WPP x InfoSum

'Playing Leapfrog' (or leaping the frog 🐸 🤭 )

Friends of NFTBC.

Since starting NFTBC earlier in the year, my biggest flop so far is the WPP post - in terms of engagement and share price performance (both dismal!) My only regret however is the subtitle (“…Multibagger?”) I had 15 subscribers at the time (200 now) and with hindsight I was trying a little too hard simply to get anyone to pay attention - anyone at all. To rub salt in the wound, I was shortly thereafter introduced to Betteridge’s Law of Headlines which states “Any headline that ends in a question mark can be answered by the word no” 🤦♂️.

I will continue to learn lessons and to evolve this blog, and in the coming weeks I intend to provide an update on future direction. But one thing I have taken away from the WPP post is that I was selling it too hard. I don’t really want NFTBC to be about me trying to persuade anyone about anything (or perish the thought - to buy anything). One of my favourite writers, the philosopher John Gray, often says that he doesn’t write to persuade people, but to get them to think - to engage with his ideas. In a similar vein, I want to write about stocks and related matters that I think are interesting, overlooked and worthy of some kind of reflection. If I find such things interesting, my hope is that there might be some sliver of audience out there who does too, whether they ultimately agree with me or not. As it happens, the stocks I write about will often be ones that I either currently own or am thinking about owning. I’ll write more about this at a later date.

Back to WPP. Outside of WPP itself, I don’t personally know anyone who’s bullish on the shares. Even inside the company, WPP is by no means universally popular. I’ll admit that WPP might very well be hated for good reason, but on the other hand I also note that for one of my best compounding stocks of the last five years (IRR >25%) there was a very similar backdrop initially - everyone seemingly hated this company. Investors, employees, customers - you name it. The company was accused of having an antiquated strategy that was no longer working - it was ex-growth and going extinct, a dinosaur. In reality, this company was trying something different, and it took a little time for the results to become fully manifest - today this business is a double-digit grower and still accelerating.

WPP, too, is trying something different. And that makes it interesting to me. But doing something different frequently comes across as weird, eccentric or just plain foolish, unless and until it starts showing results. In the latter part of 2024, it seemed to me that WPP’s strategy was showing early signs of success and setting the scene for a modest acceleration this year. But then along came Q4 and we seemed to go back to square one. I won’t revisit the full story here, but please do dive in if you’re intrigued.

WPP

Welcome to the second published stock idea, here at NFTBC. It’s WPP. For more context about this substack, please head over to the NFTBC intro piece. My gratitude to everyone who has read my work so far. If you like what you read, I would be grateful if you share it around. You can also find me on

The short version is that WPP has been reinventing itself around end-to-end marketing automation - essentially an internally-developed marketing software stack called ‘WPP Open’ that can be used both internally and by clients. Everything that can be automated, has been or soon will be, while still leaving a central role for WPP’s ‘creatives’ - genuine human creativity, being one of the few remaining things that cannot yet be automated (and perhaps never will be). If it works, then marketing becomes cheaper and more effective - and in a way that’s tough to replicate, lowers client churn and operates outside the walled gardens of the digital ad giants. It’s too soon to conclude whether it’s working and to what extent, but investors are hardly looking at all - in the meantime I continue my investigations…

The ‘Missing Piece’

In my WPP post I discussed the company’s sophisticated data and AI strategy, all geared towards increasing the effectiveness and economics of advertising for clients. The perceived problem is that, relative to its major peers, WPP’s own proprietary data assets are more modest in size. I’ll get into this a bit more later, but it really helps to explain why French rival Publicis’ media business is very significantly outperforming WPP’s, for example.

In early April WPP acquired InfoSum. Here’s how the press release put it:

WPP today announced the acquisition of InfoSum, the world’s leading data collaboration platform. InfoSum will join GroupM, WPP’s media investment group, to power the creation of a new generation of AI-enhanced marketing solutions for clients, delivered through the industry’s most powerful and secure data infrastructure.

The acquisition is a major strategic step forward for WPP’s AI-driven data offer, giving WPP and its clients immediate access to the industry’s largest cross-platform source of privacy-safe, actionable data for marketing intelligence, audience targeting, and AI model training.

“The world’s leading data collaboration platform”. OK then. That’s kind of a big claim, but also vague - so I’ve spent some time kicking the tires on InfoSum. Here’s how Mark Read weighed things up at Q1:

The InfoSum transaction is going to strengthen significantly our data proposition and we're seeing that with clients. So I think greater clarity on that is perhaps the thing that we have been missing a little bit.

And per Evan Hanlon, CEO of Choreograph (WPP’s data business): “Now, we have all the pieces”. So we have here the prospect of a ‘missing piece’ type acquisition. I’ve been wracking my brain to think of examples of genuinely transformational acquisitions where the insertion of that ‘final piece’ really did make all the difference. It’s perhaps not especially common, but there are such examples - Nvidia’s acquisition of Mellanox comes to mind. Which ones can you think of? I was initially tempted to include Publicis’ acquisition of Epsilon, but Epsilon was perhaps less of a missing piece and more of a strategic change in direction.

The Debate

If you listen to WPP’s earnings calls, there are frequently questions of the sort “when are you going to buy a database?” The reason originates in Publicis’ 2019 acquisition of Epsilon which brought with it hundreds of millions of IDs linked to individuals. Marketers use such IDs for targeting and measurement to make their campaigns more effective - and by bundling its data offering with its media offering, Publicis has been more competitive than peers at winning accounts. Here’s what Publicis CEO Arthur Sadoun has to say about it:

If you don’t add proprietary data that will bring to your clients something that they don’t have, they won’t find new sources of growth. They won’t be able to connect every individual to the entire media ecosystem.

Publicis recently doubled down on this strategy with the acquisition of Lotame. And it’s also a strategy being pursued WPP’s other largest peers - as exemplified by IPG’s acquisition of Axciom and Omnicom’s pending acquisition of IPG.

Here’s how Brian Lesser, GroupM CEO, framed WPP’s side of the debate at Q4 2024:

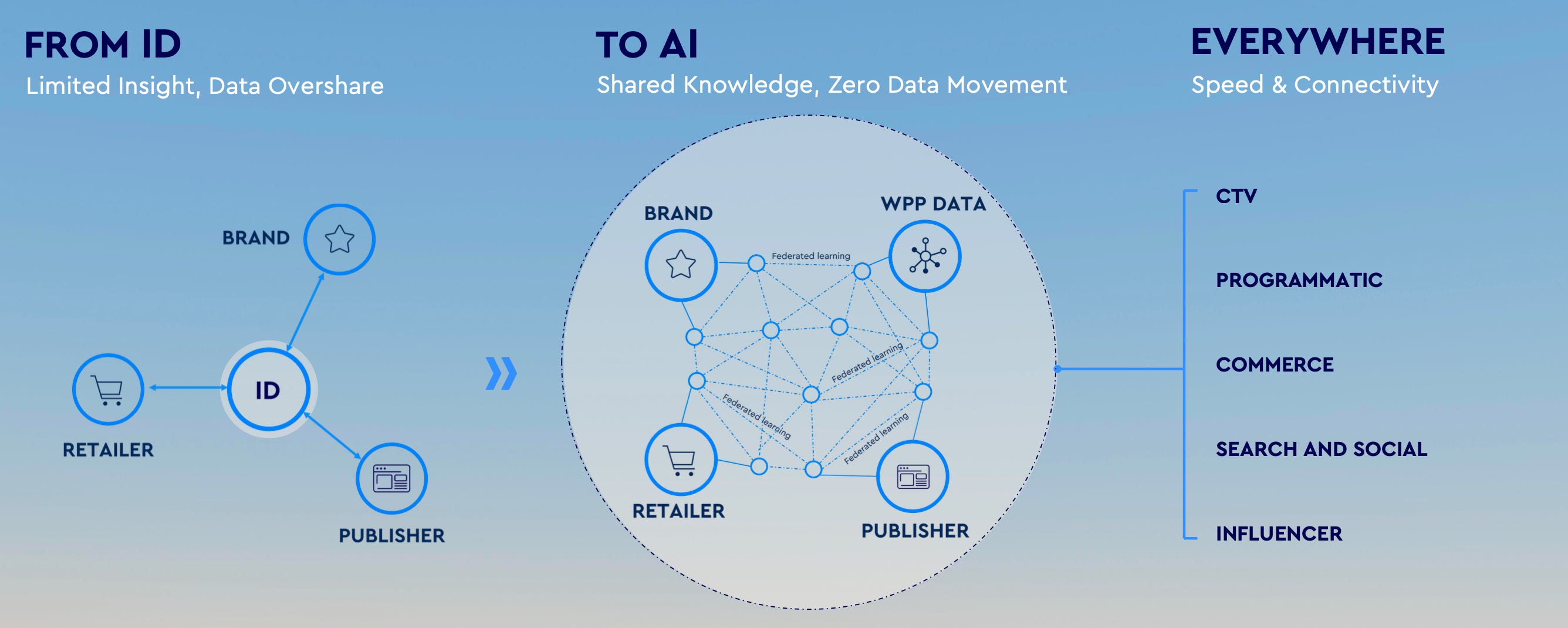

The market is quickly moving from identity-based solutions to AI-driven connectivity. Here’s what that means:

We believe that data connectivity is more important than simply owning data, and the value of connectivity will only continue to grow

No matter how many traditional IDs you own, it will never be enough. The real power lies in connecting data across publishers, partners, retailers, platforms, and clients, and thoughtfully using our own first party data assets in conjunction with the available data in the world.

The future is about connecting disparate data sets to extract insights, create predictive models, and drive performance

Traditional ID solutions, like those grounded in email addresses, only learn from overlapping data points, relying on outdated lookalike models that limit insights. Using technologies, like federated learning, we can create shared knowledge and predictions across all our partners, without sharing raw data and activate via a simple connector. It’s a game-changer. And as Mark mentioned, this will drive significant efficiencies in audience targeting and real-time campaign optimisation, tailored to clients' unique needs based on their own data maturity.

By 2030, we’ll be working with thousands of data partners to guide audience decisions. The only way to harness that scale is by leveraging AI at every step of the process. No singular, legacy database can manage that scale and complexity.

And he shared this slide:

And here is WPP’s Alex Steer (chief data officer at Choreograph):

We reckon that only around 10 to 20 percent of data that’s useful for decisions that we make in marketing can be resolved back to an individual ID about an individual person. Most of the information that businesses own comes in different types and sits in different structures. You might have data that’s organised by store, or by postcode, or by keyword. AI is really good at translating between those things, and at learning and spotting patterns.

Which approach is better then - ID or “from ID to AI”?

Frankly the debate continues and there are both sceptics and optimists. But the thing is, the ID approach is clearly working for Publicis today and at scale. Whereas WPP’s solution is earlier in its implementation, it’s new, it’s different and it raises challenges of its own - how do you deal with the trust and data privacy issues of bringing different parties together to collaborate on their proprietary data? How can you make it scaleable? Now bear in mind that WPP had not announced the InfoSum deal at the time Lesser produced his Q4 slide, but one way of looking at it is this - InfoSum is the infrastructure that allows WPP, brands, retailers, publishers, data providers and others to connect all of those ‘nodes’ together to generate unique insights, and to do so securely, quickly and easily. If federated learning is WPP’s strategy here, then InfoSum really is starting to look like a ‘missing piece’.

InfoSum

InfoSum was founded by Nick Halstead in the UK in 2016. A software engineer, serial entrepreneur and racing driver, he’s a pretty interesting fellow and you can listen to his story here. Halstead’s prior two companies had been in social media, and he had spent years working in partnership with the usual suspects:

I was really thinking about what would level the playing field for everyone else… to think about about how do you solve for data, making every company be as data rich as Facebook and Google… Some of the largest public companies out there may still have access to a couple of hundred million people, but these days it’s a global economy and people want to be able to market to literally everyone like you can on Facebook. And I was thinking about the technology that would break down those barriers of those big companies to be able to work with each other.

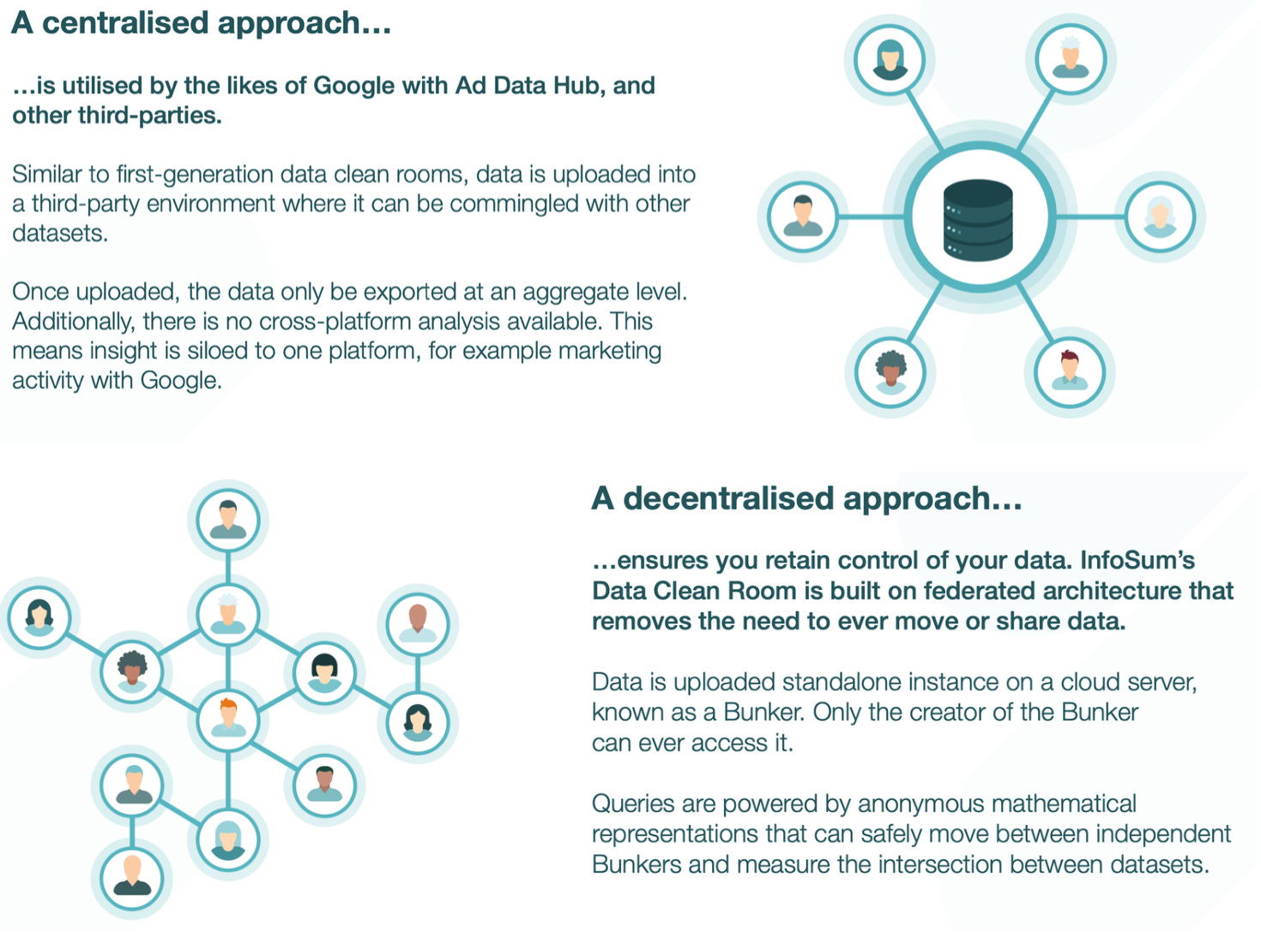

And the barriers he was talking about: trust, privacy, identity and integration. He looked at a number of approaches to integrating the first-party datasets of separate businesses but they all required centralisation, co-mingling, reversible encryption and such things. He raised venture funds and it took his team three years to build what would become InfoSum, launching in 2019. The approach itself was highly innovative, centring around what they call the “non-movement of data”. InfoSum clients never send each other their data - the system is completely decentralised, operating via patented mathematical models that never send any underlying identities.

By solving for “non-movement of data” InfoSum was able to break down Halstead’s four barriers. Customers can now collaborate without fear of data ‘leakage’ or losing commercial value to other parties - instead the parties can focus their collaboration on the upside of bringing unique and disparate datasets together (non-zero sum). The same goes for privacy concerns - customers never send their data to anyone or hand over control. Moreover, customers are able to match their shared identity footprint but without ever exposing the underlying identities, via non-reversible synthetic identifiers. Having been built from the ground-up to address these barriers, InfoSum’s argument is that most alternative data clean rooms have been designed as ‘add-ons’. Per Halstead:

[What is] utterly unique to InfoSum is that we combine the clean room, the identity matching and the data processing all through the lens of non-movement.

And because data is never moved, it makes InfoSum much faster to onboard and to use both from the perspective of data extraction and upload and from a contracting perspective. According to InfoSum CEO Lauren Wetzel, clients save 156 days on average with InfoSum, seven times faster than other platforms - while I haven’t audited these claims, it is easy to recognise how a decentralised platform could be a lot faster logistically.

Once businesses are on the InfoSum platform, it then becomes very easy for them to collaborate - they just have to agree to:

InfoSum’s extensive global data network represents hundreds of billions of data signals across multiple dimensions of data from media platforms including Channel 4, DIRECTV, ITV, Netflix, News Corp, and Samsung Ads, as well as major retailers around the world and identity and data partners including Experian, TransUnion, Circana, Dynata, and NCSolutions.

While we don’t know how big InfoSum currently is, media sources have suggested WPP paid around $150m. In any case, the deal was not a major surprise given the various hints that Lesser dropped at Q4 - moreover, Lesser himself was InfoSum CEO for four years prior to Wetzel. Cynics, of course, are saying that Lesser was self-dealing. Others have speculated that InfoSum was “treading water” with investors looking for a way out. For her part, Wetzel has stated on the record that InfoSum was doing a fundraise earlier this year (which included WPP) and during the process it became clear that the option of a takeover was compelling. With WPP already a client and familiar with the product, it was becoming clear that there was a clear strategic fit and shared mission.

Where Next?

In WPP’s words, the acquisition allows them to:

leapfrog traditional identity-based solutions that depend on decades-old, deteriorating databases weakened by cookie deprecation, platform fragmentation, and splintering audience match rates…

But the power of the transaction, is what it means in the context of WPP Open and GroupM more broadly and by integrating InfoSum's capabilities within WPP Open, our clients are able to unlock the full potential of their customer data and reach through AI in strong, quality media environments that's not always available to people using legacy first-party data systems. And using federated learning techniques, clients are able to build, train, and deploy custom AI models that they can use in a privacy compliant way. They can generate insights and audiences to create precise predictive models, optimized campaigns, and deliver measurable improvement in real time.

By integrating InfoSum directly into WPP Open, it should, in theory, make both propositions more attractive to customers. InfoSum customers can benefit from the application of WPP’s AI/ML capabilities in the interrogation of their datasets, while WPP customers will get seamless access to InfoSum’s enabling infrastructure to power their data collaborations. Moreover, one of the apparent reasons for the acquisition is to accelerate InfoSum’s roadmap, with WPP’s scale and resources - Wetzel (who is remaining as InfoSum CEO) believes they’ll be able to scale very quickly.

One outstanding question is whether InfoSum will lose its former neutrality. Will potential WPP competitors still want to partner with it? One has to assume that some degree of neutrality will be lost. But we have been told that InfoSum will continue “operating under its own identity and with its own go-to-market, working directly with clients who want to be able to do data collaborations”.

I guess we’ll just have to see how things evolve from here. Per Mark Read at Q1 2025:

So the conversations we had with clients were very positive. Dozens of conversations over the last few weeks and the feedback very positive and then we're confident the deal alongside our broader simplification efforts will drive a step change in performance, particularly in competitive reviews.

Some degree of grace period must be allowed, after which I’ll be on the lookout for that step change. But it does seem to me that Mark Read’s window of opportunity could be at risk and without signs of progress soon, there could be increased activism for change at the top. He has been CEO since 2018 and, despite profound change beneath the surface, there’s little to show in the financials or share price. If GroupM can accelerate to the sorts of growth rates achieved by Publicis’ media business, at 40% of the group total it will be enough to underpin WPP as a whole and warrant a significant P/E re-rating. Perhaps we’ll start to learn in the coming months if the puzzle is indeed complete now.

As always, get in touch if you have any comments or questions.