Regeneron's Partnerships: "We Like Platforms"

And musings on zero terminal value

Friends of NFTBC

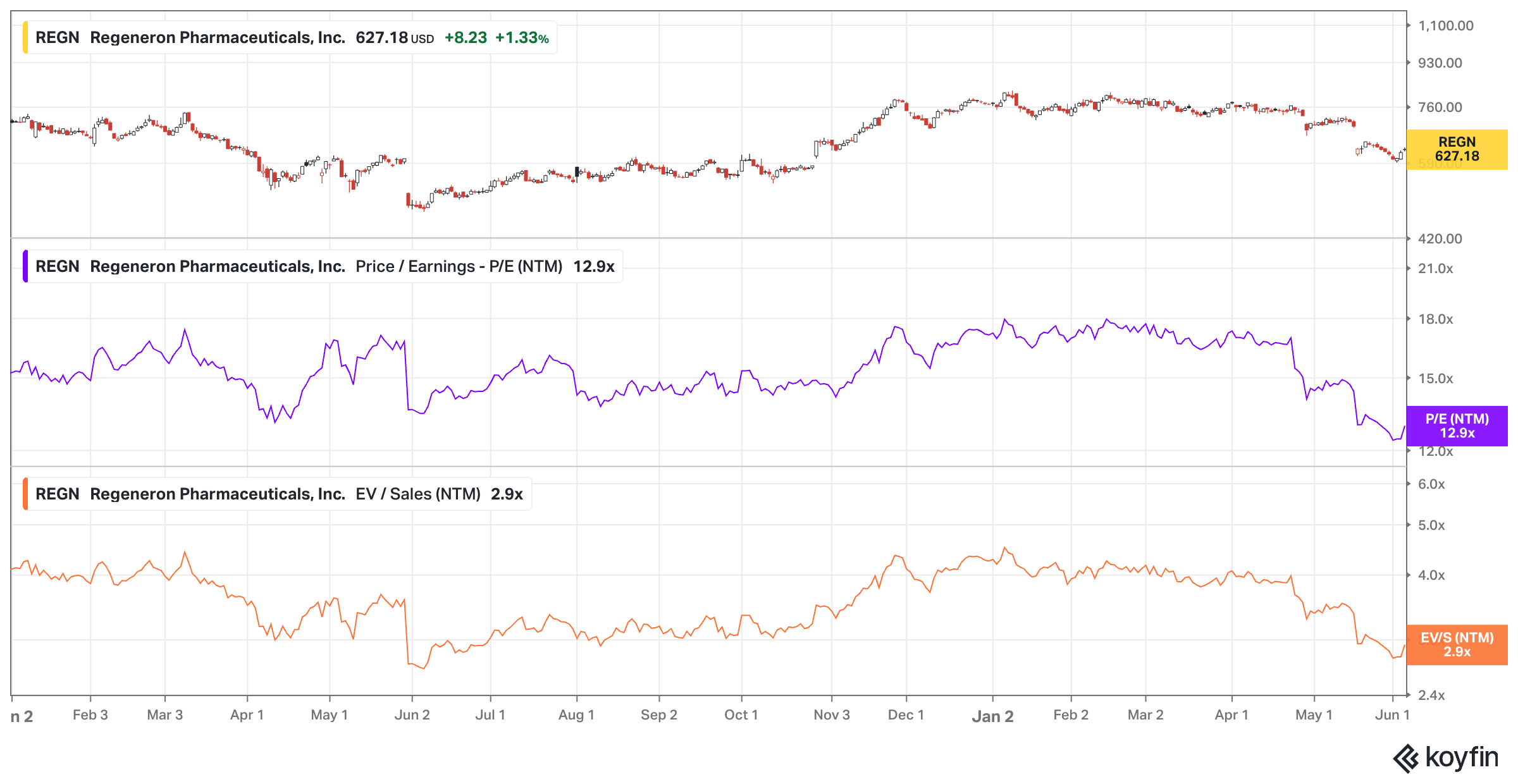

It was exactly a year ago when I wrote to you about the outright despair that had taken over REGN sentiment at the time. Unwittingly, I caught the exact bottom with that post, with the shares going on to appreciate by around 70% over the following 6 months.

…Yet here we are a year later and we’re back in much the same position from a sentiment and valuation perspective:

Once you factor in REGN’s massive $16bn net cash pile, the effective P/E is 8-point-something on consensus numbers for the next 12 months. 8x earnings is so low, that you’ll be hard pressed to find anything much lower in this sector - not even in the stodgiest dregs of old big pharma. And don’t forget, REGN invests in R&D at twice the rate - on a like-for-like basis the P/E drops to just 6x. Moreover, on consensus numbers (which I think are too low by the way), REGN is set to grow its earnings by 70% out to the end of the decade. This is why, at various times over the last 12 months, co-founder Len Schleifer and others have claimed that you can arrive at the company’s entire market value just from the cash flows of Dupixent.

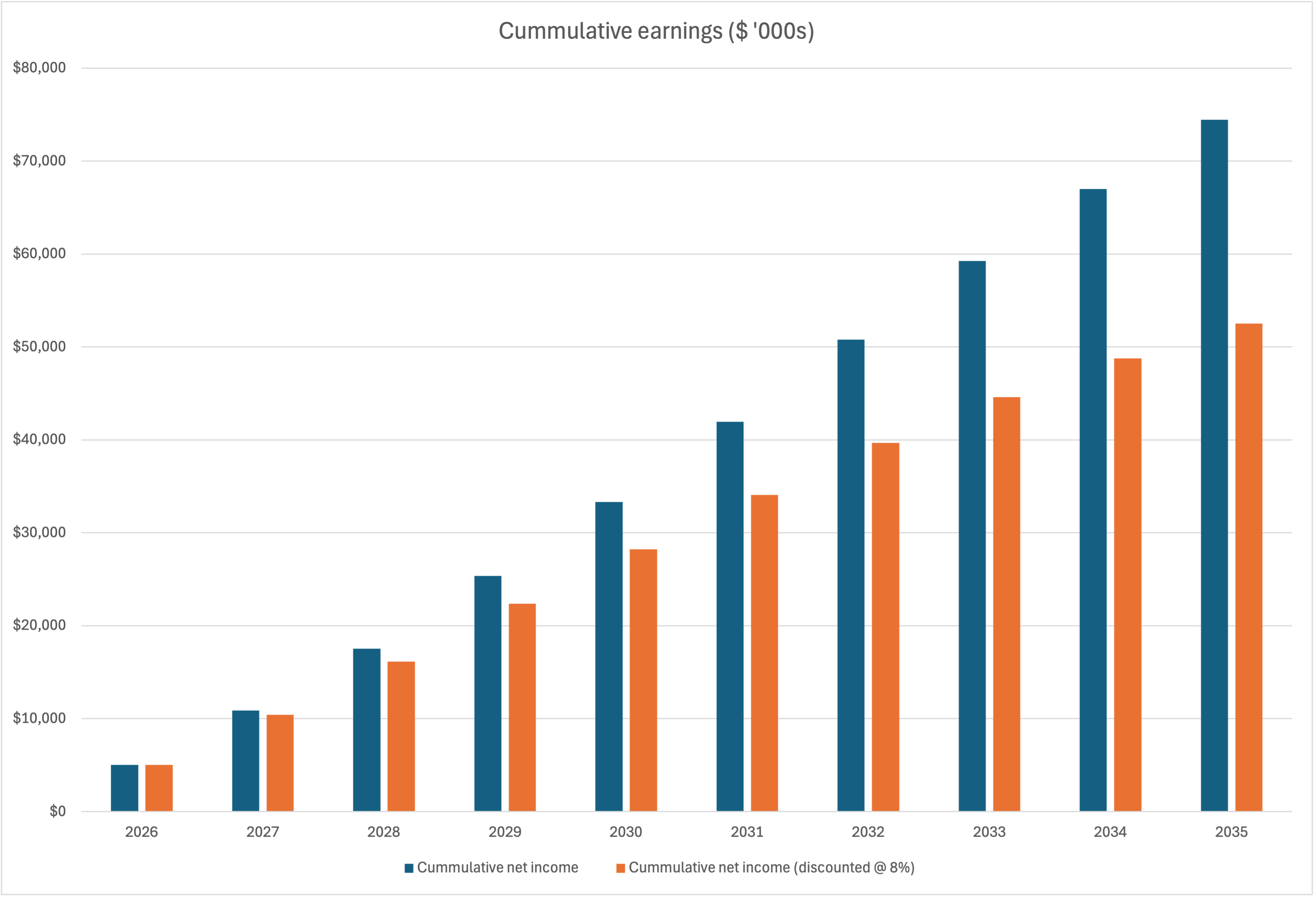

Here’s a similar and very simple way of thinking about it:

Note I’ve picked consensus net income here for simplicity (and because it’s the lower number than free cash flow). And you can pick your own discount rate, but the point is that earnings between now and the early/mid 2030s account for 100% of REGN’s current unlevered market cap or enterprise value.1 Or in other words, the implication is that REGN has zero terminal value beyond the mid 2030s.

Now, of course, I don’t think that anyone really believes this - that would be silly. I think one of two things is going on. Maybe investors have cleverly sussed out that REGN will very shortly go into steady decline and will be much smaller in the 2030s than sell-side analysts collectively think. For example, REGN would be approximately fairly valued today at a terminal multiple of 10x if you assume it makes 40-50% less money than consensus over the coming 10-year period. Even if someone only had a moderate understanding of REGN’s core products, collaborations, IP and competitive landscape - this wouldn’t be much less silly than the notion of zero terminal value in my view. So here’s the more likely explanation: investors are collectively just playing their own games, and the market cap is merely the outcome of those games at this snapshot in time. I’ve written about these games before, and in fact the very name and premise of this blog comes from the Keynesian Beauty Contest. There’s no shortage of reasons to positively downvote REGN’s in the Beauty Contest right now:

Two phase 3 misses in the last year (and extrapolation therefore / Gambler’s Fallacy)

Ongoing Eylea approval delays in the US (Eylea fears being the traditional bête noire with this company)

A handful of CRLs in recent years (and the assumption the problem is structural)

Dupixent loss of exclusivity creeping into the distant horizon

Monkish abstinence from big M&A

Investing more than twice the industry average in internal R&D2

The last two in particular render REGN something of a total weirdo in the minds of many players - and surely no one’s going to vote for the weirdo in a Keynesian Beauty Contest. If only REGN would behave more conventionally - throw on a little Instaglam if you like - then perhaps the players would take more notice. Or so it might seem. But we all know about unconventional beauty - and it’s arguably the more profound and enduring kind. If there’s a purpose to this blog, it’s in seeking out and exploring some of these cases. Naturally, I make no promise that I’ll always be right about them. That said, I suspect I am right about REGN - only time will time. Time being the operative word here. As I’ve said a few times at NFTBC before, I don’t even think the bears are wrong at all - we’re just playing different games. Games with very different time horizons for the most part. Which brings me to…

…the more serious part of this post. So why do I believe that REGN deserves a terminal value much higher than zero? For one thing, I was struck by something co-founder George Yancopoulos said earlier this year:

A lot of people have a mistaken belief that it's easy to make antibodies and all antibodies are created the same. More fully human antibodies have been approved from our platform than any other platform, 10% to 20% of all approved antibodies come from our platform. And we repeatedly are producing the best agents with the least number of problems such as antidrug antibodies and so forth. And so when you have 2 antibodies against the same target, they’re not necessarily the same. And across many programs. Remember, other people have tried to make DUPIXENT-like antibodies that all failed, including Amgen. So it’s not that easy to always make the best antibodies. Our platform and our people have perfected that ability. And that’s why our antibodies seem to work in places where other antibodies against the same targets don’t work.

I had never thought about it in those terms before, but it’s true. Depending how exactly you count it, somewhere in the mid- to high-teens percent of all fully human antibodies currently approved came out of REGN’s VelociSuite platform. The odds that this platform continues to turn out great therapeutic antibodies therefore seem very favourable - VelociSuite’s not worth nothing anyway. I have written about it before, so I won’t repeat myself here. But I thought it might be more interesting to write about another important and overlooked contributor to REGN’s terminal value: platform partnerships. And this is where we come back to time horizons.

The central platform partnership in REGN’s commercial operation is, of course, the one originating in the Sanofi antibody collaboration - established back in 2007. VelociSuite was the platform and Sanofi were paying to access it, on pretty favourable terms to REGN I might add. There were various additions and amendments made in the ensuing years. Here we are almost 20 years later and antibody therapeutics born of this alliance are currently annualising at around $23bn and together grew more than 34% in the latest quarter. A great pharmaceutical collaboration can take years and years to really pay off. But who in this industry has a 20 year time horizon? Who even has a 5 year horizon? Certainly not your typical investor anyway. As Len recently noted, he’s worked with 8 different Sanofi CEOs during the collaboration. It’s almost impossible to imagine that the collaboration would have been as successful if the same turnover and constant rearranging of the deck chairs had applied on both sides. Despite Sanofi’s numerous unforced errors3 this is arguably the most successful pharma partnership of all time. But what if instead of Sanofi, both parties were more REGN-like in time horizon and innovative by nature, and the resulting value creation was more multiplicative rather than one sided? And what if instead of one such partnership REGN had 10 or so of these with new ones landing every year? These are the sorts of questions that I believe should feed into the conversation about REGN’s terminal value. Why? Because it’s literally their strategy, or a major part of it anyway.

As a reminder, via its sequencing operation RGC, REGN plans to sequence the genomes (and increasingly, proteomes) of tens of millions of people in the years ahead, with the specific intention of using this unique resource to generate insights and invent innovative therapies. But only a portion of this tidal wave of genetically validated drug targets will be optimally addressable with plain vanilla VelociSuite-derived antibodies. REGN is well aware of this hence their desire to expand into new modalities. While some of this can be done in-house (e.g. bispecifics, ADCs), much of it is better achieved through platform partnerships where both parties can bring something valuable to the table: world-leading target discovery and antibody technologies on REGN’s part and world-leading capabilities in new modalities and related technologies on the part of partners.

By the mid-2030s I would expect REGN’s revenue from partnered products to be one of the fastest growing parts of the business, albeit still a minority share relative to pure VelociSuite products. The evidence for this is the fact that ~60% of REGN’s phase I pipeline is constituted of partnered molecules, most of which from the Alnylam partnership. Including also the partnered assets already in phase 2, one could well envisage waves of new approvals during the early- to mid-2030s period - right at the time when REGN is implicitly supposed to be worth nothing at all. And we can only imagine what the pre-commercial partnered pipeline might look like at that stage. But outside of REGN and its partners, no one is thinking that far ahead. We’re talking here about the event horizon, beyond which the analysts’ models cannot possibly see. And they’ll give you all sorts of very good reasons why: this industry is far too unpredictable to model that far into the future - fair enough, I don’t disagree. But I ask: do you even need to model it? At today’s prices you’re getting the 2033 instantiation of REGN essentially for free. The pharmaceutical industry being inherently fat-tailed, this makes the option-like nature of REGN kind of interesting to me. REGN is built from the ground-up to exploit these fat tails and stay in the game long enough to reap the rewards:

Platforms, platforms, platforms: lots of low-cost bets through repeatable constantly-improving platforms, rather than one-off assets and singular bets acquired through competitive bidding

Skewing the odds of success: it’s not only about shots on goal. The centrepiece of George’s philosophy is removing bottlenecks in the R&D process. This is what VelociSuite/platforms and RGC are for: making the shots on goal faster, cheaper, much more precise - more option-like

Pipelines in products: one product, multiple indications, massive payoffs

Unconventional behaviours: time horizons measured in decades rather than quarters, optimising for fat tails rather than smooth earnings, avoiding the average, being unafraid to look weird/wrong etc

Massive pile of cash: safety + optionality.

I think there are two ways to play REGN. If you’re skilled at reading the tea leaves - then go for it and play the short term game. This stock moves around a lot (actually for this reason) and that creates opportunity. Alternatively, if you’re as fascinated as I am by the things going on at this company you can use such occasional opportunities to build yourself a stake and settle in for the journey whenever that may go. One way or another, it’ll be fun.

Now lets talk some more about partnerships.

[NFTBC does not give advice - please do your own research. I currently own shares in REGN]

The idea of doing some version of this post has been percolating for a while. I have written about the Decibel platform before and the increasing importance of the Alnylam partnership has come up a few times too. But REGN’s recently announced collaboration with Parabilis Medicines was the eventual catalyst - it looks like a really interesting partnership.