Cerebras: following up on the deep dive

Q1 and other post-IPO musings

Friends of NFTBC

This post is for those of you who read the Cerebras deep dive and are curious to continue following the story in the months and years ahead. A couple of evenings ago CBRS held its first earnings conference call. There are already plenty of ‘hot takes’ out there following the results - this is, emphatically, not intended to be another one of those.

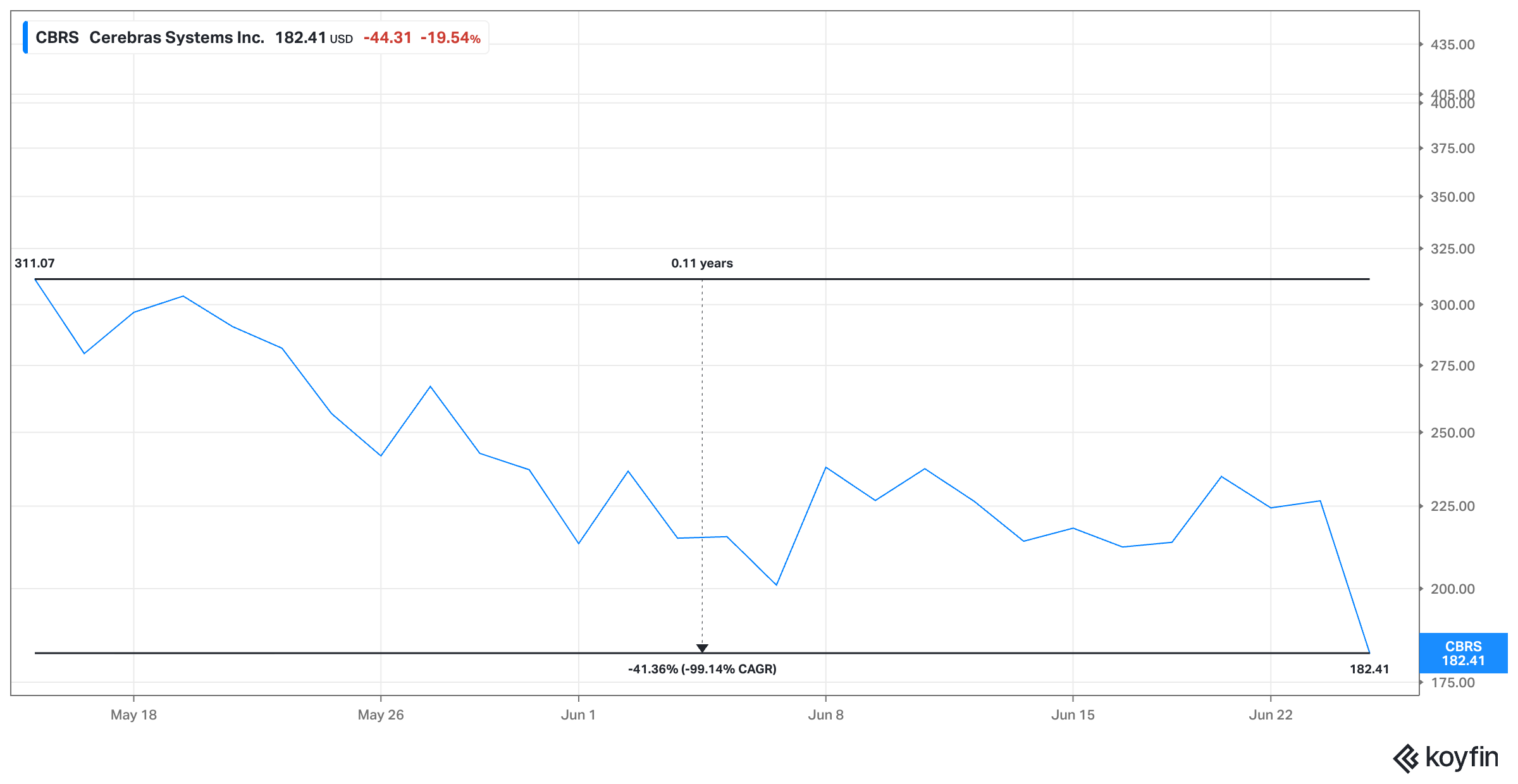

Everything about CBRS currently is very very noisy: the financials, the punditry, the share price… Just to update you since the deep dive, the IPO was priced at $185 but the shares opened on 14 May at $350 and hit an intra-day high of around $400. As I write, the shares are now below the IPO price having plunged 20% yesterday in the earnings aftermath:

As I suggested at the time of my deep dive, the post-IPO reaction is all turning into a bit of a circus. So the point of this post is to take stock of where we are following the IPO and what relevant signals there might be for the future - on a multi-year view.

One important recent development is the commencement of sell-side coverage just a few weeks ago. And what’s really notable about the Q1 earnings is that it kind of looks as though CBRS management were, in their first earnings event, trying to engineer a big beat and raise on both revenue and margin relative to expectations previously shared with analysts - and this is in fact what they did. That the shares reacted so negatively appears to have been a surprise to them (e.g. see here and here). But it might be less surprising to observers of the Beauty Contest. Along with the beat and raise, they signalled a willingness to take some short term margin pain for longer-term gain - the type of act generally not looked upon favourably in present market conditions. Neither does it help that one of CBRS’s greater perceived fragilities is around the margin question - room for doubt. Throw in some second-, third- and fourth- orders of guessing along with a thin float, and a single-day correction of 20% seems fairly run-of-the-mill.

One interesting question worth grappling with is the CBRS valuation at this stage. If the consensus 2028 revenue numbers are in the right ballpark (and the CFO has suggested they are), then the stock is perhaps in the region of 5-6.5x EV/S on a 2028 timeframe (depending on what share count and net cash position you use) - putting it at a significant discount to many other semiconductor stocks (and practically all of those with links to AI). And it’s also growing much faster. But it’s not necessarily to say it’s low risk - the burden very much appears to be on management at the moment to prove that they can execute smoothly and simultaneously on a massive manufacturing and cloud capacity ramp. That said, once you can get past all the hand-waving about high multiples on trailing revenue and such things, CBRS may even be in the process of emerging as a cheap stock following the not-entirely-unexpected post-IPO blowup. For my part, I still own my pre-IPO shares. I will, of course, let full subscribers know if I change my holding in any way.

Now onto the meat and potatoes…

[NFTBC does not give investment advice. Please do your own research.]