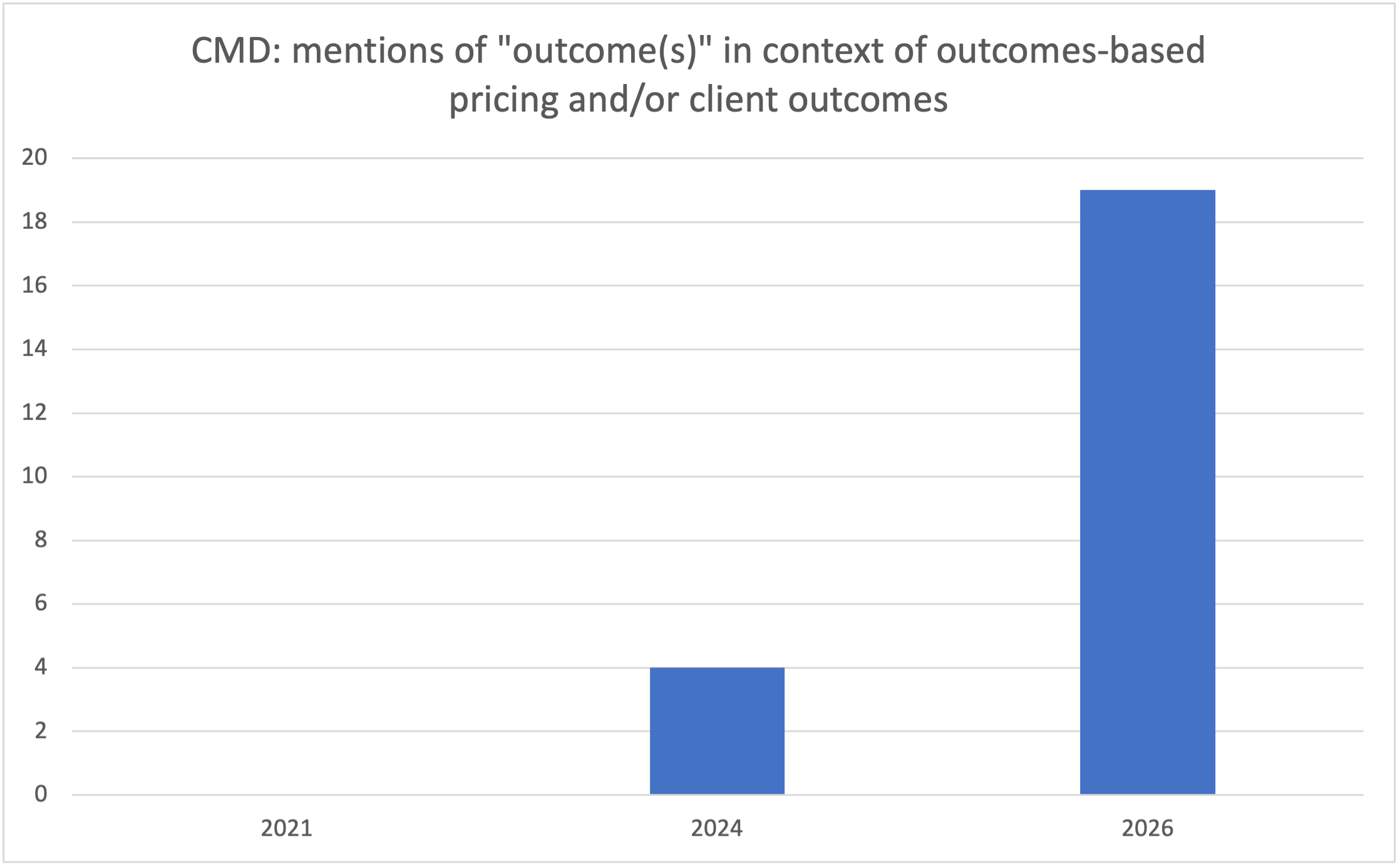

Putting on my hindsight hat once again, it now seems clear that what the previous CEO Mark Read was talking about a year ago was more of a strategic vision rather than a pitch-ready proposition. But to give him credit, he perhaps wasn’t too far off by the time he “retired” last Summer. To help demonstrate the point graphically, this is where he had got to at the time of the Capital Markets Day in early 2024:

Six months into the job, this is what Cindy Rose is presenting today:

As a reminder, Rose is a Microsoft alumnus (COO Global Enterprise Sales) who has been on the WPP board since 2019. I wondered last Summer whether she would pivot to more of Publicis-type strategy or continue some version of Read’s strategy. The answer is: a bit of both. What definitely remains is the WPP Open and federated learning foundation. I’ll talk here about what’s changed.

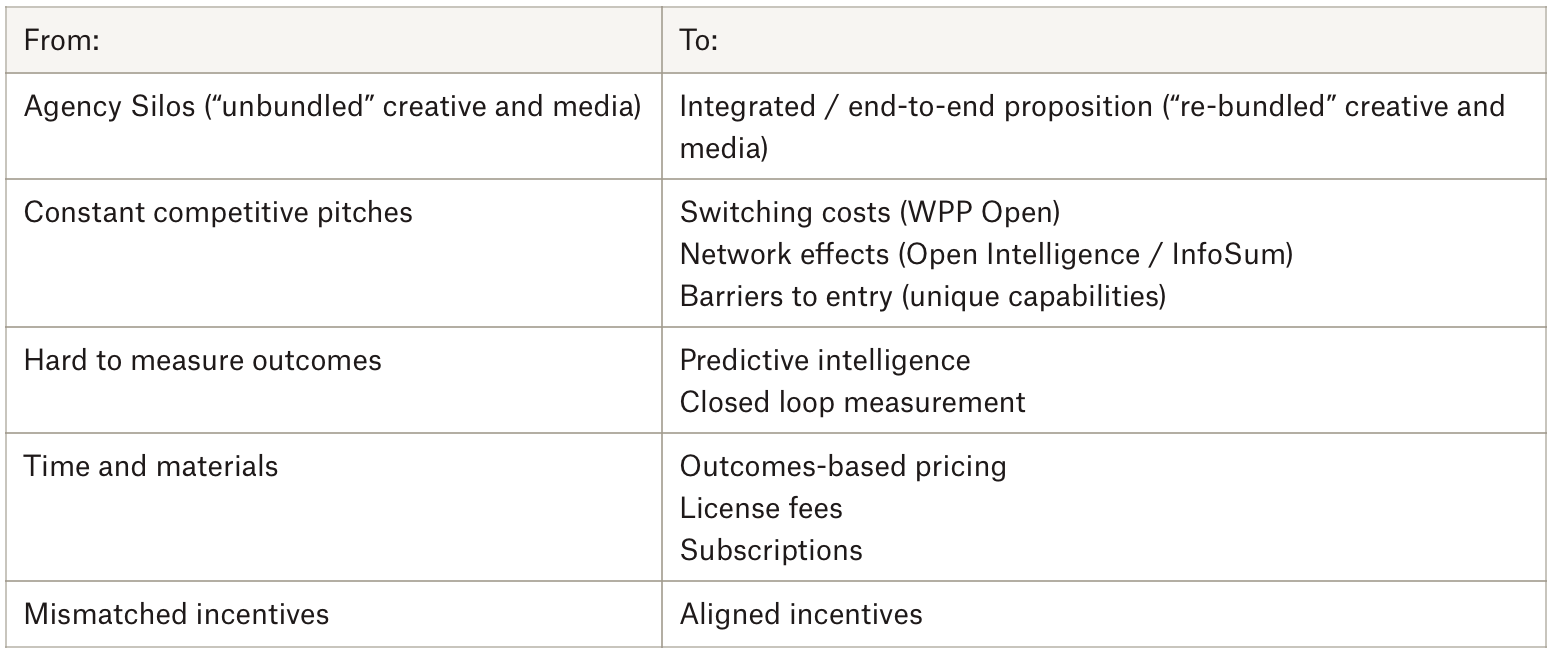

About a decade ago Publicis’ previous CEO announced a new strategy called The Power of One - a strategy that his successor Arthur Sadoun has pursued relentlessly and very successfully. The basic idea was to break down the traditional agency company silos and be able to offer clients more integrated and holistic solutions - all while hanging onto many of the individual agency brand names. Get it right and you can re-bundle3 creative and media, drive better client outcomes and win pitches more consistency. It’s worked fantastically well. Mark Read actually, in many respects, set off in a similar direction - OpenX is a successful example of this. But he never quite managed to land the strategy into a winning proposition that could consistently win in pitches - we discussed the data part earlier, but what else did he get wrong?

Rose believes she knows the answer:

Clients pointed to the fact that our complexity got in the way of true client obsession. We were siloed. We were hard to navigate. We haven’t been intentional enough about evolving our integrated proposition to adapt to the changing needs of our clients.

Now the good news from my perspective is that all of these issues are fixable. And as I said, we’ve already started to do so.

To build on our current momentum and make it sustainable, we need to radically simplify our organization really to unlock true client centricity. So to do that, WPP will no longer be a holding company. We will no longer be a shopping basket full of stand-alone businesses, hundreds of stand-alone businesses.

We’re going to move to a single company model. with 4 operating units across 4 regions with incentives that closely align to the overall performance of WPP. Being a single company with a simpler structure and common incentives are critical enablers of our strategy.

If WPP was only setting off on this simplification journey today, I think the business would most likely be in serious trouble. But, despite Rose’s dramatic terminology (“radically simplify”) the heavy lifting has already been done - we’re mostly talking about tweaks here. I think you can roughly split these fixes/tweaks into several overlapping flavours:

Narrative

Structural

Incentives

At the most basic/obvious level it seems pretty clear that Rose just wants to tell the story better than her predecessor did - and she does seem to be better at this, I would argue (as is Arthur Sadoun). From listening to others, she seems to have been received reasonably well internally so far, in contrast to declining morale under Read. And I wouldn’t be surprised to see a similar spillover effect into client attitudes. And it’s clear that WPP is now increasingly going into pitches as a unified “WPP” rather than a collection of siloed agencies - story telling.

On structure, the main change to call out here is the creation of WPP Creative which unifies the various creative agencies into single regional P&Ls with more shared corporate function - all while maintaining the individual identities. Per WPP, the simplified corporate structure allows for new common incentives:

At the heart of WPP’s relationship with our largest clients are our global client leaders, our GCLs -- and our GCLs are already masters of creating value. But our existing operating model and our incentives and our internal processes have not always afforded them the agility needed to deliver seamless client-centric services that unlock new avenues for growth.

We’re transforming our approach. We’re going to empower our GCLs with the authority and the resources to function as true leaders for their client portfolios, exercising strategic leadership rather than merely orchestrating a bunch of activities. This is going to include greater control over client P&Ls and the authority to make the best strategic decisions supported by streamlined internal processes designed to eliminate organizational friction and provide access to the right resource at the right time.

We’re also establishing a new team of client solution architects. This team will apply deep industry expertise to develop winning growth strategies for clients and then architect tailored solutions to deliver on those strategies, unifying technology, media data, all of our marketing capabilities to really drive successful execution.

Now here’s the interesting part:

If you’re sitting in an operating unit, your incentives are 50% tied to your operating unit and 50% tied to WPP. If you’re in WPP as part of a corporate function, you’re 100% WPP. If you’re a GCL, you’re paid on your client growth. It’s that simple. And it’s dramatically different from where we are today, where if you’re in an agency, you’re paid on your agency results primarily.

So that is very, very different. And that’s why I think it’s going to unlock very different behavior, much different collaboration. In the past, our agencies competed with each other. That was the model. Today, when we go into a pitch, we cast the right resource for the right client at the right time and -- it enables that.

It enables a much more client-centric approach to the business. Just to add, we’re implementing that in 2026.

Client growth was a topic that came up a lot in WPP’s latest investor presentation - much more than in the past. And it’s an important point. Brands haven’t been growing as fast as they used to and you have to ask if part of the reason is the time-and-materials model that does away with upside capture. Upside capture kills two birds with one stone: 1) aligned incentives: WPP wins when the client wins and 2) it solves for the time-and-materials problem in the world of AI. In 2024 this was the vision, whereas in 2026 they’re pushing it as the reality. So here we come to the crux of it all: is WPP now in a strong enough position to be able to pitch client outcomes linked to outcomes-based pricing?

When WPP won the Jaguar Land Rover pitch in December, they won the whole lot: creative and media. Getting both accounts at once hasn’t been the norm in a long time (since the days of bundled creative and media), although Publicis has been making inroads with its Power of One strategy. Here’s what Johnny Horny said (who led the JLR pitch):

So starting with Open Intelligence to be able to build cohorts and understand audiences in a way that doesn’t require us to do simply old-fashioned ID matching, but to keep the data where it is, keep it safe and secure and then put that into a team that we’re going to build with JLR, where we and they are all together on the open platform end-to-end. And it’s the end-to-end integrated nature of this offer that I think then allows us to make what I think are becoming genuinely competitive offers when it comes to outcomes.

So those outcomes aren’t do you like the agency you work with, those outcomes are, are we selling more product? And will we get paid on being able to sell more product by being able to build their brands and measurably show that there’s greater levels of desire for their products and the crown jewels of brands that they’ve got. So we haven’t finished contracting, but those are the defining - and that pitch was against all the major holding companies - I think those are going to be the integrated propositions that will see us win JLR and hopefully many more JLRs pulling these ingredients together.

And CFO, Joanne Wilson :

Navigating through what is an incredibly and ever more complex ecosystem is incredibly challenging for CMOs. It’s getting tougher and tougher. And that’s what they’re paying us for. It’s no longer they’re paying for us to create 5 ads.

In fact, we can create 1,000 ads, but it’s how do you get those ads into the right audiences.

And that’s really what they’re paying for, which is really enabling this output-based pricing, it’s outcome-based pricing, and it’s also shifting more to tech fees and licensing fees as well. So this will be an evolution, but we’re making lots of progress in this area.

Part of the key to outcomes is “closing the loop” on measurement. And they cited Heineken as an example:

Consider our work with Heineken. They needed a way to connect their first-party consumer data with ITV’s on-demand viewing audience and Tesco shoppers.

Powered by InfoSum, Heineken was able to identify relevant audience segments based on age and real-time drinking preferences. Crucially, Tesco provided closed-loop measurement of sales impact, all without moving or sharing any customer data out of Heineken’s environment. In a world where measurable outcomes truly matter, the campaign success wasn’t measured in brand uplift or impressions, but in real sales data from Tesco stores, which increased by an impressive 189%.

If they can turn this into a repeatable process, then the prospect of an emerging moat might not seem so farfetched after all. But it remains, of course, too soon to tell and much will depend on execution.

Loose Ends / FAQs

Is WPP Open easily replicable? Could it be vibe coded?

I think there are two answers to this. The first one is yes - the bare bones of a marketing software tool with API links to model providers would be easy to get up and running. But it’s a lot more complicated than that. To start with there’s WPP’s proprietary IP which includes decades of brand and campaign data used to train proprietary models and inform proprietary agents (outside of the newly enlarged Omnicom it’s doubtful anyone has more of this). Then there’s WPP Media and Open Intelligence. A startup software effort on the creative and production side, for example, isn’t going to have any of the media and data infrastructure that are necessary for buying the right ad inventory - and that’s half the battle. Then there’s the challenge of getting to stable release with ongoing support and maintenance - WPP Open is now serving more than 70,000 regular users. There are barriers to entry.

Importantly, most of the putative WPP Open alternatives (including those emerging from the AI labs) are essentially point solutions and frequently tied to some kind of data or technology platform. Whereas WPP Open covers the entire marketing workflow (planning » creative » production » media + commerce) and it’s ‘open’ (you choose which data, third-party tools and models to use) - for the needs of your typical large brand-based business it’s arguably very differentiated.

Could InfoSum be vibe coded?

I think this could be more challenging given InfoSum’s higher complexity - moreover, a number of the innovations behind it are patented. But even then, anyone starting afresh would have to rebuild the network effects that come from onboarding increasing numbers of partners.

Existing client spend - is something broken?

As noted, existing clients cut spending with WPP in 2025 resulting in a 400bps headwind. Other than the WPP Media disruption, WPP attributes this to sudden cuts in discretionary project spend, especially beginning in Q2 at the time of the ‘Liberation Day’ tariff announcement. WPP has tended to have a disproportionate share of project spend in agencies such as AKQA. Qualitatively, peers such as Omnicom and Dentsu have reported similar trends in 2025. But one might be tempted to ask: did something change in 2025, e.g. are clients using AI for some work instead? I’m somewhat suspicious. I think we’ll have to wait and see.

Do we even need professional marketing services anymore?

The risk, perhaps, is that the trend towards viewing marketing as a discretionary expense to be squeezed (i.e. rather than a necessary growth investment) continues to snowball from here. This could push an increasing proportion of share either to Zuckerberg-style black boxes or to in-sourcing (“we’ll do it ourselves”). But it seems to me that black boxes are likely to be most relevant to small businesses merely looking to increase their surface area, in contrast to the more demanding complex nature of brand campaigns (Zuckerberg himself has essentially said as much himself). On in-sourcing, I kind of view this argument as related to the ongoing software debates. Many businesses already do some degree of marketing and software work in-house, and yet continue to outsource these functions in large part. Perhaps the main difference is that while software is near-term mission-critical, marketing is medium- to long-term mission critical. Ultimately we’ll have to see how this develops over time. My general feeling is that those brands that squeeze efficiency too hard, try to do too much themselves or surrender entirely to automation will seriously struggle - if anything, the incoming tidal wave of AI-generated content is going to make imaginative and innovative marketing campaigns more important than ever for those advertisers who wish to stand out in a sea of undifferentiated ‘AI slop’. For all the automation that WPP Open provides, it centres around keeping talented creative professionals very much inside and driving the process. But I fully expect this point to remain contentious for some time and readers will undoubtedly have their own views.

Where next? / thoughts on valuation

Given the distressed valuation, my working assumption remains that WPP is highly vulnerable to takeover - probably by private equity. But if they do manage to remain independent, the basic announced plan is this:

2026: Stabilise the business. LFL revenue growth to decline mid- to high-single digit in H1 and improve thereafter. Operating margin 12-13% (-100bps to flat)

2027: Return to positive LFL growth and start to rebuild margins

2028: Accelerate growth and margins

2026 is shaping up to be another rough year but, let’s face it, the bar is low at this stage. In order to work out reasonably well from here I think WPP merely needs to persuade investors of its right to exist. If they can continue to win client pitches and simply stop shrinking, I think that should be sufficient - and it could be on the cards for the second half of 2026. Quarterly comps get much easier in the second half of 2026, especially in the context of Q4 2025 which was the strongest billings quarter since 2020.

The last time WPP faced sentiment and performance somewhat comparable to today was in 2020 - weak project work and declining revenue masked strong net billings that took a couple of quarters to start showing up. From Summer 2020 the shares surged by 100% to the end of 2021.

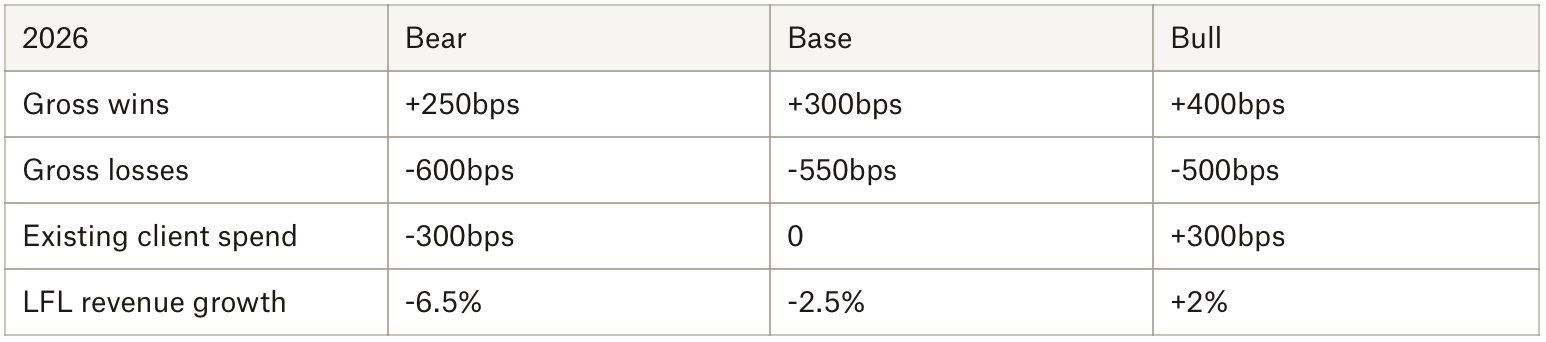

There are other considerations too. First, for 11 out of 12 months in 2025 there were four major holding companies until Interpublic was engulfed by Omnicom in November. Not only will there be significantly reduced competition in pitches, but it’s hard to imagine Omnicom being able to fight its best game during a year of heavy integration work. Second, perhaps the big swing factor for 2026 will be existing client activity. Given guidance (gross losses 500-600bps and >250bps of gross wins already baked in), we can start to think about scenarios:

Consensus is currently sitting nearer to the bear case - but the range of possible outcomes is actually kind of wide. For a stock trading at 5x consensus 2026 EPS, it’s intriguing. If something like the bear case does indeed prove to be the terminal state, then the shares might be fairly valued after all - or maybe even too high. But if it’s something more like the bull case and we exit 2026 on a healthy trajectory, I would expect a rapid normalisation to an Omnicom-like valuation or about +90% (~8x P/E on potentially stable earnings). To be clear, I think WPP is very hard to value currently, given the range of outcomes. Personally, I’m hopeful that WPP will re-establish its right to survive but I couldn’t yet tell you what a steady state might look like. If things did go well there’s no reason in principle why a path to Publicis-like performance (18% margins and consistent MSD growth) shouldn’t be the aspiration - over time. My inclination for now is to view WPP more like an option - a cheap option.

Other things to look out for in 2026:

They more or less confirmed they’ll be doing some divestments this year. For me, the lead candidate seems to be Burson, their public relations business, which I see as peripheral to the strategy. If they can get just 1x revenue for it, that would be around 25% of the market cap and 7% of net revenue. Even after some degree of net debt reduction, there could be scope for a significant buyback that more than offsets the divested earnings.

Rose made clear that she want to keeps the narrative going with investors throughout the year: there will be three webinars on each of WPP Media, Production and Enterprise.

That’s it. Thanks for reading!

Note that OMC does not provide a net revenue figure. EV/Net Revenue for WPP is ~0.6x and ~1.2x for PUB.

Which is indistinguishable from being wrong - I know, I know…

I’ve written before about the unbundling of creative and media several decades ago. The start of a slippery slope resulting in pricing pressure for agencies and less effective work for clients.