The NFTBC Digest (17 May 2026)

News, Earnings & Links (BMW, CBRS, OBCK, PRCT, REGN)

Friends of NFTBC

Welcome to The NFTBC Digest - a regular email that normally goes out to full subscribers only. Since I started it last year, The Digest has essentially developed into a repository for all the material that I have decided not to make into standalone posts - generally news, earnings, links and occasional updates around my own portfolio activities. Every once in a while I’ll do a wider-circulation email, principally to ensure that newer joiners are aware that The Digest exists. This week’s will be slightly longer than usual as there were plenty of things worth writing about with regard to NFTBC stocks.

The week certainly had its ups and downs. I’ll dispense with my usual alphabetical ordering and get straight to the bad news.

Regeneron

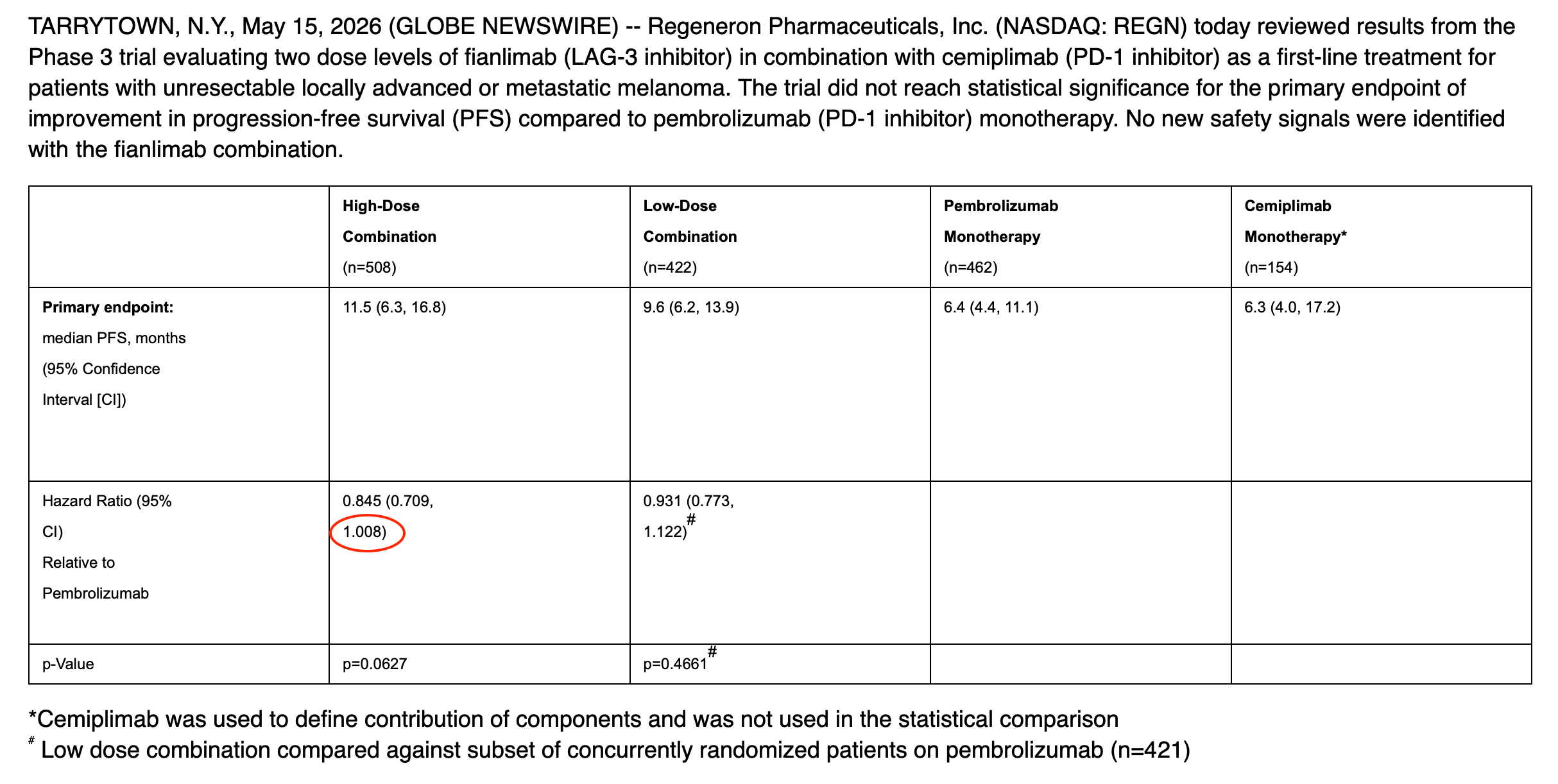

On Friday evening Regeneron provided an update on their long-anticipated fianlimab-cemiplimab combination trial in metastatic melanoma. The trial did not reach statistical significance for the primary endpoint of improvement in progression-free survival (PFS). Regeneron has inevitably taken some heat for releasing the results on a Friday post-market close, but per the press release they only reviewed the results themselves on Friday. The press release itself contains not a single word of commentary, only headlines and data - which seems rather unusual. My guess is that Regeneron probably felt the need to get this news out as quickly as possible before having had sufficient time to process it in any helpful manner, but no doubt others will have different takes.

It’s clear that Regeneron was expecting a positive result in this trial, as was I. However, the timing of the readout was previously deferred a couple of times due to the unexpectedly slow accrual of events in the study - this has been well communicated and discussed and consequently there was already some degree of building scepticism prior to Friday. Additionally, some months ago they amended the trial protocol to include additional patients from the overall survival cohort in order to be able to accumulate more events.

Last year they provided two possible explanations for the slow rate of events - either the pembrolizumab control arm was performing better than expected or the study drug was delivering long and durable responses. They also mentioned they were looking for a PFS in the low- to mid-teens of months in order to be differentiated against the existing field - and that’s against the context of the 24 month PFS they reported from their pooled phase I cohorts.

Here are the headlines:

You can see the high-dose combination (the principal dose of interest) failed on statistical significance - and it seems to be a particularly narrow fail as indicated by the upper bound of the hazard ratio confidence interval only very marginally crossing the 1.0 threshold. In any case the 15.5% relative risk reduction likely falls short of the company’s expectations. Median PFS at 11.5 months arguably just makes it into the low- to mid-teens they were hoping for at a minimum (if we take that to mean 11 to 15).

Notably, they were only expecting the pembro arm median PFS to land somewhere in the range of 4 to 5 months when they designed the study, although they previously said the study was conservatively powered to assume 7 months. In the event it was 6.4 months - which suggests that not only did pembro outperform their expectations, but the fianlimab combination underperformed their expectations. I think our working assumption has to be that the fianlimab combination is not as good as Regeneron was hoping.

However. We are told that detailed results will be presented at an upcoming medical meeting and presumably the data will continue to mature (the study officially runs until 2031). One plausible theory is that at the cutoff date there was a high number of censored (i.e. event-free) patients in the fianlimab arm who may go on to have durable responses beyond the 11.5 months - especially in the context of the 360 overall survival cohort who were dropped in later (and enrolled January to late Summer 2025). In such a context, the study could still have been underpowered at the analysis point. With maturing data, it’s not impossible that PFS goes up and hazard ratio improves. How likely this is, I just don’t know. There’s also the overall survival data. While I’m certainly not betting that this trial delivers subsequent positive surprises, it’s probably premature to draw any strong conclusions about fianlimab before there’s more data in hand.

The good news is that fianlimab still has a further shot on goal in metastatic melanoma coming up in around 10 months - the head-to-head against Opdualag, another LAG-3 combination that’s already on the market. A convincing superiority readout against Opdivo would certainly be helpful in reviving hope of approval and a meaningful commercial opportunity. I think there’s a decent chance that the fianlimab combination could still stack up favourably against Opdualag. That’s partly because Regeneron likely has the better anti PD-1, partly due to their being able to administer their anti LAG-3 at a higher dose and partly due to the relative ORRs they’ve previously shown. We’ll just have to wait until Q1/Q2 next year to find out. But what might make the difference in commercial traction will be the eventual overall survival data, if it’s encouraging.

I wouldn’t write off fianlimab in metastatic melanoma just yet, although in the absence of further data we should downgrade our expectations and push the timeline out by another year. In my mental model, fianlimab was not one of the sizeable opportunities that was going to have a major contribution to intrinsic value. Rather, it was going to be incrementally helpful out to the end of the decade in the interim phase before before some of Regeneron’s bigger swings start to come to fruition. For some context, Regeneron recently said they believe the global metastatic melanoma market opportunity to be between $2bn and $3bn, of which Opdualag does ~$1.2bn.

A convincing win in the pembro head-to-head would certainly have been very helpful for sentiment around the stock and the company in general. But, alas, I suspect this failure will be received in a similar way to the itepekimab failure 12 months ago. As such, we should be braced for a severely negative market reaction next week with this readout being construed as another loss of confidence. The market seems to be much more of a mind to focus on Regeneron’s failures rather than the successes at this moment. But it’s important not to overlook the successes - for example the C5 program is the much more interesting commercial opportunity than fianlimab in my view and it’s coming soon.

An outstanding question is whether Regeneron blundered in designing the pembro head-to-head trial in the way they did or if they just got unlucky. I don’t know enough to have a view - if you have one, I’m happy to hear it. I’m not a clinical trials expert, but I know some of you are. I have left the comments section open, so feel free if you would like to add something or otherwise explain where I have erred.

Now back to alphabetical order…

BMW

In the last Digest I suggested the possibility of a standalone post following the AGM this week. In the end I decided against this. Last year’s AGM was unusually eventful (so far as BMW AGMs go) with the first public showing of the (camouflaged) iX3 and i3 Neue Klasse models as well as a rare speech given by controlling shareholder Stefan Quandt. This year was more business as usual, although did mark the last occasion with Oliver Zipse as chair of the executive board. The renewed plan here is to post a few combined notes and interesting quotes from the both the earnings conference calls (analysts/media) and AGM.

The most notable thing that came up was the idea of export credits in the US. Apparently BMW is in discussions with the US administration about implementing an offset agreement whereby BMW is allowed to import one vehicle for each one it exports. Per comments, the administration seems to be very supportive of the idea and “there’s a very good chance to implement it” - but it all hangs on the EU first implementing their side of last year’s trade deal first. This would clearly be tremendously positive for BMW’s margins given that they import as many vehicles into the US as they export (i.e. net imports are roughly zero) - and it would allow for a faster recovery to the 8-10% strategic automotive margin corridor.

Speaking of which, in my last BMW post I modelled a return to the 8-10% corridor in 2029 along with a potential doubling of automotive profits in the 2025-2029 period (via a dip in 2026). The corridor came up on the analyst call:

the 8% to 10% is not unreachable. Don’t forget that it is 3 x 1 EBIT point we have to achieve. One is on the performance side. We love our BMW ecosystem, and we can do even better. Not to forget Alpina to come, which is also positive for the contribution side. Not to forget that the Gen 6 Neue Klasse has a much better contribution margin than the Gen 5, as we all know for a while. So that’s the performance 1 EBT point.

Second one is, of course, we are doing our homework, working on the material cost side, on the manufacturing cost side, on the warranty cost side. If you have a better quality, you have to provision less warranty costs, which is also contributable to the EBIT margin, not to forget and of course, also logistic costs, et cetera, to be optimized with our global footprint. So that’s the second EBIT point.

The third EBIT point is also homework, is our fixed cost levels, which we are also coming down, as we mentioned already, step by step in ‘26 and ‘27 and also in ‘28. Not to forget the BBA purchase price allocation depreciation, which is always accounted for 1.1, 1.2 EBIT points. This is only lasting until mid- ‘28. So you will have already a half year effect in ‘28 and a full effect in ‘29.

So with these elements to come, there is a chance to come back to 8% to 10%. Of course, we are not naive. There is always something coming around the next corner, whether there are tariffs or other crisis points, and we mitigate as they come along. And we have plans already to do so.

“Not unreachable” / “there is a chance”. I’ve been following BMW long enough to have developed an ear for ‘BMW Speak’ which is characterised by wiggle room and conservatism. My translation is something like this: “We’re gunning hard to get back to 8-10% in the next several years and have a well-developed plan to do it - but we’re not giving guidance on it”.

On differentiation versus ‘monoculture’ in the China auto market:

when you walked over the Beijing Auto Show and compared what the BMW Group was representing and what the rest of the show was representing by and large, there was a very focused presentation of most of the players in that industry. The majority was electric. The majority was the same segment of cars, very few sedans, a lot of SAVs of larger size, focus on autonomous driving, it’s all the same. It was almost a monoculture. And of course, markets worldwide, they are not monolithic. They are widespread. They are differentiated by drivetrains. They are differentiated by size. They’re differentiated by price segments.

And then you looked at the BMW Group stand. There was a large portion of MINI with all drivetrains available. Then you look at the BMW stand, you saw individualization. You saw all drivetrains. You saw V8s. You saw, of course, the Neue Klasse, fully electric. You saw smaller cars. You saw the new 7 Series. You saw our focus on hydrogen. So the full breadth of a premium player, you saw that. And that differentiates BMW. The variety, which represents the variety of market segments. And you don’t have to look on a global scale. You see that in China as well. The markets are much more wider than you would see on that fair.

And that is a worrying thing. If the whole industry thinks they can concentrate only on one segment, larger cars, SAVs, electric, then something is wrong. On the other hand, this makes us more resilient, antifragile to offer the whole breadth. Let’s just look at the first 3 months. EV sales in China were plummeting, not only decreasing, they were plummeting. And what happened, our ICE sales went up at the same minute. So especially China shows what it means to be a full segmenter, to be technology open and at the end, also to be a global industry. That was proof that our strategy is right.

Much is being made currently of the entry of the Chinese into the premium market. When I originally wrote the deep dive, I had some of these things in mind. It’s one thing to pack in a load of features and undercut competitors on price (which gets much of the media attention in the moment), but it’s another altogether to have a desirable and successful premium brand with longevity - I think this is a really under-appreciated characteristic of BMW that gets lost in today’s noise. It’s really really hard being a successful premium automotive brand, but BMW is uniquely good at it. Zipse added some useful thoughts on the topic:

on the strategic side, what is premium in the future? Premium of the future is product quality, specifically long-term product quality. It does not make sense to push cars in the market who lose their resale value after 2 or 3 years’ time. This is not premium. So it’s not feature count in a new car, it’s what is the residual value after 1, 2, 3 or even 5 years. I’m not even talking about historic cars of 15 or 20 years. That is premium.

The second thing is premium system integration. It’s not feature count. We discussed what we saw in Beijing, again, feature count over future count. That’s not the point. How does that all play together? How does it fit? And is it for someone who drives the car, not while it’s standing, but while it’s driving, does it fulfill the function they are supposed to?

And the third one is safety. And I think that becomes one of the foremost criteria for premium of the future, safety, no casualties, no risks. Absolute promises to a brand who promises to be premium means no casualties, no risk in driving the car. And I think that will define premium of the future, and I think we are well underway to fulfill that promise.

And, relatedly, on who will be the survivors in the next five years:

I still think there’s too much focus from the media, but also from the capital markets on individual players, individual technologies, singular events. In 5 years’ time, the players who will still survive, they have the competence to system integrate, to bring all technologies into a car, who build cars who have a long-term quality, who are not falling apart after 1 or 2 years, who will still be in service after 5 years. It’s a completely different game which is happening there, and who are able to differentiate between a singular hype and an overall business model.

If you watch the industry today, actually, there are too many bets going on, too many bets on a singular technology that might happen, but this cannot be endured. So much money is lost in this industry on bets. So system integrators who are able to follow regulation and at the end, have still a business model on high-quality products, that’s the key of everything. And in 5 years from now, to follow CO2 regulations specifically and remain a profitable business will be more or less the key to everything.

Some interesting facts about BMW in Germany (that came up during the AGM):

one in three customers who have ordered the new iX3 are new to the BMW brand

in 2025 they built more than one million cars in Germany - the most ever. 25% of all cars built in Germany are now BMWs. I have a strong impression that few investors/observers appreciate the contrast with the wider German automotive industry here

Next - conversion of preferred shares to ordinary shares. This was approved at the AGM. One thing I actually hadn’t appreciated was the possibility of a technical benefit to the share price from the conversion and a strengthening of BMW’s weighting in the various indices.

One last thing: BMW has now unveiled its first Vision Alpina model. As a reminder, a couple of years ago BMW licensed the historic BMW-underpinned Alpina brand from the Bovensiepen family with plans to relaunch Alpina has a BMW sub-brand positioned between the highest-end BMWs and Rolls-Royce. This is presumably Bentley and Aston Martin territory with ASPs in the EUR 200,000 to 250,000 range. Alpina production models are due to hit the roads starting in 2027. It’s worth noting that CFO Walter Mertl specifically referenced their expectations of a positive margin contribution (see above). As I’ve noted before, Rolls-Royce ASPs are over EUR 500,000 and they make, I suspect, margins at least in the higher 20s percent range on 6,000 units per year - it’s potentially in the region of 15% of group automotive EBIT. Alpinas were previously very rare with around 2,000 sold per year prior to the license deal, although there’s perhaps no reason in principle why they can’t drive this to 6,000 (~Aston Martin) or even 10,000 (~Bentley) if they’re particularly shrewd in their positioning/strategy. Assuming margins in the low 20s (such as Bentley managed until recently) it becomes possible to envisage a 20-30bps automotive margin contribution by the end of the decade - hence why I assume Mertl brought it up. Here’s BMW’s video of the Vision Alpina:

Cerebras

Following my recent deep dive Cerebras has now gone public. You can watch the five founders ring the opening bell here. I will now start accounting for my shares in my listed stock portfolio and you’ll see further updates at NFTBC. Until the lock-up ends in September, effective free float is only 16% at the moment and according to comments made by the CEO, the IPO was 25x oversubscribed - in other words, some more reasonable measure of price discovery perhaps won’t come until later in the year.

Cerebras’ CFO Bob Komin was interviewed on CNBC and a couple of notable points came up:

He said Cerebras’ valuation was probably trading in line with Nvidia on 2028 revenue. With Nvidia at ~8x calendar-2028 EV/S this might imply Cerebras is anticipating a much more aggressive revenue ramp than what I modelled in the deep dive. I said in the deep dive that the range of outcomes is particularly wide, and this also includes the possibility I was too conservative

They are already serving one trillion parameter models, including ChatGPT 5.4 and 5.5 internally for OpenAI. These are not yet released to the public “but that’s coming very soon”. This is one of the key debates around Cerebras. A one trillion parameter model might require 46 or more CS-3s to fit it, at $1 to $1.5m each - so there are serious questions as to whether that is economical relative to the throughput. I’m assuming there are various co-designed elements to it that we can’t see from the outside including things like disaggregation. But I’m also starting to wonder if the relationship could eventually involve an element of sparse pretraining (weight sparsity) which is only possible on Cerebras hardware. It was supposed to be one of Cerebras’ USPs before the pivot inference in 2024 and everyone seems to have assumed it was a dead end - but is it..? In any case, if they start serving 5.5 at high speed soon, I think that’s going to be a really big deal - there won’t be anything else like it

Ottobock

Ottobock announced that it is acquiring Blatchford’s Norwegian patient care business. The price is EUR 110m and comes with EUR 40m in revenue. In effect, this signals Blatchford’s retreat from patient care outside of the UK. This is actually quite interesting. I discussed some of the competitive dynamics in the deep dive - I think Ottobock’s forward integration model is going to be very tough to compete with and Blatchford has apparently dropped its decade-long ambition to try the same.

Procept

Procept spoke at the Bank of America Global Healthcare Conference this week. CEO Larry Wood provided some helpful context around the prospect of a hybrid support model that they started talking about recently:

The going to a hybrid support model is really not about trying to drive leverage out of the P&L. What it’s really about is trying to drive procedure growth. And what I worry about is that we could be losing procedures here and there because a doctor sits there on a Thursday and says, I got 2 more cases tomorrow, I could do Aquablation, but I don’t want to call the rep or maybe he’s always [out of town] on Friday.

And what I don’t want to do is ever lose any cases because we can’t get somebody there. I want our team routinely visiting with our customers. I want them routinely making sure the system setup is being done properly. There’s a lot of turnover of staff in hospitals, and there’s a setup element to the robot, and we want to make sure that people are doing that right and doing it correctly.

So I always want our people in that. There’s never going to be something where we don’t see a customer for 3 months and they’re just written off cases. And I think there’s actually - at some level, there’s a risk to the business that you quit paying attention to your customer and you just open the door for other people to come in. So we’re always going to be there doing that.

I just don’t want somebody dependent on us. I don’t want somebody saying, if a rep can’t get there, if a rep is sick tomorrow, I can’t do cases and thus I’m going to have to convert them to something else. So I just see this as a lever for us to be able to continue to drive case growth more than I see it as an operational lever. Now the byproduct of it is if we can cover - if we can double the number of cases and we can keep our sales footprint the same or grow slightly, obviously, that drives tremendous leverage for us. But it’s a byproduct, it’s not the reason.

That’s it for this edition. Thanks for reading.

Get in touch if you have any comments or questions.